Regions Bank 2012 Annual Report Download - page 157

Download and view the complete annual report

Please find page 157 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

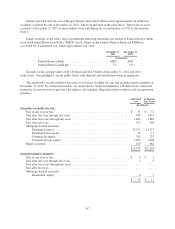

made, must be based on sufficient information available to support an alternate opinion of market value. An

estimated standard discount factor, which is updated at least annually, is applied to the appraisal amount for

certain commercial and investor real estate properties when the recorded investment in the loan is transferred into

foreclosed property. Internally adjusted valuations are considered Level 3 measurements as management uses

assumptions that may not be observable in the market.

Loans held for sale for which the fair value option has not been elected are recorded at the lower of cost or

fair value and therefore are reported at fair value on a non-recurring basis. The fair values for loans held for sale

that are based on formally committed loan sale prices or valuations performed using observable inputs are

classified as a Level 2 measurement. If no formally committed sales price is available, a professional valuation is

obtained, consistent with the process described above for foreclosed property and other real estate.

FAIR VALUE OF FINANCIAL INSTRUMENTS

The following methods and assumptions were used by the Company in estimating fair values of financial

instruments that are not disclosed above:

Cash and cash equivalents: The carrying amounts reported in the consolidated balance sheets and cash

flows approximate the estimated fair values. Because these amounts generally relate to either currency or highly

liquid assets, these are considered Level 1 valuations.

Securities held to maturity: The fair values of securities held to maturity are estimated in the same manner

as the corresponding securities available for sale, which are measured at fair value on a recurring basis.

Loans, (excluding leases), net of unearned income and allowance for loan losses: A discounted cash

flow method under the income approach is utilized to estimate the fair value of the loan portfolio. The discounted

cash flow method relies upon assumptions about the amount and timing of principal and interest payments,

principal prepayments, and estimates of principal defaults, loss given default, and current market rates (excluding

credit). The loan portfolio is aggregated into categories based on loan type and credit quality. For each loan

category, weighted average statistics, such as coupon rate, age, and remaining term are calculated. These are

Level 3 valuations.

Other interest-earning assets: The carrying amounts reported in the consolidated balance sheets

approximate the estimated fair values. While these instruments are not actively traded in the market, the majority

of the inputs required to value them are actively quoted and can be validated through external sources.

Accordingly, these are Level 2 valuations.

Deposits: The fair value of non-interest-bearing demand accounts, interest-bearing transaction accounts,

savings accounts, money market accounts and certain other time deposit accounts is the amount payable on

demand at the reporting date (i.e., the carrying amount). Fair values for certificates of deposit are estimated by

using discounted cash flow analyses, based on market spreads to benchmark rates. These are Level 2 valuations.

Short-term and long-term borrowings: The carrying amounts of short-term borrowings reported in the

consolidated balance sheets approximate the estimated fair values, and are considered Level 2 measurements as

similar instruments are traded in active markets. The fair values of certain long-term borrowings are estimated

using quoted market prices of identical instruments and are considered Level 1 measurements. If identical

instruments are not available, fair values are estimated using quoted market prices for similar instruments and are

considered Level 2 valuations. Otherwise, valuations are based on a combination of non-binding broker quotes

and quoted prices for identical instruments in non-active markets and are considered Level 3 valuations.

Loan commitments and letters of credit: The estimated fair values for these off-balance sheet instruments

are based on probabilities of funding to project future loan fundings, which are discounted using the loan

methodology described above. The premiums/discounts are adjusted for the time value of money over the

141