Regions Bank 2012 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

Refer to the discussion of intangible assets in Note 1 “Summary of Significant Accounting Policies” to the

consolidated financial statements for a discussion of these approaches and Note 9 “Intangible Assets” for a

discussion of the assumptions. The fair values of assets and liabilities are determined using an exit price concept.

Refer to Note 1 “Summary of Significant Accounting Policies” to the consolidated financial statements for

discussions of the exit price concept and the determination of fair values of financial assets and liabilities.

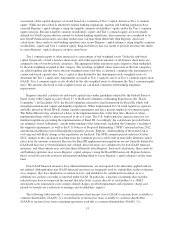

Throughout 2009 and 2010 in the former Banking/Treasury reporting unit, the credit quality of Regions’

loan portfolio declined, which contributed to increased losses as well as elevated non-performing loan levels.

Accordingly, Regions performed tests of goodwill for impairment during each quarter of 2010 and during the

second, third and fourth quarters of 2009 in a manner consistent with the test conducted in the fourth quarter of

2008. While credit quality has improved, Regions continued to perform its goodwill impairment tests during the

four quarters of 2011 and the first two quarters of 2012, in a manner consistent with the tests conducted in prior

periods, primarily due to the Company’s market capitalization remaining below book value. As a result of the

management reporting changes described above, Regions revised its reportable segments and, consequently, its

reporting units from the three segments previously reported and reallocated goodwill to the new reporting units

based on the relative fair values of the revised reporting units. The long-term fair value of equity was determined

using both income and market approaches (referenced above and discussed in Note 9 “Intangible Assets”). The

results of these calculations indicated that the estimated fair value of the Wealth Management reporting unit was

greater than its carrying amount and the estimated fair values of the Business Services and Consumer Services

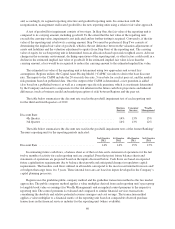

reporting units were less than their respective carrying amounts. At October 1, 2012, the carrying amount and

estimated fair value of the Business Services reporting unit were $8.7 billion and $7.1 billion, respectively, while

the carrying amount of goodwill for the reporting unit was $2.6 billion. At October 1, 2012, the carrying amount

and estimated fair value of the Consumer Services reporting unit were $5.2 billion and $5.2 billion respectively,

while the carrying amount of goodwill for the reporting unit was $1.8 billion. Therefore, Step Two of the

goodwill impairment test was performed for both the Business Services and Consumer Services reporting units.

In Step Two, the fair values of each reporting unit’s assets, both tangible and intangible, and liabilities were

determined using estimates of the amounts at which the assets (or liabilities) could be bought (or incurred) or

sold (settled) in a taxable transaction between willing participants. For the Business Services and Consumer

Services reporting units, the effects of the Step Two adjustments, which were primarily write-downs of assets to

fair value, exceeded any reductions in the value of common equity determined in Step One; accordingly the

calculation of implied goodwill exceeded its carrying amount. Therefore, the results were no impairment for the

Business Services and Consumer Services reporting units, whose implied fair value of goodwill exceeded their

carrying amounts by approximately 74 percent and 202 percent, respectively, as of October 1, 2012.

Specific factors as of the date of filing the financial statements that could negatively impact the assumptions

used in assessing goodwill for impairment include: a protracted decline in the Company’s market capitalization,

disparities in the level of fair value changes in net assets (especially loans) compared to equity, increases in book

values of equity of a reporting unit in excess of the increase in fair value of equity, adverse business trends

resulting from litigation and/or regulatory actions, higher loan losses, lengthened forecasts of higher

unemployment relative to pre-crisis levels beyond 2013, future increased minimum regulatory capital

requirements above current thresholds (refer to Note 13 “Regulatory Capital Requirements and Restrictions” for

a discussion of current minimum regulatory requirements), future federal rules and regulations resulting from the

Dodd-Frank Act, and/or a protraction in the current low level of interest rates significantly beyond 2014.

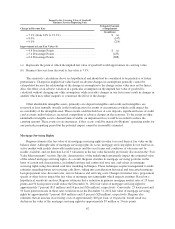

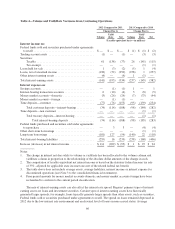

The following tables present an analysis of independent changes in market factors and significant

assumptions that could adversely impact the carrying balance of goodwill in the Business Services reporting unit.

Due to the magnitude of the excess of the Consumer Services reporting unit’s implied fair value of goodwill over

its carrying amount, no such table has been included for this reporting unit.

61