RBS 2014 Annual Report Download - page 171

Download and view the complete annual report

Please find page 171 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

36

RBS – Interim Results 2015

Appendix 1 Capital and risk management

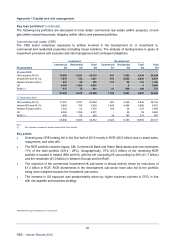

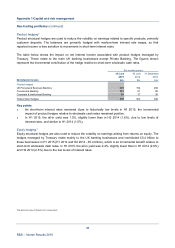

Non-trading portfolios

Non-trading VaR

Average VaR for RBS’s non-trading book, comprising predominantly available-for-sale portfolios, was £2.9

million for H1 2015 compared with £4.8 million for H1 2014 and £4.4 million for H2 2014. This was largely

driven by a decline in the credit spread VaR as a result of the ongoing RCR run-down. The period end VaR

decreased from £3.8 million at 31 December 2014 to £2.0 million at 30 June 2015.

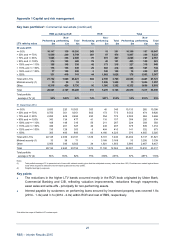

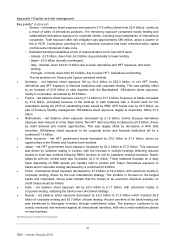

Non-traded interest rate risk

Non-traded interest rate risk affects earnings arising from banking activities. This excludes positions in

financial instruments which are classified as held-for-trading. The methodology relating to interest rate risk is

detailed in Capital and risk management - Market risk - Non-traded market risk in the 2014 Annual Report

and Accounts.

Non-traded interest rate risk VaR metrics are based on interest rate repricing gaps at the reporting date. The

table below captures the risk resulting from mismatches in the repricing dates of assets and liabilities. This

includes any mismatch between structural hedges and stable non and low interest bearing liabilities such as

equity and money transmission accounts as regards their interest rate repricing behavioural profile. Other

customer products and associated funding and hedging transactions as well as non-financial assets and

liabilities such as property, plant and equipment are also included.

VaR does not provide a dynamic measurement of interest rate risk since static underlying repricing gap

positions are assumed. Changes in customer behaviour under varying interest rate scenarios are captured

by way of earnings at risk measures. VaR relating to non-traded interest rate risk for RBS’s retail and

commercial banking activities at a 99% confidence level and a currency analysis at the period end were as

follows:

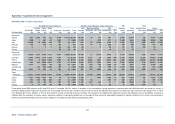

Average Period end Maximum Minimum

Six months ended £m £m £m £m

30 June 2015 17 13 25 11

30 June 2014 64 68 79 45

31 December 2014 37 23 56 23

30 June 30 June 31 Decembe

r

2015 2014 2014

£m £m £m

Euro 2 3 2

Sterling 13 8 12

US dollar 14 73 27

Other 4 3 3

Key point

• In H1 2015, interest rate VaR was lower on average than in 2014 as RBS continued to steer its

structural interest rate exposure more closely to the neutral duration prescribed in its risk management

policy. The reduction in the US dollar VaR reflects reduced exposure to US dollar fixed rate assets,

which helped to achieve the alignment to policy.