RBS 2014 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

23

RBS – Interim Results 2015

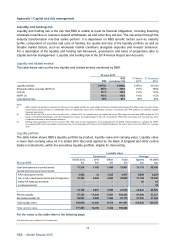

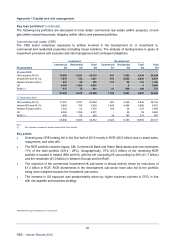

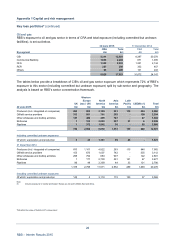

Appendix 1 Capital and risk management

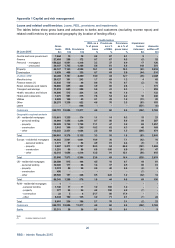

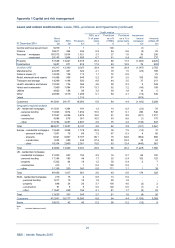

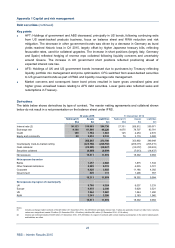

Debt securities (continued)

Key points

• HFT: Holdings of government and ABS decreased, principally in US bonds, following continuing exits

from US asset-backed products business, focus on balance sheet and RWA reduction and risk

mitigation. The decrease in other government bonds was driven by a decrease in Germany as bund

yields reached historic lows in Q1 2015, largely offset by higher Japanese treasury bills, reflecting

favourable rates, used for collateral upgrades. The increase in short positions (largely Italy, German

y

and Spain) reflected hedging of reverse repo collateral following liquidity concerns and uncertaint

y

around Greece. The increase in UK government short positions reflected positioning ahead o

f

expected interest rate rise.

•

A

FS: Holdings of UK and US government bonds increased due to purchases by Treasury reflecting

liquidity portfolio mix management and price optimisation. CFG switched from asset-backed securities

to US government bonds as part of RWA and liquidity coverage ratio management.

• Market concerns and consequent lower bond prices resulted in lower gross unrealised gains and

higher gross unrealised losses relating to AFS debt securities. Lower gains also reflected sales and

redemptions in Treasury.

