RBS 2014 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

26

RBS – Interim Results 2015

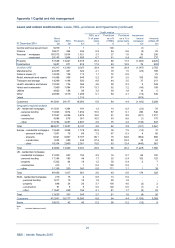

Appendix 1 Capital and risk management

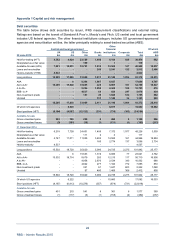

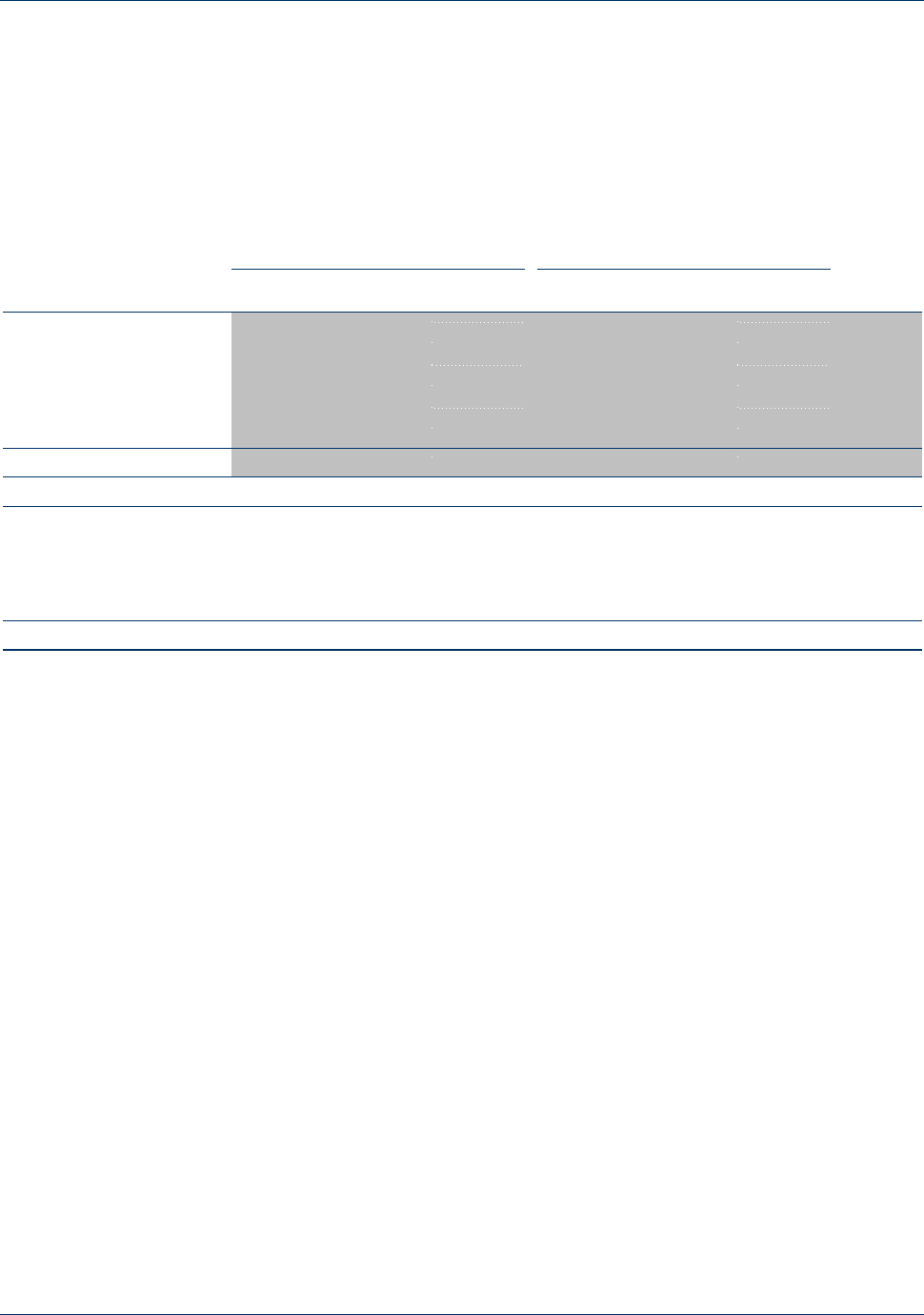

Key loan portfolios* (continued)

The following key portfolios are discussed in more detail: commercial real estate (within property); oil and

gas (within natural resources); shipping (within other); and personal portfolios.

Commercial real estate (CRE)

The CRE sector comprises exposures to entities involved in the development of, or investment in,

commercial and residential properties (including house builders). The analysis of lending below is gross of

impairment provisions and excludes rate risk management and contingent obligations

Investment Development

Commercial Residential Total Commercial Residential Total Total

By geography £m £m £m £m £m £m £m

30 June 2015

UK (excluding NI (1)) 15,959 4,351 20,310 541 3,393 3,934 24,244

Ireland (ROI and NI (1)) 1,519 312 1,831 614 2,022 2,636 4,467

Western Europe (other) 947 29 976 110 22 132 1,108

US 4,489 1,362 5,851 - 5 5 5,856

RoW (1) 415 16 431 41 249 290 721

23,329 6,070 29,399 1,306 5,691 6,997 36,396

31 December 2014

UK (excluding NI (1)) 17,327 4,757 22,084 600 3,446 4,046 26,130

Ireland (ROI and NI (1)) 2,864 740 3,604 1,499 4,469 5,968 9,572

Western Europe (other) 1,222 53 1,275 189 24 213 1,488

US 4,063 1,358 5,421 - 59 59 5,480

RoW (1) 406 22 428 34 185 219 647

25,882 6,930 32,812 2,322 8,183 10,505 43,317

Note:

(1) ROI: Republic of Ireland; NI: Northern Ireland; RoW: Rest of World.

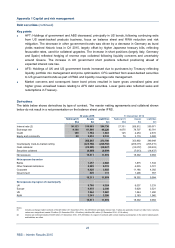

Key points

• Overall gross CRE lending fell in the first half of 2015 mostly in RCR (£6.5 billion) due to asset sales,

repayments, and write-offs.

• The RCR portfolio contains legacy CIB, Commercial Bank and Ulster Bank assets and now represents

17% of the total portfolio (2014 - 29%). Geographically, 57% (£3.5 billion) of the remaining RCR

portfolio is located in Ireland (ROI and NI), with the UK (excluding NI) accounting for 28% (£1.7 billion)

and the remainder (£1.0 billion) in Western Europe and the RoW.

• The reduction of the commercial investment UK sub-sector is almost entirely driven by reductions o

f

£1.3 billion in RCR. RCR divestments in the development sub-sector have also led to the portfolio

being more weighted towards the investment sub-sector.

• The increase in US exposure was predominantly driven by higher business volumes in CFG, in line

with risk appetite and business strategy.

*Not within the scope of Deloitte LLP’s review report