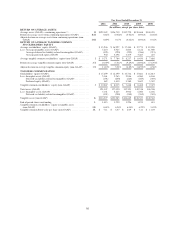

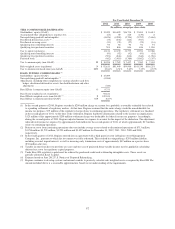

Regions Bank 2012 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

In preparing financial information, management is required to make significant estimates and assumptions

that affect the reported amounts of assets, liabilities, income and expenses for the periods shown. The accounting

principles followed by Regions and the methods of applying these principles conform with accounting principles

generally accepted in the U.S. and general banking practices. Estimates and assumptions most significant to

Regions are related primarily to the allowance for credit losses, fair value measurements, intangible assets

(goodwill and other identifiable intangible assets), mortgage servicing rights and income taxes, and are

summarized in the following discussion and in the notes to the consolidated financial statements.

Allowance for Credit Losses

The allowance for credit losses (“allowance”) consists of the allowance for loan losses and the reserve for

unfunded credit commitments. These two components reflect management’s judgment of probable credit losses

inherent in the portfolio and unfunded credit commitments at the balance sheet date. A full discussion of these

estimates and other factors is included in the “Allowance for Credit Losses” section within the discussion of

“Credit Risk”, found in a later section of this report, Note 1 “Summary of Significant Accounting Policies”, and

Note 6 “Allowance for Credit Losses” to the consolidated financial statements.

The allowance is sensitive to a variety of internal factors, such as portfolio performance and assigned risk

ratings, as well as external factors, such as interest rates and the general health of the economy. Management

reviews different assumptions for variables that could result in increases or decreases in probable inherent credit

losses, which may materially impact Regions’ estimate of the allowance and results of operations.

Management’s estimate of the allowance for the commercial and investor real estate portfolio segments

could be affected by estimates of losses inherent in various product types as a result of fluctuations in the general

economy, developments within a particular industry, or changes in an individual’s credit due to factors particular

to that credit, such as competition, management or business performance. For non-accrual commercial and

investor real estate loans equal to or greater than $2.5 million, the allowance for loan losses is based on specific

evaluation considering the facts and circumstances specific to each borrower. For all other commercial and

investor real estate loans, the allowance for loan losses is based on statistical models using a probability of

default (“PD”) and a loss given default (“LGD”). Historical default information for similar loans is used as an

input for the statistical model. A 5 percent increase in the PD for non-defaulted accounts and a 5 percent increase

in the LGD for all accounts would result in an increase to estimated losses of approximately $85 million.

For residential real estate mortgages, home equity lending and other consumer-related loans, individual

products are reviewed on a group basis or in loan pools (e.g., residential real estate mortgage pools). Losses can

be affected by such factors as collateral value, loss severity, the economy and other uncontrollable factors. A 5

percent increase or decrease in the estimated loss rates on these loans would change estimated inherent losses by

approximately $28 million.

Additionally, the estimate of the allowance for the entire portfolio may change due to modifications in the

mix and level of loan balances outstanding and general economic conditions, as evidenced by changes in real

estate demand and values, interest rates, unemployment rates, bankruptcy filings, fluctuations in the gross

domestic product, and the effects of weather and natural disasters such as droughts and hurricanes. Each has the

ability to result in actual loan losses that could differ from originally estimated amounts.

The pro forma inherent loss analysis presented above demonstrates the sensitivity of the allowance to key

assumptions. This sensitivity analysis does not reflect an expected outcome. For additional information regarding

the allowance for credit losses calculation, see Note 1 “Summary of Significant Accounting Policies” and Note 6

“Allowance For Credit Losses” to the consolidated financial statements.

58