RBS 2014 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

38

RBS – Interim Results 2015

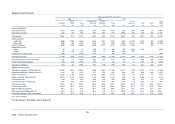

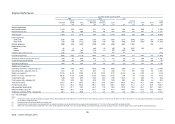

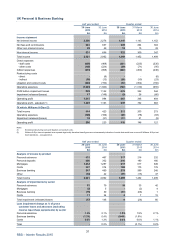

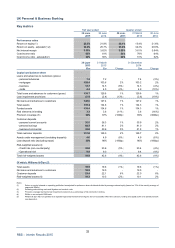

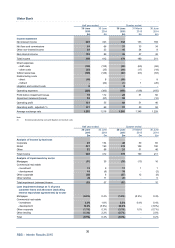

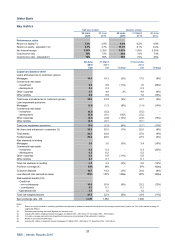

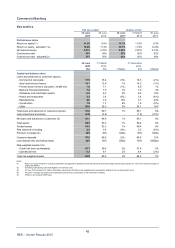

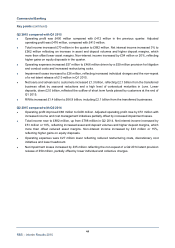

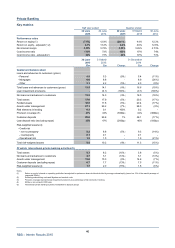

Ulster Bank

Ulster Bank retains a strong capital and funding position as it continues to support the economic recovery

across the island of Ireland. New lending activity increased further during H1 2015 with mortgage drawdowns

up 45% versus H1 2014 and £0.8 billion of new lending made available to business customers, an increase

of 57% from H1 2014. Impairment releases have continued driven by proactive debt management and the

improving economic conditions.

During H1 2015 Ulster Bank continued to make it simpler and easier for customers to do business:

• The launch of the “Mortgage you can live with” campaign offers a range of new product options to both

new and existing mortgage customers including a suite of fixed rate options. The bank has also

introduced a dedicated team of mobile mortgage managers and returned to the mortgage broke

r

market.

• Ulster Bank continues to support Commercial customers and launched new propositions fo

r

businesses operating in the food and drink, agriculture and international business sectors during H1

2015.

• A fully digitalised account opening option was introduced for personal customers in Northern Ireland

as the digital proposition continued to be enhanced. Customers continue to move towards direc

t

channels with over 88% of all transactional activity now outside the traditional branch.

• Significant progress has been made to improve the customer service proposition. The announcement

of a new partnership with ‘An Post’ in the Republic of Ireland will provide customers with 1,140 new

points of presence. The bank’s award winning customer contact centre announced 350 new jobs

which will handle customer calls across a number of RBS brands.

• The launch of a set of customer commitments specifically designed to support customers in arrears on

their home loan has been positively received by the market.

A significant weakening in the euro relative to sterling during H1 2015 had a material impact on Ulster Bank’s

financial performance as reported and in comparison to prior periods.

H1 2015 compared with H1 2014

• Operating profit increased by £76 million to £131 million for H1 2015 with the benefit of net impairment

releases. Adjusted operating profit was £141 million for H1 2015, compared with a profit of £69 million

for H1 2014. The reduction in profit before impairment losses to £79 million is partly attributable to a

weakening of the euro, (an impact of £17 million), a decrease in income on free funds and an increase

in pension servicing costs. Return on equity increased 5.1 percentage points to 8%.

• Total income decreased by £44 million primarily driven by the weakening of the euro (an impact of £33

million) and a lower return on free funds. While deposit pricing improved steadily and loan margins

remained stable in a competitive market, the net interest margin of 1.94% reflected the lower return on

free funds and the impact of liquidity management requirements. The offsetting income movements

between the Corporate and Retail businesses primarily reflect a transfer of management responsibility

for a specific business channel to align with the bank’s distribution strategy.

• Operating expenses decreased by £11 million to £289 million principally from a reduction in headcount

and the property footprint coupled with a benefit from the weakening of the euro (an impact of £16

million), offset partly by higher pensions charges and investment in technology and infrastructure.

•

A

net impairment release of £52 million for H1 2015 reflected the benefits of proactive debt

management and improving macroeconomic conditions.