RBS 2014 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

25

RBS – Interim Results 2015

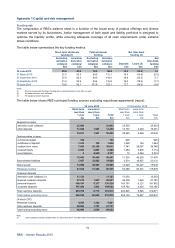

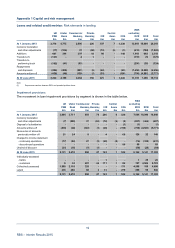

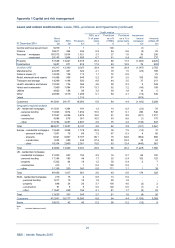

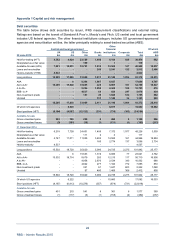

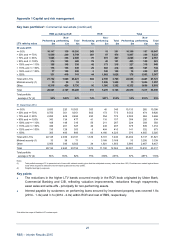

Appendix 1 Capital and risk management

Key loan portfolios*

The internal measure used for credit risk management is credit risk assets (CRA) and consists of lending,

derivatives after the effect of enforceable netting arrangements and contingent obligations.

The table below summarises CRA by sector and geographic region.

Wholesale

Banks and Natural Retail and Of which:

Personal other FIs Sovereign Property resources leisure Othe

r

Total RCR

30 June 2015 £m £m £m £m £m £m £m £m £m

UK 130,302 25,382 50,922 39,438 8,099 14,618 40,062 308,823 7,168

Western Europe (excl. UK) 15,113 33,644 11,025 7,523 3,232 2,418 11,485 84,440 6,241

North America 33,113 12,779 22,465 7,308 5,057 5,945 19,892 106,559 556

RoW (1) 3,383 9,916 3,599 1,511 3,703 597 11,933 34,642 2,936

Total 181,911 81,721 88,011 55,780 20,091 23,578 83,372 534,464 16,901

of which: RCR 90 2,621 30 7,458 2,746 796 3,160 16,901 n/a

Flow into forbearance (2) 1,625 88 - 1,934 412 454 902 5,415 1,420

of which: RCR - 11 - 1,060 36 145 168 1,420 n/a

A

Q10 7,477 715 1 8,003 258 1,278 2,397 20,129 7,662

of which: RCR 75 304 - 5,540 150 483 1,110 7,662 n/a

31 December 2014

UK 129,091 27,560 45,308 44,401 7,825 15,539 40,199 309,923 11,579

Western Europe (excl. UK) 16,802 37,156 6,855 11,858 4,030 3,221 13,162 93,084 12,159

North America 32,449 13,367 27,162 6,846 7,070 5,736 21,642 114,272 851

RoW (1) 2,406 13,406 3,039 1,875 5,685 1,188 17,187 44,786 5,061

Total 180,748 91,489 82,364 64,980 24,610 25,684 92,190 562,065 29,650

of which: RCR 203 3,587 536 14,819 2,910 1,828 5,767 29,650 n/a

Flow into forbearance (2) 4,350 60 - 5,416 377 984 1,956 13,143 4,839

of which: RCR - 29 - 3,551 28 535 696 4,839 n/a

A

Q10 8,424 638 1 14,743 263 2,329 3,662 30,060 16,099

of which: RCR 182 423 - 11,886 112 1,355 2,141 16,099 n/a

Notes:

(1) Rest of World comprises Asia Pacific, Central and Eastern Europe, the Middle East, Central Asia and Africa, and supranationals such as the World Bank.

(2) Completed during the period.

Key points

• The CRA decrease reflected a continued focus on risk reduction and improving overall credit quality.

• CRA decreased in all regions and sectors except sovereign where CRA increased by 7%, reflecting

Treasury activity. UK CRA (excluding RCR) increased by 1%, in personal (mainly mortgage lending).

• For wholesale loans, the flow into forbearance decreased during H1 2015 compared with H2 2014 in

line with improving market conditions and RCR’s disposal strategy. Of the total forbearance granted,

54% related to non-performing loans with a provision coverage of 48% (2014 - 62%).

• The property sector remained the most significant contributor to the forborne portfolio. There was an

increase in forbearance granted in the natural resources sector driven by counterparties in the oil and

gas sector (refer to page 28 for further sector information).

• RCR is on track to complete its targeted run-down by the end of 2015, with CRA down by 43% to

£16.9 billion. Non-performing exposures decreased significantly to £7.7 billion (2014 - £16.1 billion)

driven by the disposal strategy and the improving economic climate.

*Not within the scope of Deloitte LLP’s review report