Regions Bank 2012 Annual Report Download - page 129

Download and view the complete annual report

Please find page 129 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

review committees noted in the previous paragraph, Regions will continue to assess and monitor disclosure controls

and procedures and internal controls over financial reporting, and will make refinements as necessary.

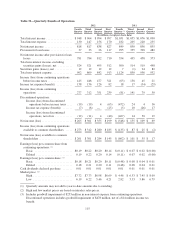

COMPARISON OF 2011 WITH 2010—CONTINUING OPERATIONS

Regions reported a net loss available to common shareholders of $429 million, or $0.34 per diluted common

share, in 2011 compared to a net loss available to common shareholders of $763 million, or $0.62 per diluted share,

in 2010. Regions reported a loss from continuing operations available to common shareholders of $25 million, or

$0.02 per diluted common share, in 2011 compared to a loss from continuing operations available to common

shareholders of $692 million, or $0.56 per diluted share, in 2010. Significant drivers of 2011 results included a

fourth quarter non-cash goodwill impairment charge of $731 (net of $14 million income tax impact) within the

former Investment Banking/Brokerage/Trust segment. Based on a relative fair value allocation, $478 million of the

impairment charge was recorded within discontinued operations and $253 million within continuing operations.

Net interest income from continuing operations was $3.4 billion in both 2011 and 2010. The net interest

margin from continuing operations (taxable-equivalent basis) was 3.07 percent in 2011, compared to 2.91 percent

during 2010. The margin improvement was driven primarily by a decrease of 34 basis points in the cost of

interest-bearing liabilities, while being partially offset by a 15 basis point decline in the overall yield on interest

earning assets. This dynamic reflected efforts to improve deposit costs and pricing on loans, while managing the

challenges posed by a low interest rate environment. Long-term interest rates in particular remained low in 2011,

pressuring yields on fixed-rate loan and securities portfolios, and contributed to the decline in the yield on

taxable securities from 3.66 percent in 2010 to 3.08 percent in 2011. The overall costs of deposits improved from

0.78 percent in 2010 to 0.49 percent in 2011.

Non-interest income from continuing operations totaled $2.1 billion in 2011, compared to $2.5 billion in

2010. The year-over-year decrease was due primarily to lower gains from both sales of securities and leveraged

lease terminations.

Service charges on deposit accounts decreased less than 1 percent in 2011 and totaled $1.2 billion in both

2011 and 2010. This modest decrease was driven by policy changes related to Regulation E, as well as a decline

in interchange income as a result of debit interchange price controls implemented in the fourth quarter of 2011.

These factors were offset by the restructuring of checking accounts from free to fee-eligible and a higher level of

customer transactions.

In 2011, mortgage income decreased $27 million, or 11 percent to $220 million. The decrease was primarily

driven by lower mortgage origination volume in 2011 as compared to 2010 due to decreased refinance activity during

2011 as compared to 2010. Mortgage originations totaled $6.3 billion in 2011 as compared to $8.2 billion in 2010. In

addition to the decrease in origination income, market valuation adjustments for mortgage servicing rights and related

derivatives subtracted $22 million and added $16 million to mortgage income in 2011 and 2010, respectively.

Regions reported net gains of $112 million from the sale of securities available for sale in 2011, compared

to net gains of $394 million in 2010. The Company’s gains for both years were due to increased sales activity

within the available-for-sale category as part of the Company’s asset/liability management strategies. In 2011,

the Company repositioned its securities portfolio and sold $7.7 billion of securities that were primarily agency

available for sale securities. The proceeds were reinvested predominately into similar securities with shorter

durations. In 2010, the Company repositioned its securities portfolio and sold $9.9 billion to mitigate prepayment

risk and extended the duration of the investment portfolio. The proceeds from the sales in 2011 and 2010 were

reinvested in U.S. government agency mortgage-backed securities classified as available for sale.

Credit card / bank card income increased $34 million in 2011 as compared to 2010. Credit card income is

derived from activity related to the Regions-branded credit card amounts purchased from FIA Card Services in

the second quarter of 2011 and any subsequent originations. Bank card income relates to commercial purchasing

cards. The increase in 2011 was primarily due to the 2011 credit card portfolio purchase.

113