Regions Bank 2012 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

Valuation adjustments are primarily recorded in other non-interest expense; adjustments are also recorded as

a charge to the allowance for loan losses if incurred within 60 days after the date of transfer from loans.

Valuation adjustments are primarily post-foreclosure write-downs that are a result of continued declining

property values based on updated appraisals or other indications of value, such as offers to purchase. Foreclosed

property sold represents the net book value of the properties sold.

Other Assets

Other assets decreased $2.6 billion to $6.2 billion as of December 31, 2012. Securities sold but not yet

settled balances at the end of 2011, which did not repeat in 2012, and lower derivative assets primarily drove the

decrease. Reduced foreclosed properties, deferred income taxes and prepaid expense balances also contributed to

the year-over-year decrease.

Deposits

Regions competes with other banking and financial services companies for a share of the deposit market.

Regions’ ability to compete in the deposit market depends heavily on the pricing of its deposits and how

effectively the Company meets customers’ needs. Regions employs various means to meet those needs and

enhance competitiveness, such as providing a high level of customer service, competitive pricing and providing

convenient branch locations for its customers. Regions also serves customers through providing centralized,

high-quality banking services and alternative product delivery channels such as internet banking.

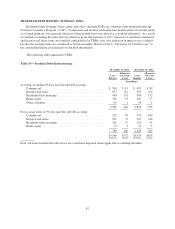

Deposits are Regions’ primary source of funds, providing funding for 88 percent of average interest-earning

assets from continuing operations in 2012 and 85 percent of average interest-earning assets from continuing

operations in 2011. Table 24 “Deposits” details year-over-year deposits on a period-ending basis. Total deposits

at December 31, 2012, decreased approximately $153 million compared to year-end 2011 levels. The overall

decrease was driven by a significant decrease in time deposits. This decrease was largely offset by increases in

almost all categories of low-cost deposits. Regions continued to focus on shifting the overall deposit mix toward

low-cost deposits, with an emphasis on non-interest-bearing demand and interest-bearing transaction accounts, in

an effort to reduce funding costs.

Customer deposits, which exclude deposits used for wholesale funding purposes, decreased by 0.2 percent

to $95.5 billion on an ending basis during 2012. Due to liquidity in the market, Regions has been able to steadily

grow its low-cost customer deposits and reduce its total deposit costs from 0.78 percent in 2010 to 0.49 percent

in 2011 and to 0.30 percent in 2012.

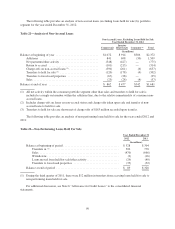

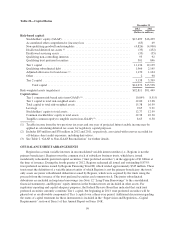

Table 24—Deposits

2012 2011 2010

(In millions)

Non-interest-bearing demand* .................................................. $29,963 $28,209 $25,683

Savings accounts ............................................................. 5,760 5,159 4,668

Interest-bearing transaction accounts ............................................. 21,096 19,388 13,423

Money market accounts—domestic* ............................................. 24,901 23,028 27,396

Money market accounts—foreign* ............................................... 311 460 643

Low-cost deposits ........................................................ 82,031 76,244 71,813

Time deposits ............................................................... 13,443 19,378 22,784

Customer deposits ........................................................ 95,474 95,622 94,597

Corporate treasury time deposits ................................................. — 5 17

$95,474 $95,627 $94,614

* Prior period amounts have been reclassified to conform to current period classification

92