RBS 2014 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

8

RBS – Interim Results 2015

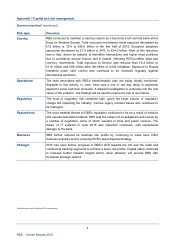

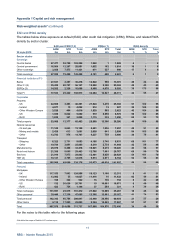

Appendix 1 Capital and risk management

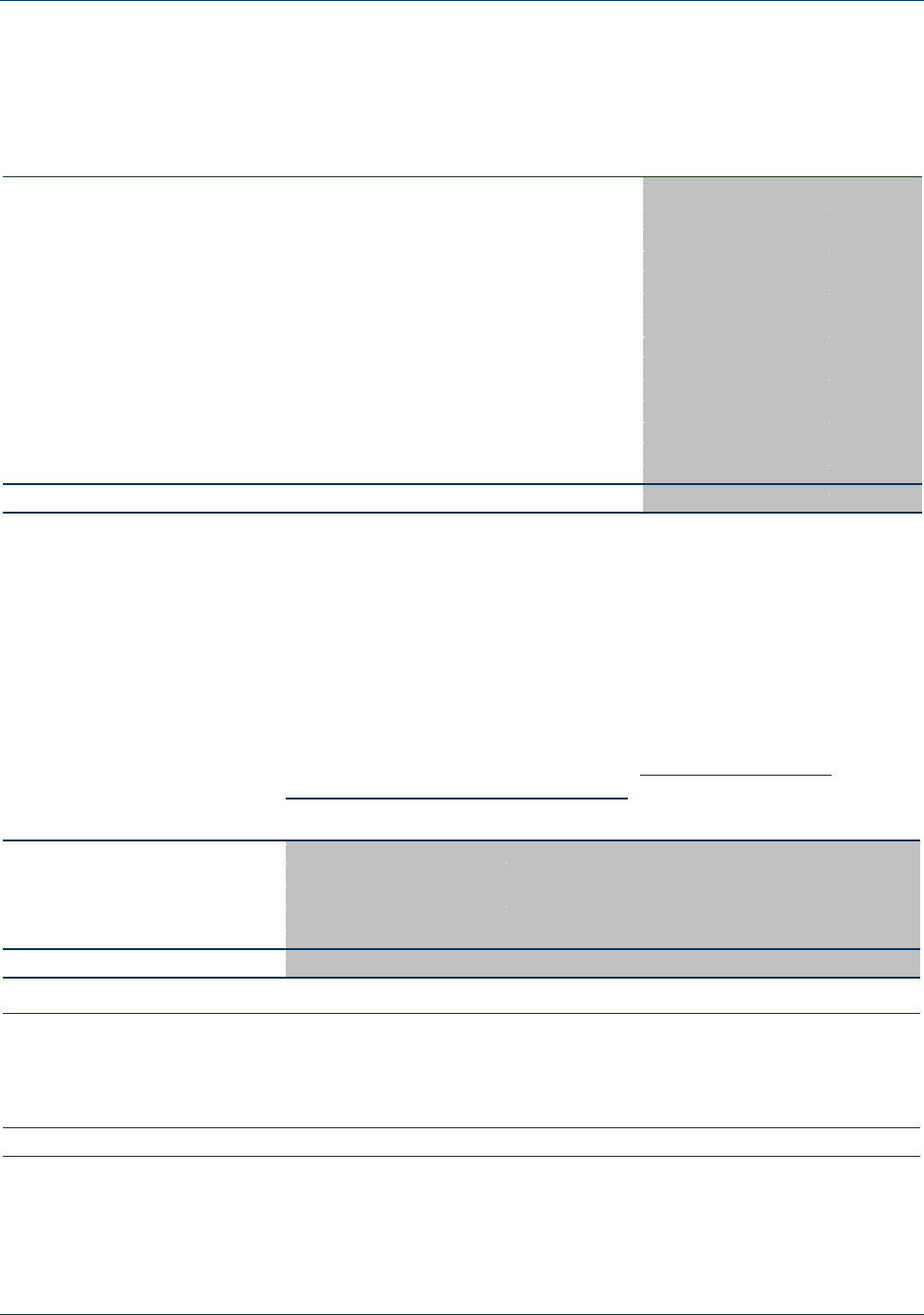

Capital resources (continued)

Capital flow statement*

The table below analyses the movement in end-point CRR CET1 and Tier 2 capital for the half year ended

30 June 2015.

CET1 Tier 2 Total

£m £m £m

A

t 1 January 2015 39,919 8,717 48,636

Loss for the year net of movements in fair value of own credit (308) - (308)

Share capital and reserve movements in respect of employee share schemes 161 - 161

Ordinary shares issued 150 - 150

Foreign exchange reserve (1,166) - (1,166)

A

FS reserves (55) - (55)

Decrease in goodwill and intangibles deduction 583 - 583

Deferred tax assets 16 - 16

Prudential valuation adjustments 18 - 18

Excess of expected loss over impairment provisions 172 - 172

Dated subordinated debt issues/(maturities) - (50) (50)

Net dated subordinated debt/grandfathered instruments - (76) (76)

Foreign exchange movements - (400) (400)

Other movements 563 (10) 553

At 30 June 2015 40,053 8,181 48,234

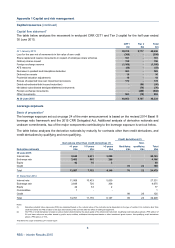

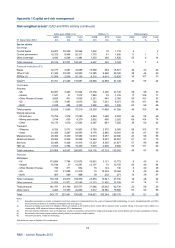

Leverage exposure

Basis of preparation*

The leverage exposure set out on page 24 of the main announcement is based on the revised 2014 Basel III

leverage ratio framework and the 2015 CRR Delegated Act. Additional analysis of derivative notionals and

undrawn commitments, two of the major components contributing to the leverage exposure is set out below.

The table below analyses the derivative notionals by maturity for contracts other than credit derivatives, and

credit derivatives by qualifying and non-qualifying.

Credit derivatives (2)

Derivatives other than credit derivatives (1) Non-

<1 yea

r

1-5 years >5 years Qualifying qualifying Total

Derivative notionals £bn £bn £bn £bn £bn £bn

30 June 2015

Interest rate 9,642 6,631 3,850 20,123

Exchange rate 3,403 505 288 4,196

Equity 42 16 2 60

Credit 78 22 100

Total 13,087 7,152 4,140 78 22 24,479

31 December 2014

Interest rate 11,069 10,423 5,839 27,331

Exchange rate 3,649 720 306 4,675

Equity 42 33 2 77

Commodities 1 -- 1

Credit 99 26 125

Total 14,761 11,176 6,147 99 26 32,209

Notes:

(1) Derivative potential future exposures (PFE) are calculated based on the notional value of the contracts and is dependent on the type of contract. For contracts other than

credit derivatives the PFE is based on the type and maturity of the contract after the effect of netting arrangements.

(2) The PFE on credit derivatives is based on add-on factors determined by the asset quality of the referenced instrument. Qualifying credit derivatives attract a PFE add-on o

f

5% and have reference securities issued by public sector entities, multilateral development banks or other investment grade issuers. Non-qualifying credit derivatives

attract a PFE add-on of 10%.

*Not within the scope of Deloitte LLP’s review report