Regions Bank 2012 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

REGIONS 2012 ANNUAL REPORT

2

We also strengthened our balance sheet with fewer

problem loans and stronger capital, which further

positions us well for future growth. The improvement

in our asset quality metrics was significant, with

non-performing assets, including assets held for sale,

decreasing 36% year-over-year. At the end of 2012,

non-performing assets stood at $1.9 billion, which

was the lowest level in four years. Our capital position

remains strong as our estimated Tier 1 Capital ratio at

December 31 stood at 12%, and our estimated Tier

1 Common ratio increased approximately 230 basis

points from the end of 2011 to 10.8%.

As positive as this performance was, it also reflected

the challenging economic environment in which we

still operate. We realize that Regions – like the rest

of the industry – must now demonstrate that we can

prudently generate organic growth. We understand

the challenge, and our management team is focused

on moving forward and addressing that challenge.

I am confident that the steps we have taken over the

past three years – and particularly in 2012 – have

positioned Regions to capture more than its share

of growth in 2013 and beyond. We have emerged

from the financial crisis stronger than before, with a

solid capital base and a strong presence in some of

the fastest growing markets in the country. We also

expect Regions and our customers to benefit from

our investments in a single operating platform, which

today gives our associates an integrated view of every

account each customer holds. We believe this is a

distinct competitive advantage. And, given that our

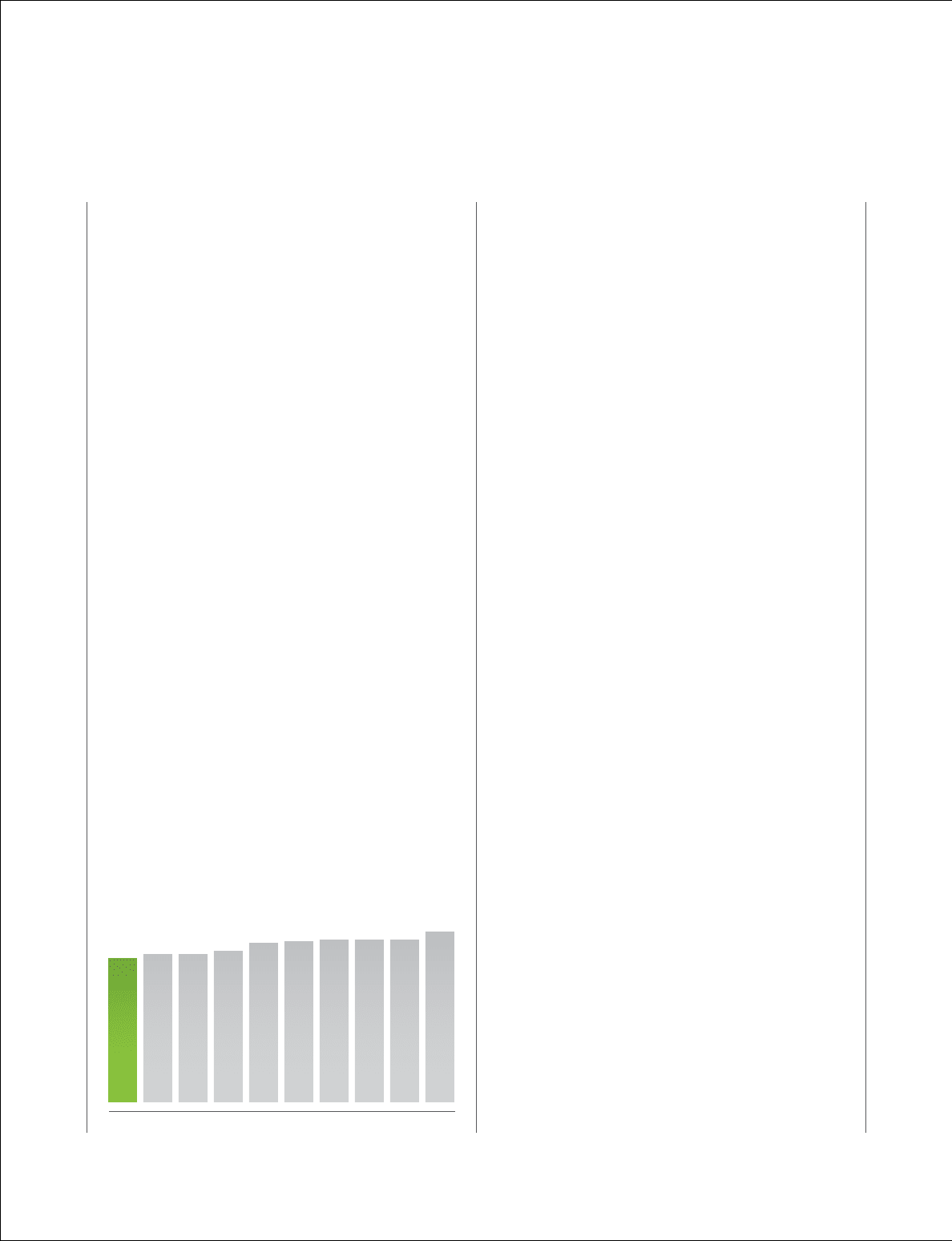

loan-to-deposit ratio remains relatively low at 78%,

we still have substantial lending capacity to tap as

the economy strengthens and as our customers’

borrowing needs increase.

We raised new equity capital. The Federal Reserve

conducted an industrywide stress test, and Regions

ranked fifth of the 19 banks in its Comprehensive

Capital Analysis and Review. With the markets

showing renewed confidence in banks, we raised

approximately $900 million in new common equity

last March to repay our TARP obligation. In October,

we raised $500 million in preferred stock that also

strengthened regulatory capital, and at the end of

2012, our Tier 1 Common ratio was 10.8%.

We divested Morgan Keegan. In April 2012, we

completed the sale of our brokerage and investment

banking company, Morgan Keegan, to Raymond

James Financial, Inc., for approximately $1.2 billion.

This move gave us the ability to better focus on the

fundamentals of our core business. Following the sale,

we also established the Regions Wealth Management

Group, which provides clients with comprehensive

financial planning, investment and banking solutions,

as well as access to premier investment managers

through our open architecture solution. This strategy

allows us to offer clients a unique value proposition

while providing us with growth potential. But most

importantly, this simplifies our business model and

allows us to focus on serving customers as one team.

We repaid our TARP obligation. In 2008, during the

financial crisis, Regions and many other banks issued

new preferred stock and warrants to the U.S. Treasury

under the Troubled Asset Relief Program (TARP). I

am pleased to report that in April, we completed our

repurchase of the $3.5 billion of Series A Preferred

Stock issued under TARP’s Capital Purchase Program.

The repurchase not only eliminated the payment of

$175 million in annual dividends on these securities,

but it also strengthened our ability to compete more

effectively going forward.

We achieved several milestones in 2012

that put us back in a growth mode:

REGIONS

BANK #2

BANK #3

BANK #5

BANK #4

BANK #6

BANK #7

BANK #8

BANK #9

BANK #10

78% 80% 80% 82% 86% 87% 88% 88% 88% 92%

LOAN TO DEPOSIT RATIO VS. PEERS