RBS 2014 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199

|

|

2

RBS – Interim Results 2015

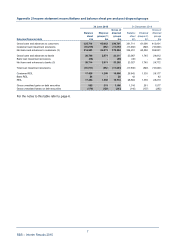

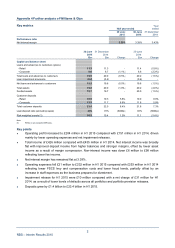

Appendix 4 Further analysis of Williams & Glyn

Key metrics Yea

r

Half year ended Half year ended ended

30 June 30 June 31 Decembe

r

2015 2014 2014

Performance ratio

Net interest margin 3.39% 3.39% 3.43%

30 June 31 Decembe

r

30 June

2015 2014 2014

£bn £bn Change £bn Change

Capital and balance sheet

Loans and advances to customers (gross)

- Retail 11.3 11.3 - 11.4 (0.9%)

- Corporate 8.6 8.7 (1.1%) 8.8 (2.3%)

Total loans and advances to customers 19.9 20.0 (0.5%) 20.2 (1.5%)

Loan impairment provisions (0.4) (0.4) - (0.4) -

Net loans and advances to customers 19.5 19.6 (0.5%) 19.8 (1.5%)

Total assets 19.8 20.0 (1.0%) 20.2 (2.0%)

Funded assets 19.7 19.7 - 20.0 (1.5%)

Customer deposits

- Retail 10.9 10.3 5.8% 10.0 9.0%

- Corporate 12.5 11.7 6.8% 11.8 5.9%

Total customer deposits 23.4 22.0 6.4% 21.8 7.3%

Loan:deposit ratio (excluding repos) 85% 91% (600bp) 93% (800bp)

Risk-weighted assets (1) 10.5 10.4 1.0% 11.1 (5.4%)

Note:

(1) RWAs on an end-point CRR basis.

Key points

• Operating profit increased to £204 million in H1 2015 compared with £151 million in H1 2014, driven

mainly by lower operating expenses and net impairment releases.

• Total income of £426 million compared with £435 million in H1 2014. Net interest income was broadly

flat with improved deposit income from higher balances and stronger margins, offset by lower asset

income as a result of margin compression. Non-interest income was down £6 million to £98 million

reflecting lower fee income.

• Net interest margin has remained flat at 3.39%.

• Operating expenses fell £21 million to £232 million in H1 2015 compared with £253 million in H1 2014

reflecting lower FSCS levy and compensation costs and lower fraud levels, partially offset by an

increase in staff expenses as the business prepares for divestment.

• Impairment release for H1 2015 were £10 million compared with a net charge of £31 million for H1

2014, as a result of lower levels of defaults across all portfolios and portfolio provision releases.

• Deposits grew by £1.4 billion to £23.4 billion in H1 2015.