Regions Bank 2012 Annual Report Download - page 7

Download and view the complete annual report

Please find page 7 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

REGIONS 2012 ANNUAL REPORT

5

to specialized lending where our local bankers work

with experienced lenders to meet customer needs.

Total new production for this portfolio was a solid $15

billion, up 3% from 2011. We finished the year with

new business pipelines slightly above the same level

at the end of 2011, and loan commitments increased

12% from the prior year.

Funding Costs –

A Competitive Opportunity

Another key to our performance in 2012 was our

ability to improve our funding costs. Thanks to our

success at attracting low-cost deposits through our

more than 1,700 branches, we continued to enjoy a

favorable improvement in funding costs. Our funding

mix has continued to improve as low-cost deposits

grew 8% to $82 billion during 2012 and higher cost

time deposits declined 31% to $13 billion – falling

from 20% of total deposits at the end of 2011 to 14%

at the end of 2012. As a result, we entered 2013 with

a better funding mix and total funding costs of 0.58%,

which is 19 basis points lower than in the prior year.

The opportunity remains for us to improve our funding

costs even further, given that another $8.3 billion in

higher-cost CDs and other time deposits will mature

during 2013. This gives us an opportunity that should

enable us to generate better margins when interest

rates rise again. Also, we will continue to prudently

evaluate liability management opportunities as we look

to further reduce our total funding costs, including

long-term debt.

Expense Control –

A Culture, Not a Campaign

Even as we were making some structural changes

to the bank, we maintained a strong discipline on

expenses. Non-interest expenses from continuing

operations totaled $3.5 billion, or 9% below our

2011 expenses. At the end of 2012, our efficiency

ratio – defined as non-interest expenses as a share

of revenues – stood at 62.7%, which was in line with

our peer group. Among the banks in our peer group,

we have the second lowest expense-to-assets ratio

at 2.79%.

We have an extensive and competitive branch

network – one of the largest among our peers.

However, we continuously analyze our locations to

ensure that we have the correct number of branches

in our markets. In fact, as a cost-efficiency strategy,

we have reduced our number of branches by 13%

since 2007. We continue to believe that physical

branches are a key component of our distribution

strategy and provide a competitive advantage over

many of our competitors. We are investing aggressively

in our contact center technology, mobile banking and

web-based services. We are committed to providing

a comprehensive set of distribution capabilities to

serve our customers with efficiency and convenience.

We have been able to shift, where appropriate, more

customer activity to the Internet from the branches

and contact center. In fact, more than 40% of our

consumer checking customers now use Regions

online banking services. The launch of our mobile

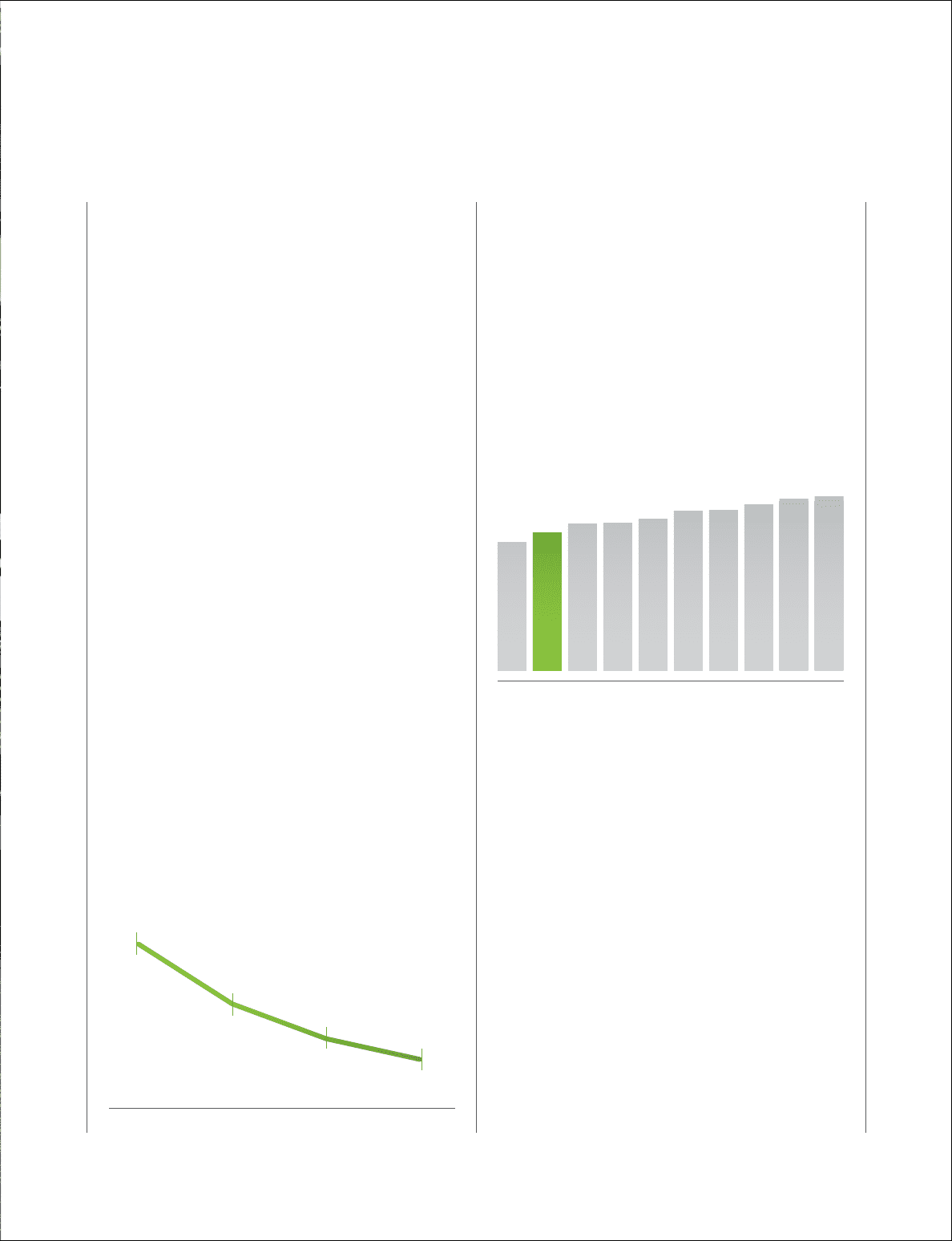

2009 2010 2011 2012

1.09%

1.64%

0.77%

0.58%

EXPENSE-TO-ASSETS RATIO VS. PEERS

REGIONS

BANK #1

BANK #3

BANK #5

BANK #4

BANK #6

BANK #7

BANK #8

BANK #9

BANK #10

2.79% 2.97%

2.60%

2.98% 3.06% 3.22% 3.25% 3.36% 3.47% 3.51%

FUNDING COSTS