RBS 2014 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

3

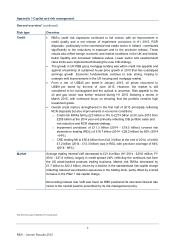

RBS – Interim Results 2015

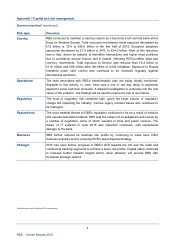

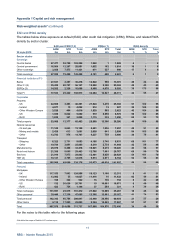

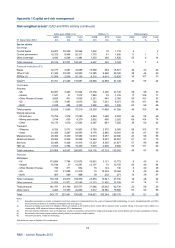

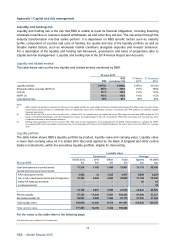

Appendix 1 Capital and risk management

General overview* (continued)

Risk type Overview

Credit • RBS’s credit risk exposures continued to fall overall, with an improvement in

credit quality and a net release of impairment provisions in H1 2015. RCR

disposals - particularly in the commercial real estate sector in Ireland - contributed

significantly to the reductions in exposure and to the provision release. These

results also reflect benign economic and market conditions in the UK and Ireland,

better liquidity and increased collateral values. Lower sector and asset/product

class limits were implemented following the new CIB strategy.

• The growth in UK PBB gross mortgage lending was within credit risk appetite and

against a backdrop of sustained house price growth in 2015 that has outstripped

earnings growth. Economic fundamentals continue to look strong, helping to

underpin mild improvements in the UK housing and mortgage market.

• From a low of US$45 per barrel in January 2015, oil prices recovered to

US$61 per barrel by the end of June 2015. However, the market is still

considered to be oversupplied and the outlook is uncertain. Risk appetite to the

oil and gas sector was further reduced during H1 2015 following a review in

March 2015, with continued focus on ensuring that the portfolio remains high

investment grade.

• Overall credit metrics strengthened in the first half of 2015 principally reflecting

RCR disposals but also improvements in economic conditions:

o Credit risk RWAs fell by £23 billion or 8% to £273 billion at 30 June 2015 from

£295 billion at the 2014 year end primarily reflecting CIB portfolio sales and

risk reduction and RCR disposal strategy.

o Impairment provisions of £11.3 billion (2014 - £18.0 billion) covered risk

elements in lending (REIL) of £18.7 billion (2014 - £28.2 billion) by 60% (2014

- 64%).

o CRE lending fell to £36.4 billion from £43.3 billion at the end of 2014, of which

£7.2 billion (2014 - £13.3 billion) was in REIL with provision coverage of 64%

(2014 - 68%).

Market Average trading internal VaR decreased to £21.8 million (H1 2014 - £30.6 million; FY

2014 - £27.8 million), largely in credit spread VaR, reflecting the continued exit from

the US asset-backed products trading business. Market risk RWAs decreased by

£1.7 billion to £22.3 billion, driven by a decline in the standardised risk capital charge

reflecting reduced securitisation exposures in the trading book, partly offset by a small

increase in the Pillar 1 risk capital charge.

Non-trading interest rate VaR was lower as RBS positioned its structural interest rate

closer to the neutral position prescribed by its risk management policy

*Not within the scope of Deloitte LLP’s review report