RBS 2014 Annual Report Download - page 170

Download and view the complete annual report

Please find page 170 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

35

RBS – Interim Results 2015

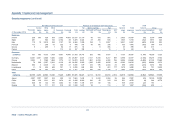

Appendix 1 Capital and risk management

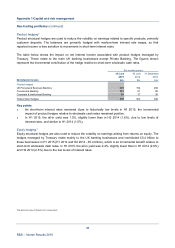

Trading portfolios (continued)

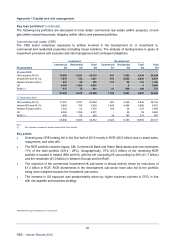

Capital charges*

The total market risk minimum capital requirement calculated in accordance with CRR was £1,786 million at

30 June 2015 (31 December 2014 - £1,917 million), representing RWAs of £22.3 billion (31 December 2014

- £24.0 billion). It comprised two categories: (i) the Pillar 1 model-based position risk requirement (PRR) of

£1,497 million (31 December 2014 - £1,458 million), which in turn comprised several modelled charges; and

(ii) the standardised PRR of £289 million (31 December 2014 - £459 million), which also had several

components.

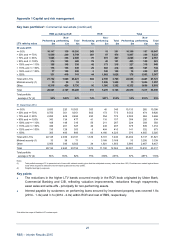

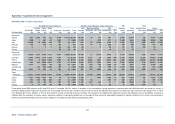

The components of the Pillar 1 model-based PRR are presented in the table below.

31 Decembe

r

2014

Average Maximum Minimum Period end Period end

30 June 2015 £m £m £m £m £m

Value-at-risk 362 400 333 400 329

Stressed VaR (SVaR) 527 555 492 555 511

Incremental risk charge (IRC) 294 348 271 288 299

Risk not in VaR (RNIV) 284 319 227 254 319

1,497 1,458

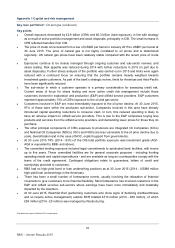

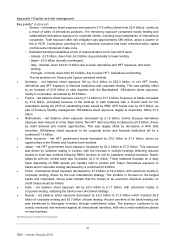

Key points

• The total model-based PRR increased by 3% in the half year to 30 June 2015, driven by higher VaR

and SVaR based capital charges, offset somewhat by the lower RNIV capital charge.

• The VaR and SVaR capital charges together increased by 14%, reflecting increased positioning by the

rates business during Q2 2015, notably relating to euro rates, following market euro sell-off in May.

• The RNIV charge fell by 20%, primarily in stressed RNIVs following reductions in inflation basis risk in

the rates business.

• Standardised charges were 37% or £170 million lower than at the 2014 year end, primarily driven by

reduced securitisation exposures in the trading book reflecting the continuation of the US ABP exit, UK

ABP risk reduction and the continuation of RCR disposals.

• All entities maintained a green status relating to regulatory back-testing during H1 2015 except fo

r

NatWest Plc, which had six exceptions during the 250 business days ending 30 June 2015, mainly

driven by market volatility. This resulted in a £49 million increase to market risk RWAs.

*Not within the scope of Deloitte LLP’s review report