RBS 2012 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

RBS GROUP 2012

187

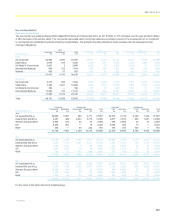

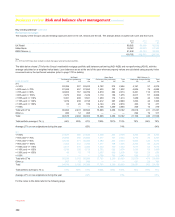

UK Retail Ulster Bank RBS Citizens (1)

2010

Performing

£m

Non-performing

£m

Total

£m

Performing

£m

Non-performing

£m

Total

£m

Performing

£m

Non-performing

£m

Total

£m

<= 50% 19,568 246 19,814 3,385 186 3,571 5,193 45 5,238

> 50% and <= 70% 24,363 345 24,708 2,534 152 2,686 4,902 79 4,981

> 70% and <= 90% 31,711 588 32,299 3,113 179 3,292 7,029 137 7,166

> 90% and <= 100% 7,998 319 8,317 1,958 121 2,079 2,459 67 2,526

> 100% and <= 110% 4,083 260 4,343 2,049 137 2,186 1,534 53 1,587

> 110% and <= 130% 1,722 202 1,924 4,033 358

4,391 1,425 61 1,486

> 130% and <= 150% 57 16 73 2,174 297 2,471 599 28 627

> 150% — — — 355 131 486 589 36 625

Total with LTVs 89,502 1,976 91,478 19,601 1,561 21,162 23,730 506 24,236

Other (2) 1,090 24 1,114 — — — 762 30 792

Total 90,592 2,000 92,592 19,601 1,561 21,162 24,492 536 25,028

Total portfolio average LTV (3) 68% 81% 68% 91% 106% 92% 75% 94% 76%

Average LTV on new originations during the year 68% 79% 66%

Notes:

(1) Includes residential mortgages and home equity loans and lines (refer to page 188 for a breakdown of balances).

(2) Where no indexed LTV is held.

(3) Average LTV weighted by value is arrived at by calculating the LTV on each individual mortgage and applying a weighting based on the value of each mortgage.

(4) Excludes mortgage lending in Wealth. This portfolio totalled £8.8 billion (2011 - £8.3 billion; 2010 - £7.8 billion) and continues to perform in line with expectations with minimal provision of £248 million.

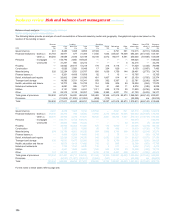

Key points

UK Retail

x The UK Retail mortgage portfolio totalled approximately £99.1 billion

at 31 December 2012, an increase of 2.8% from 31 December 2011.

x The assets are prime mortgages and include £7.9 billion, 8% (2011 -

£6.9 billion) of residential buy-to-let lending. There is a small legacy

portfolio of self-certified mortgages (0.2% of the total mortgage

portfolio). Self-certified mortgages were withdrawn in 2004. The

interest rate product mix is approximately one third fixed rate with

the remainder on variable rate products including those on managed

rates.

x UK Retail’s mortgage business is subject to prudent underwriting

standards. These include an affordability test using a stressed

interest rate, credit scoring with different pass marks depending on

LTV as well as a range of specific criteria, for example, LTV

thresholds. Changes over the last few years include: a reduction in

maximum LTV for prime residential mortgage lending from 100% to

95% in the first quarter of 2008 and from 95% to 90% in the third

quarter of 2008 and a tightening of credit scoring pass marks: credit

score thresholds were increased in the third quarter of 2009 and

again in the third quarter of 2010. In the first quarter of 2011, new

scorecards were introduced alongside a further tightening of

thresholds, these were tightened still further in the second quarter of

2012.

x Gross new mortgage lending remained strong at £14 billion. The

average of individual LTV on new originations was 65.2% weighted

by value of lending (2011 - 63.0%) and 61.3% by volume (2011 -

58.4%). The ratio of total lending to total property valuations was

56.3% (2011 - 52.9%). Average LTV by volume is arrived at by

calculating the LTV on each individual mortgage with no weighting

applied in the calculation of the average. The ratio approach is the

sum of all lending divided by the value of all properties held as

security against the lending.

x The maximum LTV available to new customers remains at 90%,

except for those buying properties under the government-sponsored,

and indemnity backed, new build schemes that were launched

during the year, where the maximum LTV is 95%. These schemes

aim to support the mortgage market, particularly first time buyers,

and completions under the scheme totalled £35 million during the

year.

x Based on the Halifax Price Index at September 2012, the portfolio

average indexed LTV by weighted value of debt outstanding was

66.8% (2011 - 67.2%) and 58.1% by volume (2011 - 57.8%). The

ratio of total outstanding balances to total indexed property

valuations is 48.5% (2011 - 48.4%).

x The arrears rate (more than three payments in arrears, excluding

repossessions and shortfalls post property sale) improved

marginally to 1.5% at 31 December 2012 from 1.6% at 31 December

2011. The number of properties repossessed in 2012 was 1,426

compared with 1,671 in 2011. Arrears rates remain sensitive to

economic developments and are currently benefiting from the low

interest rate environment.

x The mortgage impairment charge was £92 million for 2012

compared with £182 million in 2011 primarily due to lower loss rate

adjustments on the non-performing back book, and a stable

underlying rate of defaults.

x 25.6% of the residential owner occupied UK Retail mortgage book is

on interest only terms down from 27.3% in 2011. A further 9.1% are

on mixed repayments split between a combination of interest only

and capital repayments (2011 - 9.6%). UK Retail withdrew interest

only repayment products from sale to residential owner occupied

customers with effect from 1 December 2012. Interest only

repayment remains an option on buy-to-let mortgages. At 1.6%, the

percentage of accounts more than 3 payments in arrears was similar

to the 1.4% observed on capital repayment mortgages.