RBS 2014 Annual Report Download - page 175

Download and view the complete annual report

Please find page 175 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

40

RBS – Interim Results 2015

Appendix 1 Capital and risk management

Country risk

Country risk is the risk of losses occurring as a result of either a country event or unfavourable country

operating conditions. As country events may simultaneously affect all or many individual exposures to a

country, country event risk is a concentration risk. Refer to Capital and risk management - Credit risk in the

2014 Annual Report and Accounts for other types of concentration risk such as product, sector or single-

name concentration and Country risk for governance, monitoring, management and definitions.

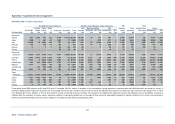

Key points*

The comments below relate to changes in country exposures in H1 2015 unless indicated otherwise.

● Net balance sheet and off-balance sheet exposure to most countries declined across most products.

RBS continues to maintain a cautious stance as it becomes a more UK-centred bank with an

international focus on Western Europe. In addition, many clients continued to reduce debt levels. The

US dollar and the euro depreciated against sterling by 0.7% and 8.9% respectively, contributing to the

decline in exposure.

● Total eurozone net balance sheet exposure decreased by £12.0 billion or 12%, to £85.6 billion.

○ The depreciation of the euro played a significant role in the reduction.

○ The main reductions were in HFT government bonds in Germany, Italy and Spain; in derivatives

exposure (mostly to banks) in the Netherlands, Italy and Germany; and in lending in Ireland, Italy

and Spain.

○ Notional bought and sold credit default swaps (CDS) continued its downward trend in line with the

bank’s general reduction in trading. Net bought CDS protection on eurozone exposures was

broadly unchanged.

○ Net lending in RCR roughly halved to £2.0 billion for the eurozone as a whole, including £0.8 billion

in Ireland and £0.5 billion in Spain, with CRE accounting for broadly half of the total.

● Eurozone periphery net balance sheet exposure decreased by £7.4 billion or 24%, to £24.0 billion.

○ Ireland - exposure fell by £2.5 billion or 11% to £20.2 billion, with exposure to corporates and

households (mostly mortgage lending) decreasing by £1.5 billion each, largely reflecting currency

movements and portfolio sales in RCR. Provisions fell by £3.3 billion to £5.1 billion, largely as a

result of these sales. Ulster Bank’s cash deposits with the Central Bank of Ireland increased by

£0.7 billion, again reflecting the proceeds of the RCR portfolio sales.

○ Spain - exposure decreased by £1.2 billion to £2.1 billion. This largely reflected reductions in net

HFT government bonds, the result of client demand and perceived peripheral eurozone risks

triggered by the Greek crisis, and corporate lending (mostly RCR exposure to the commercial real

estate, construction and transport sectors). Off-balance sheet exposure, mostly to corporates,

decreased by £0.5 billion.

○ Italy - exposure fell by £3.2 billion to £1.1 billion, reflecting reductions in net HFT government

bonds, driven by client demand and eurozone risks, and the maturity of a few large derivatives

transactions with banks and corporate loans. Off-balance sheet exposure, largely to corporate

clients, decreased by £0.7 billion. RBS will continue to service core clients in Italy.

○ Portugal - exposure decreased by £0.3 billion to £0.5 billion, due to decreases in net HFT

government bonds, derivatives to banks and corporate lending.

*Not within the scope of Deloitte LLP’s review report