Regions Bank 2012 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

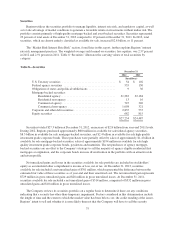

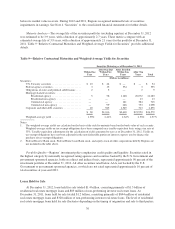

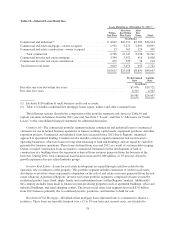

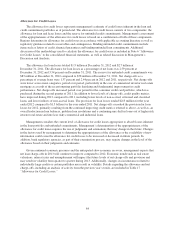

Allowance for Credit Losses

The allowance for credit losses represents management’s estimate of credit losses inherent in the loan and

credit commitment portfolios as of period-end. The allowance for credit losses consists of two components: the

allowance for loan and lease losses and the reserve for unfunded credit commitments. Management’s assessment

of the appropriateness of the allowance for credit losses is based on a combination of both of these components.

Regions determines its allowance for credit losses in accordance with applicable accounting literature as well as

regulatory guidance related to receivables and contingencies. Binding unfunded credit commitments include

items such as letters of credit, financial guarantees and binding unfunded loan commitments. Additional

discussion of the methodology used to calculate the allowance for credit losses is included in Note 6 “Allowance

for Credit Losses” to the consolidated financial statements, as well as related discussion in Management’s

Discussion and Analysis.

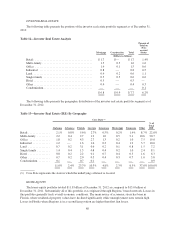

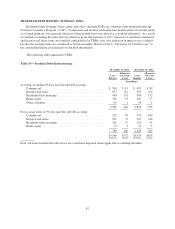

The allowance for loan losses totaled $1.9 billion at December 31, 2012 and $2.7 billion at

December 31, 2011. The allowance for loan losses as a percentage of net loans was 2.59 percent at

December 31, 2012 and 3.54 percent on December 31, 2011. The reserve for unfunded credit commitments was

$83 million at December 31, 2012 compared to $78 million at December 31, 2011. Net charge-offs as a

percentage of average loans were 1.37 percent and 2.44 percent in 2012 and 2011, respectively. Net charge-offs

were lower across most categories, period over period, particularly in the case of commercial investor real estate

mortgage as a result of the recent ongoing portfolio derisking and fundamental improvement in credit

performance. Net charge-offs increased period over period for the consumer credit card portfolio, which was

purchased during the second quarter of 2011. In addition to lower levels of charge-offs, credit quality metrics

have improved during 2012 compared to 2011, including lower levels of non-accrual, criticized and classified

loans, and lower inflows of non-accrual loans. The provision for loan losses totaled $213 million for the year

ended 2012 compared to $1.5 billion for the year ended 2011. Net charge-offs exceeded the provision for loan

losses for 2012, primarily resulting from the continued improving credit metrics referred to above, as well as, an

overall reduction in loan balances, problem loan resolutions and a continuing mix shift in loans out of higher risk

investor real estate and into less risky commercial and industrial loans.

Management considers the current level of allowance for credit losses appropriate to absorb losses inherent

in the loan portfolio and unfunded commitments. Management’s determination of the appropriateness of the

allowance for credit losses requires the use of judgments and estimations that may change in the future. Changes

in the factors used by management to determine the appropriateness of the allowance or the availability of new

information could cause the allowance for credit losses to be increased or decreased in future periods. In

addition, bank regulatory agencies, as part of their examination process, may require changes in the level of the

allowance based on their judgments and estimates.

Given continued economic pressures and the anticipated slow economic recovery, management expects that

net loan charge-offs in 2013 will continue to improve compared to 2012. Economic trends such as real estate

valuations, interest rates and unemployment will impact the future levels of net charge-offs and provision and

may result in volatility from quarter to quarter during 2013. Additionally, changes in circumstances related to

individually large credits or certain portfolios may result in volatility. Details regarding the allowance and net

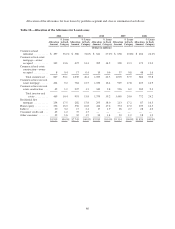

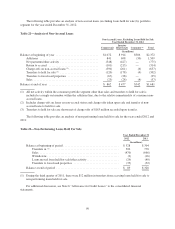

charge-offs, including an analysis of activity from the previous year’s totals, are included in Table 17

“Allowance for Credit Losses.”

84