RBS 2012 Annual Report Download - page 496

Download and view the complete annual report

Please find page 496 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

486 -

487

487 -

488

488 -

489

489 -

490

490 -

491

491 -

492

492 -

493

493 -

494

494 -

495

495 -

496

496 -

497

497 -

498

498 -

499

499 -

500

500 -

501

501 -

502

502 -

503

503 -

504

504 -

505

505 -

506

506 -

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

494

Additional information continued

Financial summary continued

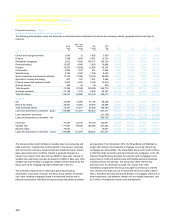

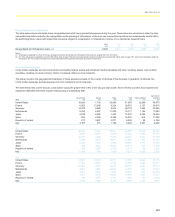

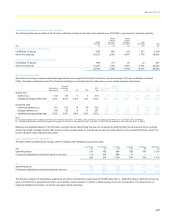

Risk elements in lending

Risk elements in lending (REIL) comprises impaired loans and accruing loans past due 90 days or more as to principal or interest.

Impaired loans are all loans (including renegotiated and forbearance loans) for which an impairment provision has been established; for collectively

assessed loans, impairment loss provisions are not allocated to individual loans and the entire portfolio is included in impaired loans.

Accruing loans past due 90 days or more comprise loans past due 90 days where no impairment loss is expected and those awaiting individual

assessment. A latent loss provision is established for the latter.

2012

£m

2011

£m

2010

£m

2009

£m

2008

£m

Impaired loans (2)

Domestic 15,323 14,528 15,471 13,572 8,588

Foreign 23,163 24,219 20,230 21,453 10,891

Total 38,486 38,747 35,701 35,025 19,479

Accruing loans which are contractually overdue 90 days or more as to principal

or interest

Domestic 2,007 1,697 2,363 2,224 1,201

Foreign 634 401 534 1,000 581

Total 2,641 2,098 2,897 3,224 1,782

Total risk elements in lending 41,127 40,845 38,598 38,249 21,261

Closing provisions for impairment as a % of total risk elements in lending 52% 49% 47% 46% 52%

Risk elements in lending as a % of gross lending to customers excluding

reverse repos (4) 9.1% 8.6% 7.3% 5.4% 2.5%

Notes:

(1) For the analysis above, 'Domestic' consists of the United Kingdom domestic transactions of the Group. 'Foreign' comprises the Group's transactions conducted through offices outside the UK and

through those offices in the UK specifically organised to service international banking transactions.

(2) The write-off of impaired loans affects the closing provisions for impairment as a % of total risk elements in lending (the coverage ratio). The coverage ratio reduces if the loan written off carries a

higher than average provision and increases if the loan written off carries a lower than average provision.

(3) Impaired loans at 31 December 2012 include £5,350 million of loans whose terms were renegotiated or secured retail loans subject to forbearance granted during 2012.

(4) Includes disposal groups.

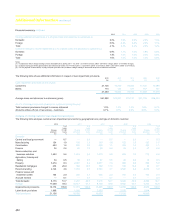

2012

£m

2011

£m

2010

£m

2009

£m

2008

£m

Gross income not recognised but which would have been recognised under the

original terms of impaired loans

Domestic 665 636 579 625 393

Foreign 940 964 830 1,032 338

1,605 1,600 1,409 1,657 731

Interest on impaired loans included in net interest income

Domestic 232 220 214 226 150

Foreign 244 264 241 182 42

476 484 455 408 192

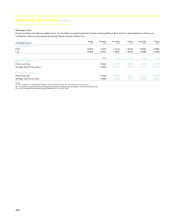

Potential problem loans

Potential problem loans (PPL) are loans for which an impairment event has taken place but no impairment loss is expected. This category is used for

advances which are not past due 90 days or revolving credit facilities where identification as 90 days overdue is not feasible.

2012

£m

2011

£m

2010

£m

2009

£m

2008

£m

Potential problem loans 807 739 633 1,009 226

Both REIL and PPL are reported gross and take no account of the value of any security held which could reduce the eventual loss should it occur, nor of

any provision marked. Therefore impaired assets which are highly collateralised, such as mortgages, will have a low coverage ratio of provisions held

against the reported impaired balance.