RBS 2014 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

32

RBS – Interim Results 2015

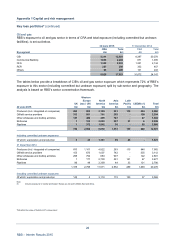

Appendix 1 Capital and risk management

Key points*

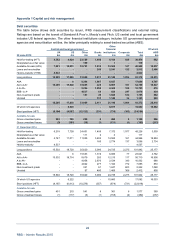

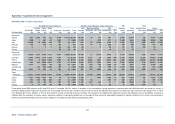

UK PBB

• The UK PBB personal mortgage portfolio increased by 2.1% to £105.4 billion, of which £92.5 billion

(31 December 2014 - £91.6 billion) was owner occupied and £12.9 billion (31 December 2014 - £11.6

billion) was buy-to-let. Of the total portfolio approximately £26 billion related to properties in the south

east of England, while £19 billion related to properties in Greater London.

• Gross new mortgage lending amounted to £9.1 billion in H1 2015 with an average LTV by weighted

value of 70.4% (2014 - 70.5%). Lending to owner-occupiers during this period was £7.5 billion (2014 -

£16.6 billion) and had an average LTV by weighted value of 71.5% (2014 - 71.7%). Buy-to-let lending

was £1.6 billion (2014 - £3.1 billion) with an average LTV by weighted value of 65.1% (2014 - 63.9%).

• Based on the Halifax House Price Index at March 2015, the portfolio average indexed LTV by volume

was 50.4% (2014 - 50.4%) and 57.4% by weighted value of debt outstanding (2014 - 57.3%).

• Fixed interest rate products of varying time durations accounted for approximately 60% of the

mortgage portfolio with 3% a combination of fixed and variable rates and the remainder variable rate.

Approximately 17% of owner-occupied mortgages were on interest-only terms with a bullet repaymen

t

and 7% were on a combination of interest-only and capital and interest. The remainder were capital

and interest. 63% of the buy-to-let mortgages were on interest-only terms and 3% on a combination o

f

interest only and capital and interest.

• The arrears rate fell from 1.0% in December 2014 to 0.9% at the end of June 2015. The number o

f

properties repossessed in H1 2015 was also lower (338 compared with 472 in H2 2014). This reflected

improvements in the UK economy and underlying asset quality

• The flow of new forbearance was £315 million in H1 2015 compared with £367 million in H2 2014. The

value of mortgages subject to forbearance has decreased by 8% since the year end to £4.5 billion

(equivalent to 4.2% of the total mortgage book) as a result of improved market conditions and

methodology changes.

• There was an overall small release of impairment provision for personal mortgages in H1 2015

compared with a small charge in H1 2014. Reduced REIL balances and a fall in the instances o

f

forborne mortgages drove the release in latent and PD90 provisions as well as lower LGDs.

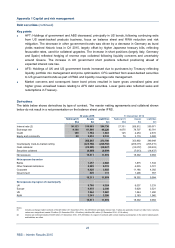

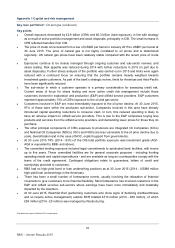

Ulster Bank

• Ulster Bank’s residential mortgage portfolio totalled £15.9 billion at 30 June 2015, with 86% in the

Republic of Ireland and 14% in Northern Ireland. Excluding the impact of exchange rate movements,

the portfolio decreased by 1.3% from 31 December 2014 as a result of amortisation a portion of which

related to the tracker mortgage portfolio. The volume of new business has increased reflecting

continuing market demand.

• The interest-rate product mix was approximately 63% of the mortgage portfolio on tracker-rate

products, 23% on variable-rate products and 14% on fixed rate. Interest-only represented 6% of the

total portfolio.

• The portfolio average indexed LTV decreased from 92% at 31 December 2014 to 89% at 30 June

2015 and reflected positive house price index trends over the last six months.

• At 30 June 2015, 22.3% of total mortgage assets (£3.6 billion) were subject to a forbearance

arrangement, a decrease of 8.3% (£0.3 billion) from 31 December 2014. Excluding the impact o

f

exchange rate movements, the value of mortgage assets subject to a forbearance arrangement has

decreased by £276 million (4.8%).

*Not within the scope of Deloitte LLP’s review report