Regions Bank 2012 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

assessment of the capital adequacy of a bank based on a variation of Tier 1 capital, known as Tier 1 common

equity. While not prescribed in amount by federal banking regulations, analysts and banking regulators have

assessed Regions’ capital adequacy using the tangible common stockholders’ equity and/or the Tier 1 common

equity measure. Because tangible common stockholders’ equity and Tier 1 common equity are not formally

defined by GAAP or prescribed in amount by federal banking regulations, these measures are considered to be

non-GAAP financial measures and other entities may calculate them differently than Regions’ disclosed

calculations. Since analysts and banking regulators may assess Regions’ capital adequacy using tangible common

stockholders’ equity and Tier 1 common equity, Regions believes that it is useful to provide investors the ability

to assess Regions’ capital adequacy on these same bases.

Tier 1 common equity is often expressed as a percentage of risk-weighted assets. Under the risk-based

capital framework, a bank’s balance sheet assets and credit equivalent amounts of off-balance sheet items are

assigned to one of four broad risk categories. The aggregated dollar amount in each category is then multiplied

by the risk weighting assigned to that category. The resulting weighted values from each of the four categories

are added together and this sum is the risk-weighted assets total that, as adjusted, comprises the denominator of

certain risk-based capital ratios. Tier 1 capital is then divided by this denominator (risk-weighted assets) to

determine the Tier 1 capital ratio. Adjustments are made to Tier 1 capital to arrive at Tier 1 common equity (non-

GAAP). Tier 1 common equity is also divided by the risk-weighted assets to determine the Tier 1 common equity

ratio. The amounts disclosed as risk-weighted assets are calculated consistent with banking regulatory

requirements.

Regions currently calculates its risk-based capital ratios under guidelines adopted by the Federal Reserve

based on the 1988 Capital Accord (“Basel I”) of the Basel Committee on Banking Supervision (the “Basel

Committee”). In December 2010, the Basel Committee released its final framework for Basel III, which will

strengthen international capital and liquidity regulations. When implemented by U.S. bank regulatory agencies

and fully phased-in, Basel III will change capital requirements and place greater emphasis on common equity.

The Federal Reserve has announced a delay in the implementation date of the final rules. However, when

implemented there will be a phase in period of up to 6 years. The U.S. bank regulatory agencies have not yet

finalized regulations governing the implementation of Basel III. Accordingly, the calculations provided below

are estimates, based on Regions’ current understanding of the framework, including the Company’s reading of

the original requirements, as well as the U.S. Notices of Proposed Rulemaking (“NPR”) released in June 2012,

and informal feedback received through the regulatory process. Regions’ understanding of the framework is

evolving and will likely change as the regulations are finalized. The NPR comment period ended in October

2012; changes to the calculation resulting from the comment process could result in materially different capital

ratios from the amounts estimated. Because the Basel III implementation regulations are not formally defined by

GAAP and have not yet been finalized and codified, these measures are considered to be non-GAAP financial

measures, and other entities may calculate them differently from Regions’ disclosed calculations. Since analysts

and banking regulators may assess Regions’ capital adequacy using the Basel III framework, Regions believes

that it is useful to provide investors information enabling them to assess Regions’ capital adequacy on the same

basis.

Non-GAAP financial measures have inherent limitations, are not required to be uniformly applied and are

not audited. Although these non-GAAP financial measures are frequently used by stakeholders in the evaluation

of a company, they have limitations as analytical tools, and should not be considered in isolation, or as a

substitute for analyses of results as reported under GAAP. In particular, a measure of earnings that excludes

selected items does not represent the amount that effectively accrues directly to stockholders (i.e., REIT

investment early termination costs, merger-related charges, goodwill impairment and regulatory charge and

related tax benefit are a reduction to earnings and stockholders’ equity).

The following tables provide: 1) a reconciliation of net income (loss) (GAAP) to income (loss) available to

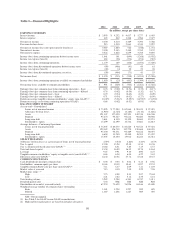

common shareholders (GAAP), 2) a reconciliation of net income (loss) available to common shareholders

(GAAP) to income (loss) from continuing operations available to common shareholders (GAAP), 3) a

53