Regions Bank 2012 Annual Report Download - page 130

Download and view the complete annual report

Please find page 130 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

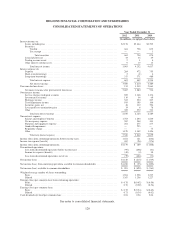

Non-interest expense from continuing operations was $3.9 billion in both 2011 and 2010 and included a

$253 million goodwill impairment charge in 2011 and a $75 million regulatory charge in 2010. See Table 6

“Non-Interest Expense from Continuing Operations” and the text preceding Table 2 “GAAP to Non-GAAP

Reconciliation”. Salaries and employee benefits remained relatively stable at $1.6 billion in 2011. At

December 31, 2011, Regions had 23,707 employees compared to 24,656 at December 31, 2010.

Net occupancy expense decreased 6 percent to $388 million in 2011. Furniture and equipment expense

decreased modestly by $2 million to $275 million in 2011. Both of these decreases were primarily driven by

branch consolidations.

Professional and legal fees are comprised of amounts related to legal, consulting and other professional fees.

These fees increased $5 million to $175 million in 2011, reflecting an increase in the level of legal expenses

including credit-related legal costs in 2011.

OREO expense decreased $47 million to $162 million in 2011 compared to $209 million in 2010, primarily driven

by the reduction in OREO balances along with lower valuation charges. Through Regions’ efforts to sell foreclosed

properties, OREO balances decreased $158 million to $296 million in 2011 compared to $454 million in 2010.

Net losses on loans held for sale decreased $31 million to $1 million in 2011 compared to $32 million in

2010, primarily due to firming prices.

Deposit administrative fees decreased $3 million to $217 million in 2011. Deposit administrative fees were

impacted by a new assessment rule in 2011, which revised the deposit insurance assessment system for large

institutions. The new rule changed the assessment base from deposits as the basis and utilizes a risk-based

approach which calculates the assessment using average consolidated assets minus average tangible equity.

Implementation of the new rule was effective beginning in the second quarter of 2011. The bank regulatory

agencies’ ratings, comprised of Regions Bank’s capital, asset quality, management, earnings, liquidity and

sensitivity to risk, along with certain financial ratios are used in determining deposit administrative fees.

During 2010, Regions prepaid approximately $2.0 billion of FHLB advances, realizing a $108 million pre-tax

loss on early extinguishment. These extinguishments were part of the Company’s asset/liability management process.

Other miscellaneous expenses include communications, postage, supplies, credit-related costs and business

development services. Other miscellaneous expenses decreased $18 million to $436 million in 2011, reflecting

the Company controlling discretionary costs.

The Company’s income tax benefit for 2011 was $28 million compared to a tax benefit of $376 million in

2010, resulting in an effective tax rate of (17.4) percent and 44.5 percent, respectively. The decrease in income

tax benefit was primarily a result of positive consolidated pre-tax earnings and the goodwill impairment.

At December 31, 2011, the allowance for loan losses totaled $2.7 billion or 3.54 percent of total loans, net

of unearned income compared to $3.2 billion or 3.84 percent at year-end 2010. Net charge-offs totaled $2.0

billion, or 2.44 percent of average loans in 2011 compared to $2.8 billion, or 3.22 percent of average loans in

2010. Net charge-offs were lower across most major categories when comparing 2011 to the prior year. The

provision for loan losses is used to maintain the allowance for loan losses at a level that in management’s

judgment is appropriate to cover losses inherent in the portfolio at the balance sheet date. During 2011 the

provision for loan losses was $1.5 billion. This compares to a provision for loan losses of $2.9 billion in 2010.

Net charge-offs exceeded the provision for loan losses during 2011 primarily due to the allowance associated

with the loans transferred to held for sale, as well as improving consumer credit metrics. Non-performing assets

decreased from $3.9 billion at December 31, 2010, to $3.0 billion at December 31, 2011, reflecting

management’s efforts to work through problem assets and reduce the riskiest exposures.

114