Regions Bank 2012 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

Repurchase agreements are also offered as commercial banking products as short-term investment

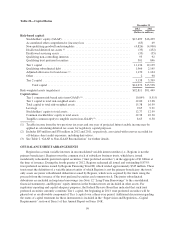

opportunities for customers. At the end of each business day, customer balances are swept into the agreement

account. In exchange for cash, Regions sells the customer securities with a commitment to repurchase them on

the following business day. The repurchase agreements are collateralized to allow for market fluctuations.

Securities from Regions Bank’s investment portfolio are used as collateral. From the customer’s perspective, the

investment earns more than a traditional money market instrument. From Regions’ standpoint, the repurchase

agreements are similar to deposit accounts, although they are not insured by the FDIC or guaranteed by the

United States or governmental agencies. Regions Bank does not manage the level of these investments on a daily

basis as the transactions are initiated by the customers. The level of these borrowings can fluctuate significantly

on a day-to-day basis.

Long-Term Borrowings

Regions’ long-term borrowings consist primarily of FHLB borrowings, senior notes, subordinated notes and

other long-term notes payable. Total long-term borrowings decreased $2.2 billion to $5.9 billion at December 31,

2012. At the parent company, the decrease resulted from the maturity of approximately $950 million of

subordinated and senior notes. Additionally at the parent company, $345 million of 8.875% Junior Subordinated

Notes were redeemed during 2012 resulting in an $11 million loss on early extinguishment of debt. At the bank

level, approximately $902 million of FHLB advances were prepaid during 2012, realizing an immaterial pre-tax

loss on early extinguishment. The weighted-average interest rate on total long-term debt, including the effect of

derivative instruments, was 4.7%, 3.3% and 3.2% for the years ended December 31, 2012, 2011 and 2010,

respectively. See Note 12 “Long-Term Borrowings” to the consolidated financial statements for further

discussion and detailed listing of outstandings and rates.

Other Liabilities

Other liabilities decreased $808 million to $2.9 billion as of December 31, 2012. The decrease was primarily

driven by lower derivative liabilities and accrued employee benefit costs, as well as the reduction of a liability

related to a third-party investment in a REIT as a result of an early termination of the investment. These

decreases were partially offset by the establishment of the indemnification obligation related to the sale of

Morgan Keegan to Raymond James. See Note 3 “Discontinued Operations” and Note 23 “Commitments,

Contingencies and Guarantees” for additional information.

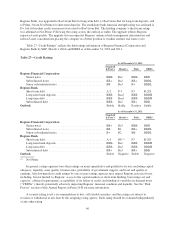

Ratings

In March of 2012, Standard & Poor’s (“S&P”) upgraded the credit ratings for each of the obligations of both

Regions Financial Corporation and Regions Bank. The upgrades were attributable to the March 2012 common

stock offering of approximately $875 million, net of issuance costs, as well as the redemption of 3.5 million

shares of Series A preferred stock. In February of 2012, Moody’s revised its outlook for Regions Financial

Corporation from negative to stable.

On March 8, 2012, Fitch Ratings (“Fitch”) downgraded the junior subordinated notes of Regions Financial

Corporation. This ratings action was part of a global review of securities impacted in part by capital requirements

set forth in Basel III as well as Fitch’s view regarding the likelihood of sovereign support.

On June 13, 2012, Dominion Bond Rating Service (“DBRS”) revised its outlook for Regions Financial

Corporation from negative to stable.

On October 30, 2012, Fitch revised its outlook for Regions Financial Corporation from stable to positive.

On December 17, 2012, Moody’s upgraded the long-term ratings of Regions Financial Corporation and its

subsidiaries. Regions Financial Corporation was upgraded to Ba1 from Ba3 for senior debt. Its lead bank,

95