Regions Bank 2012 Annual Report Download - page 167

Download and view the complete annual report

Please find page 167 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

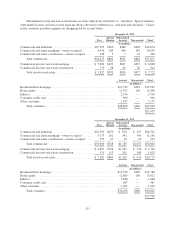

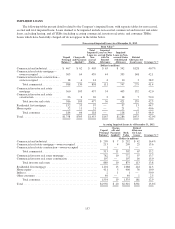

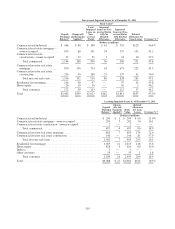

NOTE 6. ALLOWANCE FOR CREDIT LOSSES

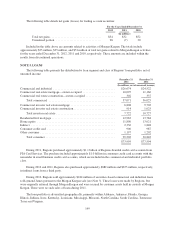

The allowance for credit losses represents management’s estimate of credit losses inherent in the loan and

credit commitment portfolios as of year-end. The allowance for credit losses consists of two components: the

allowance for loan and lease losses and the reserve for unfunded credit commitments. Management’s assessment

of the appropriateness of the allowance for credit losses is based on a combination of both of these components.

Regions determines its allowance for credit losses in accordance with applicable accounting literature as well as

regulatory guidance related to receivables and contingencies. Binding unfunded credit commitments include

items such as letters of credit, financial guarantees and binding unfunded loan commitments.

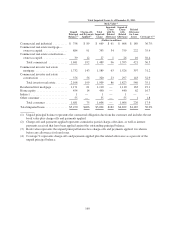

CALCULATION OF ALLOWANCE FOR CREDIT LOSSES

As part of the Company’s ongoing efforts to enhance the allowance calculation, and in response to

regulatory guidance, the home equity portfolio was segmented at a more granular level during the first quarter of

2012. Loss rates for home equity products are now developed based on lien position, status as a troubled debt

restructuring (“TDR”), geography, past due status, and refreshed FICO scores for non-past due loans. The

enhancement had the impact of reducing the component of the allowance for loan losses related to home equity

loans by an estimate of approximately $30 million.

In addition to the home equity enhancement, in the second quarter of 2012, the Company refined the

methodology for estimation of the reserve for unfunded credit commitments. Before the change, the Company

based the reserve for unfunded credit commitments on an analysis of the overall probability of funding and

historical losses. Beginning with the second quarter of 2012, the reserve is based on an exposure at default

(“EAD”) multiplied by a probability of default (“PD”) multiplied by a loss-given default (“LGD”). The EAD is

estimated based on an analysis of historical funding patterns for defaulted loans in various categories. The PD

and LGD align with the statistically-calculated parameters used to calculate the allowance for loan losses for

various pools, which are based on credit quality indicators and product type. The methodology applies to

commercial and investor real estate credit commitments and standby letters of credit. The Company made this

change to enhance portfolio segmentation within the calculation of the reserve for unfunded credit commitments

and to improve overall consistency within the calculation of the allowance for credit losses. The change did not

have a material impact on the allowance for credit losses or the reserve for unfunded credit commitments.

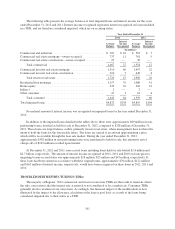

Except for the enhancements to home equity segmentation and to the reserve for unfunded credit

commitments described above, there were no changes during 2012 in methodology for the calculation of the

allowance for credit losses or policies for identification of non-accrual loans or for charge-offs. See Note 1 for a

detailed description of the Company’s methodology.

151