RBS 2014 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

13

RBS – Interim Results 2015

Appendix 1 Capital and risk management

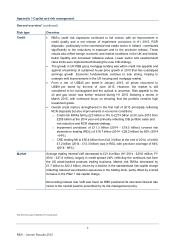

Liquidity and funding risk

Liquidity and funding risk is the risk that RBS is unable to meet its financial obligations, including financing

wholesale maturities or customer deposit withdrawals, as and when they fall due. The risk arises through the

maturity transformation role that banks perform. It is dependent on RBS specific factors such as maturity

profile, composition of sources and uses of funding, the quality and size of the liquidity portfolio as well as

broader market factors, such as wholesale market conditions alongside depositor and investor behaviour.

For a description of the liquidity and funding risk framework, governance and basis of preparation refer to

Capital and risk management - Liquidity and funding risk in the 2014 Annual Report and Accounts.

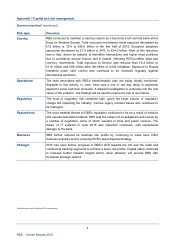

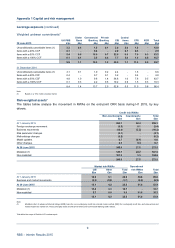

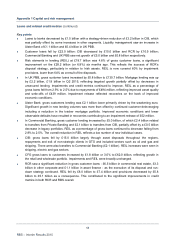

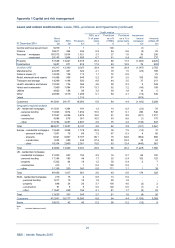

Liquidity and related metrics*

The table below sets out the key liquidity and related metrics monitored by RBS.

30 June 2015

RBS 31 March 31 Decembe

r

RBS excluding CFG 2015 2014

Liquidity portfolio £161bn £148bn £157bn £151bn

Stressed outflow coverage (SCR) (1) 215% 235% 187% 186%

LCR (2) 117% 118% 112% 112%

NSFR (3) 115% 112% 110% 112%

Loan:deposit ratio 92% 91% 95% 95%

Notes:

(1) RBS's liquidity risk appetite is measured by reference to the liquidity portfolio as a percentage of stressed contractual and behavioural outflows under the worst of three

internal severe stress scenarios (a market-wide stress, an idiosyncratic stress and a combination of both) in accordance with PRA guidance on Individual Liquidity

Adequacy Assessment.

(2) Within the EU, the LCR is due to come into effect from 1 October 2015 on a phased basis, and replace the current PRA regime from this date. RBS monitors the LCR

based on its internal interpretations of the EU Delegated Act rules for the implementation of the LCR. Consequently, RBS’s ratio may change over time and may not be

comparable with those of other financial institutions.

(3) Pending further guidelines from the EU and the PRA, RBS uses its own interpretation of the proposals from the BCBS recommendations to calculate the NSFR.

Consequently RBS’s ratio may change over time and may not be comparable with those of other financial institutions. The ratio is due to come into effect from 1 Januar

y

2018.

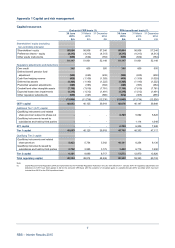

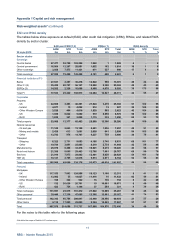

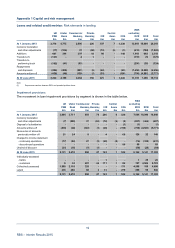

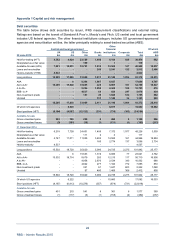

Liquidity portfolio

The table below shows RBS’s liquidity portfolio by product, liquidity value and carrying value. Liquidity value

is lower than carrying value as it is stated after discounts applied by the Bank of England and other central

banks to instruments, within the secondary liquidity portfolio, eligible for discounting.

Liquidity value

Period end Average

UK DLG (1) CFG Other Total Quarte

r

H1 2015

30 June 2015 £m £m £m £m £m £m

Cash and balances at central banks 73,218 1,183 1,406 75,807 71,113 66,392

Central and local government bonds

AAA rated governments 3,932 12 1,033 4,977 5,609 6,529

AA- to AA+ rated governments and US agencies 10,202 9,845 2,852 22,899 21,154 20,285

Below AA rated governments - - -- 80 91

Local government - - -- - 24

14,134 9,857 3,885 27,876 26,843 26,929

Primary liquidity 87,352 11,040 5,291 103,683 97,956 93,321

Secondary liquidity (2) 54,667 2,085 1,022 57,774 57,586 57,024

Total liquidity value 142,019 13,125 6,313 161,457 155,542 150,345

Total carrying value 177,485 14,199 7,262 198,946

For the notes to this table refer to the following page.

*Not within the scope of Deloitte LLP’s review report