RBS 2014 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

6

RBS – Interim Results 2015

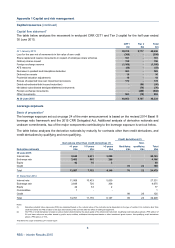

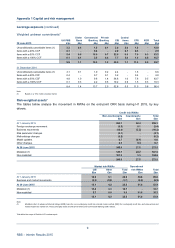

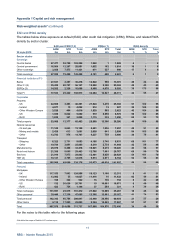

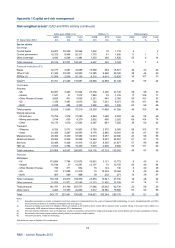

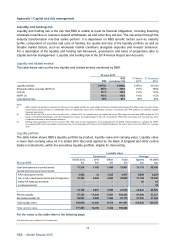

Appendix 1 Capital and risk management

Developments in prudential regulation

The European Union Capital Requirements Regulation (CRR) is in transition until 2019. Recent

developments are set out below.

Capital

The Basel Committee on Banking Supervision (BCBS) has consulted on implementing capital floors, and the

expectation is that the framework design will be based on a standardised methodology that is currently being

revised.

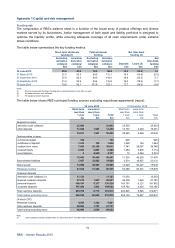

Systemic capital buffers - Global Systemically Important Banks (G-SIB) are assessed according to

methodology set out by BCBS, and an additional loss absorbency requirement has been set according to the

size. An annual assessment of size is undertaken and RBS is currently required to hold a 1.5% buffer.

Additional requirements are being set for domestic (D-SIB) by the EBA (up to 2%) and for ring-fenced banks

by the Financial Policy Committee of the Bank of England (up to 3%).

BCBS is still considering its proposals on the possible inclusion of interest rate risk in the banking book

within Pillar 1 capital rather than the existing Pillar 2 treatment. Similarly, there is a possibility that operational

risk charges will be moved from Pillar 2 to Pillar 1 capital.

A comprehensive review by BCBS into the market risk framework (Fundamental Review of the Trading

Book) is likely to result in changes to the banking book/trading book boundary, replacing VaR with an

expected shortfall model and new, more risk sensitive standardised methodologies which will need to be

calculated for the entire book, regardless of whether a firm has permission to use a modelled approach.

BCBS has finalised rules for the capital requirements of securitisation positions. There is a new hierarchy of

methods, as well as changes to the methodologies. The new rules, effective from 1 January 2018, aim to

reduce reliance on credit rating agencies, although their use will still be permitted subject to local approval,

reduce cliff effects seen in the current rules, and enhance risk sensitivity.

PRA has published a new approach to setting Pillar 2 capital requirements, replacing the capital planning

buffer with a ‘PRA buffer’. Broadly this follows the consultation paper of January 2015.

Disclosure requirements required by regulators will be more frequent, more extensive and much more

standardised (Pillar 3). BCBS requirements will be introduced from the end of 2016 and the more detailed

EU requirements are being phased in during late 2015.

Leverage ratio

The PRA is consulting on implementation of a UK leverage ratio framework, expected to come into force

from 2016, which will incorporate a systemic capital buffer and a countercyclical buffer when establishing the

minimum leverage ratio for banks. There will also be disclosures and related measurement bases for

exposures.

Recovery & resolution planning

The Financial Stability Board is continuing impact studies on Total Loss Absorbency Capacity (TLAC) for G-

SIBs with an expectation of final proposals to be issued in late 2015 for implementation in 2019. Minimum

requirement for eligible liabilities (MREL) is the EU equivalent of TLAC but is not restricted to G-SIBs. The

required amount will be set on a case by case basis by resolution authorities, with the Bank of England

proposing that MREL be aligned to TLAC.