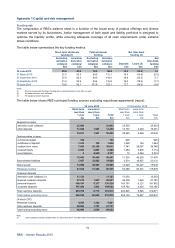

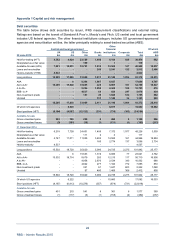

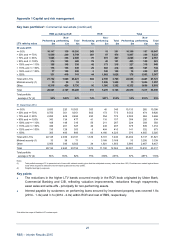

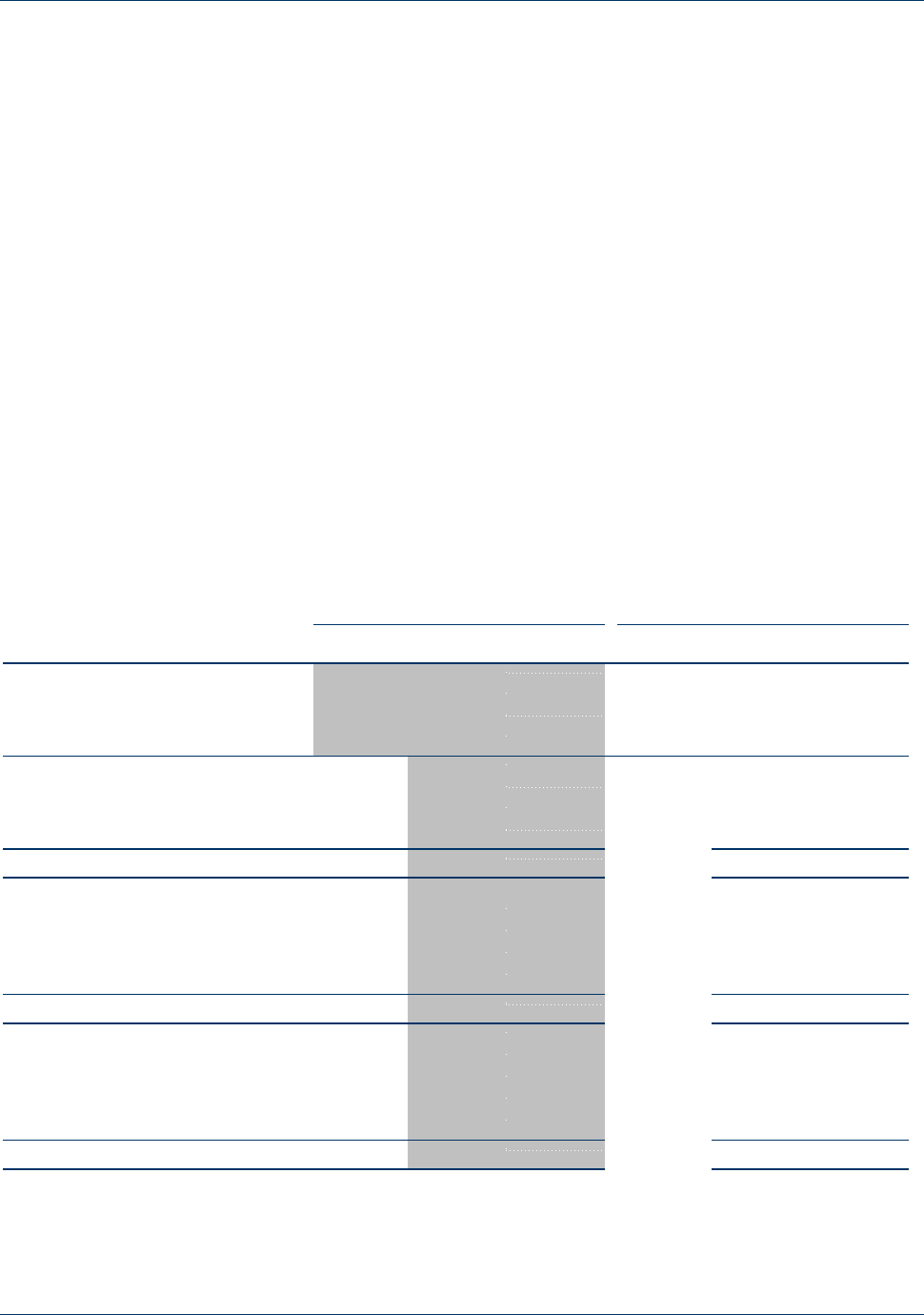

Derivatives

The table below shows derivatives by type of contract. The master netting agreements and collateral shown

below do not result in a net presentation on the balance sheet under IFRS.

30 June 2015 31 December 2014

Notional (1)

A

ssets Liabilities Notional (1) Assets Liabilities

£bn £m £m £bn £m £m

Interest rate (2) 20,123 216,983 204,738 27,331 269,912 259,971

Exchange rate 4,196 61,566 65,228 4,675 78,707 83,781

Credit 100 1,704 1,681 125 2,254 2,615

Equity and commodity 60 2,032 2,133 78 3,119 3,582

282,285 273,780 353,992 349,949

Counterparty mark-to-market netting (228,780) (228,780) (295,315) (295,315)

Cash collateral (28,295) (25,627) (33,272) (30,203)

Securities collateral (6,999) (8,299) (7,013) (14,437)

Net exposure 18,211 11,074 18,392 9,994

Net exposure by sector

Banks 1,357 2,065 1,875 1,534

Other financial institutions 6,205 5,313 4,035 3,721

Corporate 9,820 3,585 11,186 4,382

Government 829 111 1,296 357

18,211 11,074 18,392 9,994

Net exposure by region of counterparty

UK 9,708 4,524 9,037 3,233

Europe 4,818 2,395 5,628 3,521

US 1,344 1,867 1,544 1,280

RoW 2,341 2,288 2,183 1,960

18,211 11,074 18,392 9,994

Notes:

(1) Includes exchange traded contracts of £2,620 billion (31 December 2014 - £2,436 billion) principally interest rate. Trades are generally closed out daily hence carrying

values were insignificant; assets £3 million (31 December 2014 - £8 million); liabilities £81 million (31 December 2014 - £119 million).

(2) Interest rate notional includes £12,007 billion (31 December 2014 - £18,452 billion) in respect of contracts with central clearing counterparties to the extent related assets

and liabilities are offset.