RBS 2014 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2014 RBS annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

|

|

58

RBS – Interim Results 2015

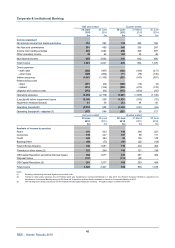

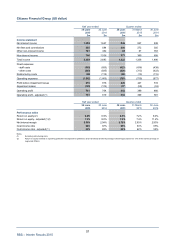

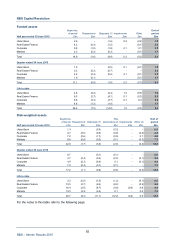

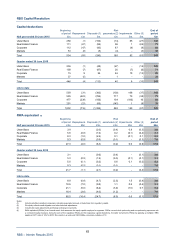

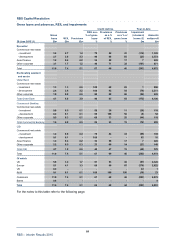

Citizens Financial Group (US dollar)

30 June 31 March 31 Decembe

r

2015 2015 2014

$bn $bn Change $bn Change

Capital and balance sheet

Loans and advances to customers (gross) 97.3 94.9 3% 93.9 4%

Loan impairment provisions (0.8) (0.8) - (0.8) -

Net loans and advances to customers 96.5 94.1 3% 93.1 4%

Total assets 137.0 136.3 1% 132.6 3%

Funded assets 136.4 135.6 1% 132.0 3%

Investment securities 25.1 25.1 - 24.7 2%

Risk elements in lending 1.9 2.0 (5%) 2.1 (10%)

Provision coverage (1) 43% 41% 200bp 40% 300bp

Customer deposits (excluding repos) 100.3 97.7 3% 94.6 6%

Bank deposits (excluding repos) 7.0 7.6 (8%) 8.0 (13%)

Loan:deposit ratio (excluding repos) 96% 96% -98% (200bp)

Risk-weighted assets (2)

- Credit risk

- non-counterparty 100.5 98.1 2% 97.4 3%

- counterparty 1.5 1.5 - 1.4 7%

- Operational risk 7.7 7.3 5% 8.0 (4%)

Total risk-weighted assets 109.7 106.9 3% 106.8 3%

Notes:

(1) Provision coverage represents loan impairment provisions as a percentage of risk elements in lending.

(2) RWAs on an end-point CRR basis.

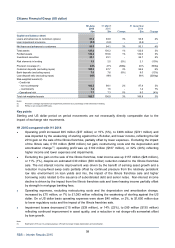

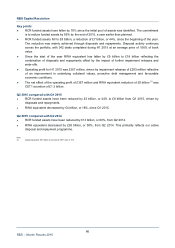

Key points

Sterling and US dollar period on period movements are not necessarily directly comparable due to the

impact of exchange rate movements.

H1 2015 compared with H1 2014

• Operating profit increased £65 million ($37 million) or 15% (5%), to £486 million ($741 million) and

was impacted by the weakening of sterling against the US dollar, and lower income, reflecting the Q2

2014 gain on the sale of the Illinois franchise, partially offset by lower expenses. Excluding the impact

of the Illinois sale, £170 million ($283 million) net gain, restructuring costs and the depreciation and

amortisation change(1), operating profit was up £102 million ($107 million), or 32% (20%) reflecting

higher income and lower expenses and impairments.

• Excluding the gain on the sale of the Illinois franchise, total income was up £157 million ($28 million),

or 11% (1%), despite an estimated £30 million ($50 million) reduction related to the Illinois franchise

sale. The net interest income improvement was driven by the benefit of earning asset growth and a

reduction in pay-fixed swap costs partially offset by continued pressure from the relatively persistent

low rate environment on loan yields and mix, the impact of the Illinois franchise sale and highe

r

borrowing costs related to the issuance of subordinated debt and senior notes. Non-interest income

decline is driven by the impact from the Illinois franchise sale and lower leasing income partially offset

by strength in mortgage banking fees.

• Operating expenses, excluding restructuring costs and the depreciation and amortisation change,

increased by £70 million, or 7% to £1,083 million reflecting the weakening of sterling against the US

dollar. On a US dollar basis operating expenses were down $40 million, or 2%, to $1,650 million due

to lower regulatory costs and the impact of the Illinois franchise sale.

• Impairment losses decreased £15 million ($39 million), or 14% (22%), to £89 million ($135 million)

reflecting continued improvement in asset quality, and a reduction in net charge-offs somewhat offse

t

by loan growth.

Note:

(1) Starting Q1 2015, as it is a disposal group, CFG will no longer charge depreciation and amortisation.