Regions Bank 2012 Annual Report Download - page 219

Download and view the complete annual report

Please find page 219 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

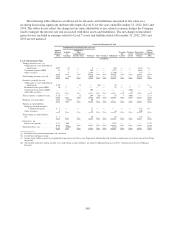

FAIR VALUE OPTION

Regions elected the fair value option for FNMA and FHLMC eligible thirty-year residential mortgage loans

held for sale originated on or after January 1, 2008. Additionally, Regions elected the fair value option for

FNMA and FHLMC eligible fifteen-year residential mortgage loans held for sale originated on or after

November 22, 2010. These elections allow for a more effective offset of the changes in fair values of the loans

and the derivative instruments used to economically hedge them without the burden of complying with the

requirements for hedge accounting. Regions has not elected the fair value option for other loans held for sale

primarily because they are not economically hedged using derivative instruments. Fair values of mortgage loans

held for sale are based on traded market prices of similar assets where available and/or discounted cash flows at

market interest rates, adjusted for securitization activities that include servicing values and market conditions,

and were recorded in loans held for sale in the consolidated balance sheets.

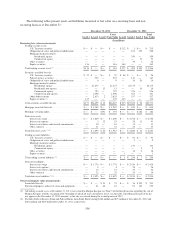

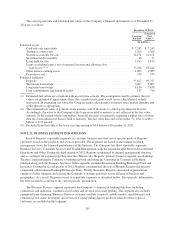

The following table summarizes the difference between the aggregate fair value and the aggregate unpaid

principal balance for mortgage loans held for sale measured at fair value:

December 31, 2012 December 31, 2011

Aggregate

Fair Value

Aggregate

Unpaid

Principal

Aggregate Fair

Value Less

Aggregate

Unpaid

Principal

Aggregate

Fair Value

Aggregate

Unpaid

Principal

Aggregate Fair

Value Less

Aggregate

Unpaid

Principal

(In millions)

Mortgage loans held for sale, at fair

value ....................... $1,282 $1,235 $47 $844 $815 $29

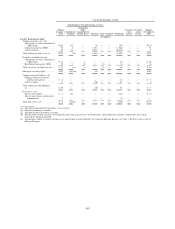

Interest income on mortgage loans held for sale is recognized based on contractual rates and is reflected in

interest income on loans held for sale in the consolidated statements of operations. The following table details net

gains (losses) resulting from changes in fair value of these loans which were recorded in mortgage income in the

consolidated statements of operations. These changes in fair value are mostly offset by economic hedging

activities. An immaterial portion of these amounts was attributable to changes in instrument-specific credit risk.

Mortgage loans held for sale, at fair value

Year Ended December 31

2012 2011

(In millions)

Net gains resulting from changes in fair

value ............................. $18 $36

203