RBS 2012 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2012 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

-

337

-

338

-

339

-

340

-

341

-

342

-

343

-

344

-

345

-

346

-

347

-

348

-

349

-

350

-

351

-

352

-

353

-

354

-

355

-

356

-

357

-

358

-

359

-

360

-

361

-

362

-

363

-

364

-

365

-

366

-

367

-

368

-

369

-

370

-

371

-

372

-

373

-

374

-

375

-

376

-

377

-

378

-

379

-

380

-

381

-

382

-

383

-

384

-

385

-

386

-

387

-

388

-

389

-

390

-

391

-

392

-

393

-

394

-

395

-

396

-

397

-

398

-

399

-

400

-

401

-

402

-

403

-

404

-

405

-

406

-

407

-

408

-

409

-

410

-

411

-

412

-

413

-

414

-

415

-

416

-

417

-

418

-

419

-

420

-

421

-

422

-

423

-

424

-

425

-

426

-

427

-

428

-

429

-

430

-

431

-

432

-

433

-

434

-

435

-

436

-

437

-

438

-

439

-

440

-

441

-

442

-

443

-

444

-

445

-

446

-

447

-

448

-

449

-

450

-

451

-

452

-

453

-

454

-

455

-

456

-

457

-

458

-

459

-

460

-

461

-

462

-

463

-

464

-

465

-

466

-

467

-

468

-

469

-

470

-

471

-

472

-

473

-

474

-

475

-

476

-

477

-

478

-

479

-

480

-

481

-

482

-

483

-

484

-

485

-

486

-

487

-

488

-

489

-

490

-

491

-

492

-

493

-

494

-

495

-

496

-

497

-

498

-

499

-

500

-

501

-

502

-

503

-

504

-

505

-

506

-

507

-

508

-

509

-

510

-

511

-

512

-

513

-

514

-

515

-

516

-

517

-

518

-

519

-

520

-

521

-

522

-

523

-

524

-

525

-

526

-

527

-

528

-

529

-

530

-

531

-

532

-

533

-

534

-

535

-

536

-

537

-

538

-

539

-

540

-

541

-

542

-

543

|

|

24

DIVISIONAL REVIEW

Making RBS safer

Our strategic priorities mean that we will

continue to contribute to making RBS safer.

One of these is our sharpened focus on

scalable markets following the introduction of

a refreshed strategy in 2011. During the year

we sold our Latin American, Caribbean and

African businesses to Royal Bank of Canada,

an important step in concentrating on

core geographies.

Together with RBS Group Risk, we introduced

the Coutts Conduct programme in order to

deliver new standards and frameworks by the

end of 2013. The intent of the programme is to

safeguard clients and the business from

breaches of regulatory rules or law.

Building a better bank that serves

customers well

We launched Coutts Mobile in October.

It means we can offer clients greater choice

and flexibility in the way they manage their

banking needs, providing them with the same

access and convenience of Coutts Online

on their smartphone or tablet.

The UK rollout of the Coutts global technology

platform was completed in early 2012, enabling

us to operate as an international organisation

on unified and common information technology,

transforming our ability to serve clients globally.

We introduced a new Sales Management

Framework for the International business

focusing on recruitment and induction,

coaching, training and development, target

setting, performance management

and monitoring.

Throughout 2012, our UK business prepared

to implement the Retail Distribution Review (RDR)

regulations. This resulted in the introduction of

the new advice model on 26 November, ahead

of the required implementation date.

We significantly enhanced our Lombard

lending programme in 2012, which will be

central to our success and a source of

important focus in 2013 and beyond. We set

higher lending values for Chinese H-shares

and Red Chips, and further increased lending

values on Russian bonds. China, India and

Russia were approved as ‘special emerging

markets’, with a corresponding removal of the

50% emerging market cap for each country.

The ruble and renminbi were added as

approved currencies and lending values were

also agreed for renminbi cash and bonds.

In the UK, we launched the Coutts multi-asset

funds comprising a range of seven UK and

global RDR-compliant funds. These aim to

deliver attractive long-term returns by investing

in a broad range of asset classes including

cash, bonds, equities, commodities and

property that allow each client’s individual

investment objectives to be matched to an

appropriate investment strategy based on four

separate asset allocation models.

We introduced a new client feedback

programme in the UK in 2012 in order to

improve the volume and quality of client

feedback and enable us to react swiftly to any

issues identified. We expect to roll out similar

programmes with Adam & Company and the

International business in 2013.

Changing our culture

During the year we began the journey towards

creating Coutts’ 'Crown Standard'. It reflects

our values as we strive for excellence in

everything we do. Whether our people serve

clients at the front line, or work in a functional

or support role, we must take pride in how we

go about our tasks and work to the highest

possible standards.

If we get this right for ourselves, we will get it

right for our clients and we will earn their trust

and loyalty for years to come. Each of us has

a hand to play in building our Crown Standard

and, as we continue with our transformation,

there is every opportunity for us to define what

this should look and feel like.

We held our first Diversity & Inclusion Week

in November. Led by our Diversity & Inclusion

Council, it recognises that at the heart of our

business are our people who represent a

variety of different cultures and beliefs.

We celebrate these differences and want to

embed Diversity and Inclusion in the DNA

of our people and our business.

Wealth

Rory Tapner

Chief Executive,

Wealth

Watch or listen to Rory Tapner

www.rbs.com/AnnualReview

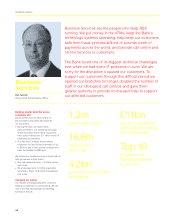

Operating profit increased by £5 million,

or two per cent, to £253 million, driven

by higher income partially offset by

increased expenses and impairment

losses. Total income increased by

£66 million and expenses by £40 million.

Impairments were £21 million higher.

Return on equity increased to 13.7 per

cent. The loan to deposit ratio was stable

at 44 per cent.

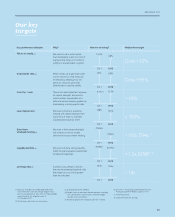

Performance highlights 2012 2011

Operating profit before impairment losses (£m) 299 273

Impairment losses (£m) (46) (25)

Operating profit (£m) 253 248

Return on equity (%) 13.7 13.1

Assets under management, excluding deposits (£bn) 28.9 30.9