Regions Bank 2012 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

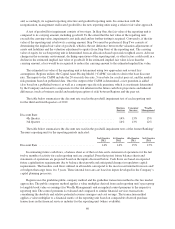

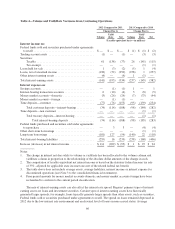

Impact to the Carrying Value of Goodwill

Business Services Reporting Unit

Change in Discount Rate

Estimated Amount

of Impairment

(In millions)

+ 7.1% (from 14% to 21.1%) ...................... $ (a)

+ 8.0% ........................................ (147)

+ 9.0% ........................................ (219)

Improvement in Loan Fair Values (b)

+ 4.4 Percentage Points ........................... $ (a)

+ 5.4 Percentage Points ........................... (435)

+ 6.4 Percentage Points ........................... (868)

(a) Represents the point at which the implied fair value of goodwill would approximate its carrying value.

(b) Business Services loan discount to fair value is 7.9%.

The sensitivity calculations above are hypothetical and should not be considered to be predictive of future

performance. Changes in implied fair value based on adverse changes in assumptions generally cannot be

extrapolated because the relationship of the change in assumption to the change in fair value may not be linear.

Also, the effect of an adverse variation in a particular assumption on the implied fair value of goodwill is

calculated without changing any other assumption, while in reality changes in one factor may result in changes in

another which may either magnify or counteract the effect of the change.

Other identifiable intangible assets, primarily core deposit intangibles and credit card intangibles, are

reviewed at least annually (usually in the fourth quarter) for events or circumstances which could impact the

recoverability of the intangible asset. These events could include loss of core deposits, significant losses of credit

card accounts and/or balances, increased competition or adverse changes in the economy. To the extent an other

identifiable intangible asset is deemed unrecoverable, an impairment loss would be recorded to reduce the

carrying amount. These events or circumstances, if they occur, could be material to Regions’ operating results for

any particular reporting period but the potential impact cannot be reasonably estimated.

Mortgage Servicing Rights

Regions estimates the fair value of its mortgage servicing rights in order to record them at fair value on the

balance sheet. Although sales of mortgage servicing rights do occur, mortgage servicing rights do not trade in an

active market with readily observable market prices and the exact terms and conditions of sales may not be

readily available, and are therefore Level 3 valuations in the fair value hierarchy previously discussed in the “Fair

Value Measurements” section. Specific characteristics of the underlying loans greatly impact the estimated value

of the related mortgage servicing rights. As a result, Regions stratifies its mortgage servicing portfolio on the

basis of certain risk characteristics, including loan type and contractual note rate, and values its mortgage

servicing rights using discounted cash flow modeling techniques. These techniques require management to make

estimates regarding future net servicing cash flows, taking into consideration historical and forecasted mortgage

loan prepayment rates, discount rates, escrow balances and servicing costs. Changes in interest rates, prepayment

speeds or other factors impact the fair value of mortgage servicing rights which impacts earnings. Based on a

hypothetical sensitivity analysis, Regions estimates that a reduction in primary mortgage market rates of 25 basis

points and 50 basis points would reduce the December 31, 2012 fair value of mortgage servicing rights by

approximately 7 percent ($13 million) and 14 percent ($26 million), respectively. Conversely, 25 basis point and

50 basis point increases in these rates would increase the December 31, 2012 fair value of mortgage servicing

rights by approximately 7 percent ($14 million) and 15 percent ($28 million), respectively. Regions also

estimates that an increase in servicing costs of approximately $10 per loan, or 18 percent, would result in a

decline in the value of the mortgage servicing rights by approximately $7 million or 3 basis points.

62