Regions Bank 2012 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2012 Regions Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

|

|

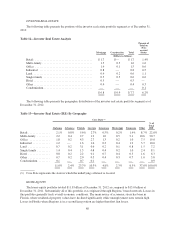

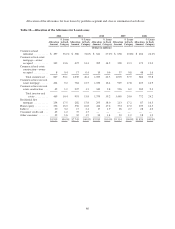

Non-performing assets totaled $1.9 billion at December 31, 2012, compared to $3.0 billion at December 31,

2011. Foreclosed properties, a subset of non-performing assets, totaled $149 million and $296 million at

December 31, 2012 and December 31, 2011, respectively. The decrease in non-performing assets and foreclosed

properties during 2012 reflects the Company’s efforts to work through problem assets and reduce the riskiest

exposures.

Based on current expectations for the economy, non-performing assets are expected to improve in 2013

compared to 2012. Economic trends such as real estate valuations, interest rates and unemployment, as well as

the level of disposition activity, will impact the future level of non-performing assets. Circumstances related to

individually large credits may result in volatility throughout 2013.

Loans past due 90 days or more and still accruing were $450 million at December 31, 2012, a slight increase

from $447 million at December 31, 2011.

At December 31, 2012, Regions had approximately $250-$350 million of potential problem commercial and

investor real estate loans that were not included in non-accrual loans, but for which management had concerns as

to the ability of such borrowers to comply with their present loan repayment terms. This is a likely estimate of

the amount of commercial and investor real estate loans that may migrate to non-accrual status in the next

quarter.

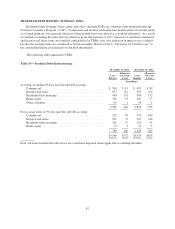

In order to arrive at the estimate of potential problem loans, personnel from geographic regions forecast

certain larger dollar loans that may potentially be downgraded to non-accrual at a future time, depending on the

occurrence of future events. These personnel consider a variety of factors, including the borrower’s capacity and

willingness to meet the contractual repayment terms, make principal curtailments or provide additional collateral

when necessary, and provide current and complete financial information including global cash flows, contingent

liabilities and sources of liquidity. A probability weighting is assigned to the listing of loans due to the inherent

level of uncertainty related to potential actions that a borrower or guarantor may take to prevent the loan from

reaching problem status. Regions assigns the probability weighting based on an assessment of the likelihood that

the necessary actions required to prevent problem loan status will occur. Additionally, for other loans (for

example, smaller dollar loans), a factor based on trends and experience is applied to determine the estimate of

potential future downgrades. Because of the inherent uncertainty in forecasting future events, the estimate of

potential problem loans ultimately represents the estimated aggregate dollar amounts of loans as opposed to an

individual listing of loans.

The majority of the loans on which the potential problem loan estimate is based are classified as substandard

accrual. Detailed disclosures for substandard accrual loans (as well as other credit quality metrics) are included in

Note 6 “Allowance for Credit Losses” to the consolidated financial statements.

89