Regions Bank 2012 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

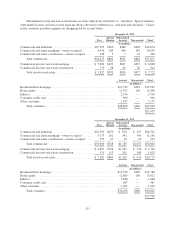

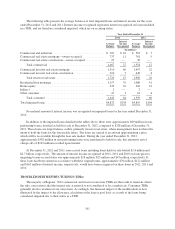

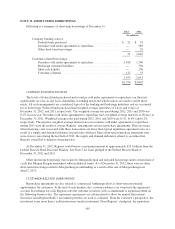

The table below presents an analysis of mortgage servicing rights for the years ended December 31 under

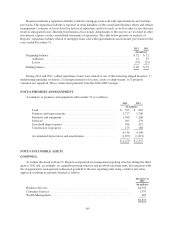

the fair value measurement method:

2012 2011

(In millions)

Carrying value, beginning of period ....................................... $182 $ 267

Additions ........................................................ 60 62

Decrease in fair value:

Due to change in valuation inputs or assumptions .................... (20) (124)

Economic amortization associated with borrower repayments ........... (31) (23)

Carrying value, end of period ............................................ $191 $ 182

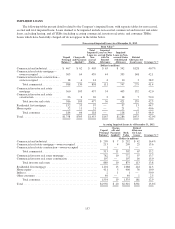

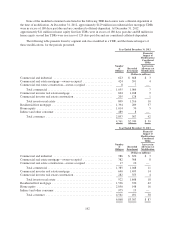

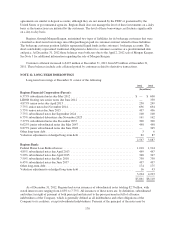

Data and assumptions used in the fair value calculation, as well as the valuation’s sensitivity to rate

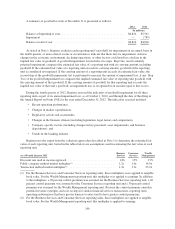

fluctuations, related to mortgage servicing rights (excluding related derivative instruments) as of December 31

are as follows:

2012 2011

(Dollars in millions)

Unpaid principal balance .................................................... $25,796 $26,218

Weighted-average prepayment speed (CPR; percentage) ........................... 17.6 % 27.8 %

Estimated impact on fair value of a 10% increase ............................ $ (13) $ (16)

Estimated impact on fair value of a 20% increase ............................ $ (23) $ (30)

Option-adjusted spread (basis points) .......................................... 754 235

Estimated impact on fair value of a 10% increase ............................ $ (4) $ (1)

Estimated impact on fair value of a 20% increase ............................ $ (9) $ (3)

Weighted-average coupon interest rate ......................................... 4.9% 5.2%

Weighted-average remaining maturity (months) ................................. 276 281

Weighted-average servicing fee (basis points) ................................... 28.3 28.7

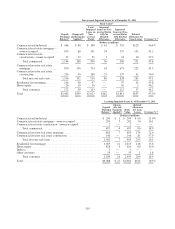

The sensitivity calculations above are hypothetical and should not be considered to be predictive of future

performance. Changes in fair value based on adverse changes in assumptions generally cannot be extrapolated

because the relationship of the change in assumption to the change in fair value may not be linear. Also, the

effect of an adverse variation in a particular assumption on the fair value of the mortgage servicing rights is

calculated without changing any other assumption, while in reality changes in one factor may result in changes in

another, which may either magnify or counteract the effect of the change. The derivative instruments utilized by

Regions would serve to reduce the estimated impacts to fair value included in the table above.

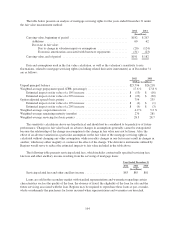

The following table presents servicing related fees, which includes contractually specified servicing fees,

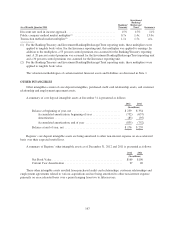

late fees and other ancillary income resulting from the servicing of mortgage loans:

Year Ended December 31

2012 2011 2010

(In millions)

Servicing related fees and other ancillary income ....................... $83 $85 $81

Loans are sold in the secondary market with standard representations and warranties regarding certain

characteristics such as the quality of the loan, the absence of fraud, the eligibility of the loan for sale and the

future servicing associated with the loan. Regions may be required to repurchase these loans at par, or make-

whole or indemnify the purchasers for losses incurred when representations and warranties are breached.

164