Bank of America 2008 Annual Report Download - page 11

Download and view the complete annual report

Please find page 11 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

We modified about

230,000 home loans

during 2008 to help

avoid foreclosures

as the regulatory environment changes

in the wake of our current crisis. A

diversified revenue stream naturally

exerts a stabilizing influence on earn-

ings over time, which reassures those

charged with overseeing the strength

and stability of the industry. And

diversification also protects against

changes in the profitability of individual

financial sectors due to changing rules

and regulations.

The universal bank model has

come under a lot of fire over the past

year. But my firm belief is that, when

properly executed, the universal model

will grow in favor as the strongest

and most viable in the industry. The

successful universal bank will be one

that achieves leading positions in the

markets in which it competes; inte-

grates operations to create value for

customers; and creates a strong, bind-

ing culture across the enterprise that

supports the institutional mission.

This is the strategy we’ve followed

at Bank of America throughout my

tenure as CEO. I continue to believe it

is the strategy that will enable us to

outperform our competitors when the

economy finally strengthens.

Looking toward the future

Successfully executing our strategy,

and managing through one of the worst

economic environments in our nation’s

history, will require an extremely

capable, experienced and tight-knit

leadership team. To that point, I’d

like to review some of the leadership

changes we’ve had over the past year.

Barbara Desoer, a longtime Bank of

America leader, has moved to Calaba-

sas, California, where she is leading the

team that is hard at work reinventing

the home lending industry. Barbara’s

experience leading our Consumer

Products and Global Technology &

Operations divisions in recent years has

prepared her well for this challenge.

Bruce Hammonds, one of the

driving forces behind the evolution of

the card industry over the past three

decades, retired at the end of 2008.

Bruce successfully led our Card

Services business since our acquisi-

tion of MBNA in 2006. He has been

succeeded by Ric Struthers, who

helped create MBNA in 1982. Ric’s

deep knowledge and experience in the

card industry will be critical to our suc-

cess as we reposition that business in

a changing economic environment.

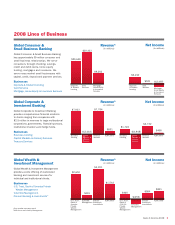

Brian Moynihan, who led our Global

Corporate & Investment Banking

business during 2008, has taken

responsibility for Global Banking &

Wealth Management, including

Commercial and Corporate Banking and

Global Product Solutions. Brian, who

led the rapid growth of our wealth

industry now faces is helping consum-

ers deleverage their household balance

sheets. For an industry that became

too dependent on interest income

to produce profits, the prospect of

significantly lower consumer borrowing

levels can be sobering. The answer, in

my view, is for financial institutions to

diversify their business models,

creating a balanced revenue stream

that includes both interest and non-

interest income from a wide range of

financial products and services that

enable customers not only to borrow,

but also to save and invest.

Bank of America’s diversified

business model should be a model

for the industry. Because we offer a

wide range of savings and investment

products as well as credit products,

we are not captive to an ever increas-

ing need for interest income. There’s

great credibility in being able to tell

customers you want to help them

achieve financial balance and finan-

cial health when you have the product

set to back it up.

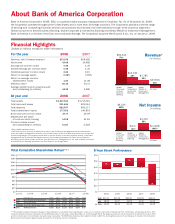

Diversification also will be helpful

Total Loans

and Leases

’06 ’07 ’08

In millions, at ye ar e nd

$706,490

$876,344 $931,446

Strong

Customer

Support

Bank of America 2008 9