Regions Bank 2012 Annual Report Download - page 177

Download and view the complete annual report

Please find page 177 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

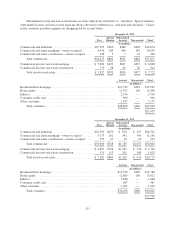

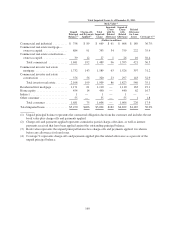

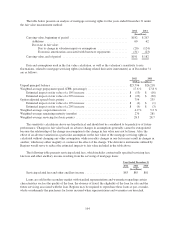

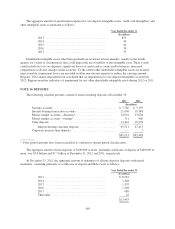

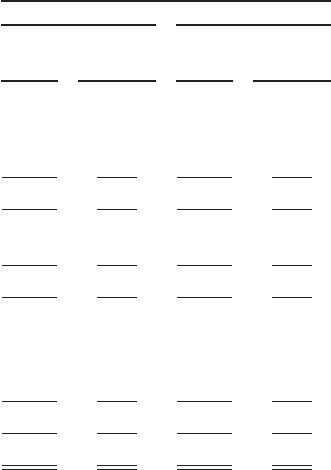

The following table presents the average balances of total impaired loans and interest income for the years

ended December 31, 2012 and 2011. Interest income recognized represents interest recognized on loans modified

in a TDR, and are therefore considered impaired, which are on accruing status.

Year Ended December 31

2012 2011

Average

Balance

Interest

Income

Recognized

Average

Balance

Interest

Income

Recognized

(In millions)

Commercial and industrial .................................. $ 707 $ 16 $ 563 $ 7

Commercial real estate mortgage—owner-occupied .............. 737 11 761 5

Commercial real estate construction—owner-occupied ............ 23 — 30 —

Total commercial ..................................... 1,467 27 1,354 12

Commercial investor real estate mortgage ...................... 1,510 40 1,457 22

Commercial investor real estate construction .................... 210 7 449 4

Total investor real estate ................................ 1,720 47 1,906 26

Residential first mortgage ................................... 1,157 39 1,086 41

Home equity ............................................. 439 22 410 21

Indirect ................................................. 2 — 2 —

Other consumer ........................................... 47 3 61 4

Total consumer ....................................... 1,645 64 1,559 66

Total impaired loans ....................................... $4,832 $138 $4,819 $104

No material amount of interest income was recognized on impaired loans for the year ended December 31,

2010.

In addition to the impaired loans detailed in the tables above, there were approximately $89 million in non-

performing loans classified as held for sale at December 31, 2012, compared to $328 million at December 31,

2011. These loans are larger balance credits, primarily investor real estate, where management does not have the

intent to hold the loans for the foreseeable future. The loans are carried at an amount approximating a price

which will be recoverable through the loan sale market. During the year ended December 31, 2012,

approximately $302 million in non-performing loans were transferred to held for sale; this amount is net of

charge-offs of $163 million recorded upon transfer.

At December 31, 2012 and 2011, non-accrual loans including loans held for sale totaled $1.8 billion and

$2.7 billion, respectively. The amount of interest income recognized in 2012, 2011 and 2010 on loans prior to

migrating to non-accrual status was approximately $18 million, $23 million and $47 million, respectively. If

these loans had been current in accordance with their original terms, approximately $76 million, $122 million

and $165 million of interest income, respectively, would have been recognized on these loans in 2012, 2011 and

2010.

TROUBLED DEBT RESTRUCTURINGS (TDRs)

The majority of Regions’ 2012 commercial and investor real estate TDRs are the result of renewals where

the only concession is that the interest rate at renewal is not considered to be a market rate. Consumer TDRs

generally involve an interest rate concession. Accordingly, the financial impact of the modifications is best

illustrated by the impact to the allowance calculation at the loan or pool level as a result of the loans being

considered impaired due to their status as a TDR.

161