RBS 2014 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

34

RBS – Interim Results 2015

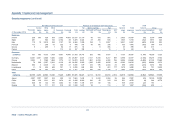

Appendix 1 Capital and risk management

Market risk

Market risk is the risk of losses arising from fluctuations in interest rates, credit spreads, foreign currency rates, equity prices, commodity prices and other factors,

such as market volatilities, that may lead to a reduction in earnings, economic value or both. For a description of market risk framework, governance, policies and

methodologies, refer to Capital and risk management - Market risk in the 2014 Annual Report and Accounts. There were no material changes to market risk

methodologies or models during H1 2015.

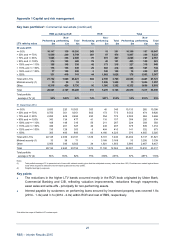

Trading portfolios

Value-at-risk

The table below presents the internal value-at-risk (VaR) for trading portfolios split by type of market risk exposure and by business area. The internal traded 99%

one-day VaR captures all trading book positions. By contrast, the regulatory VaR-based charges take into account only regulator-approved products, locations and

legal entities and are based on a ten-day, rather than a one-day, holding period for market risk capital calculations.

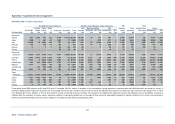

Half year ended Year ended

30 June 2015 30 June 2014 31 December 2014

Average Period end Maximum Minimum Average Period end Maximum Minimum Average Period end Maximum Minimum

Trading VaR (1-day 99%) £m £m £m £m £m £m £m £m £m £m £m £m

Interest rate 16.0 11.7 29.8 10.8 16.7 14.9 39.8 10.9 17.4 16.9 39.8 10.8

Credit spread 12.5 7.6 16.4 7.5 28.3 24.4 42.8 20.9 23.1 14.2 42.8 13.4

Currency 5.3 5.4 7.8 3.3 5.4 3.0 8.5 2.0 4.7 5.5 9.7 1.0

Equity 2.4 1.2 6.1 1.0 3.5 2.5 6.0 2.1 3.0 3.7 6.5 1.2

Commodity 0.5 0.7 2.2 0.2 0.6 0.7 1.4 0.3 0.6 0.4 2.5 0.3

Diversification (1) (11.6) (24.8) (18.2)

Total 21.8 15.0 30.1 15.0 30.6 20.7 58.2 20.7 27.8 22.5 58.2 17.1

CIB 21.1 14.2 29.8 14.0 28.2 21.3 48.8 20.5 26.3 21.3 48.8 15.5

RCR 3.1 2.8 4.5 2.6 6.0 3.5 16.2 3.3 4.5 3.0 16.2 2.6

Note:

(1) RBS benefits from diversification as it reduces risk by allocating positions across various financial instrument types, currencies and markets. The extent of the diversification benefit depends on the correlation between the assets and risk factors in the portfolio at a

particular time. The diversification factor is the sum of the VaR on individual risk types less the total portfolio VaR.

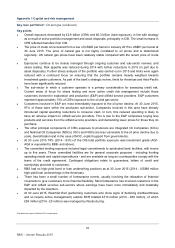

Key points

• During H1 2015, trading book exposure continued to decline. The markets exhibited higher volatility and reduced liquidity, resulting from a number o

f

macroeconomic factors, including ongoing political and economic uncertainty in Europe and growing concerns regarding economic slowdown in China.

• The period end and average total traded internal VaR were lower than in 2014, primarily in credit spread VaR resulting from the ongoing exit of the US asset-

backed products (ABP) trading business.