Bank of America 2008 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

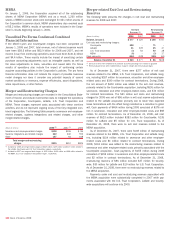

In addition to the commercial impaired loans included in the preceding

table, the Corporation recorded $903 million of consumer impaired loans

at December 31, 2008 that are individually impaired and restructured in a

troubled debt restructuring. Included in this amount were $529 million of

residential mortgage, $303 million of home equity and $71 million of

discontinued real estate. These impaired loans exclude loans that were

written down to fair value at acquisition within the scope of SOP 03-3,

which is discussed in more detail below. Included in consumer impaired

loans are performing troubled debt restructurings of $320 million for resi-

dential mortgage, $1 million for home equity and $66 million for dis-

continued real estate at December 31, 2008. There were no material

consumer impaired loans at December 31, 2007. At December 31, 2008

the Corporation had commitments of $123 million to lend additional

funds to debtors whose terms have been modified in a commercial or

consumer troubled debt restructuring.

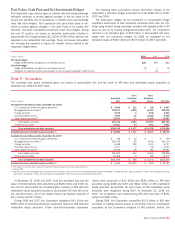

The average recorded investment in the commercial and consumer

impaired loans for 2008, 2007 and 2006 was approximately $5.0 billion,

$1.2 billion and $722 million, respectively. At December 31, 2008 and

2007, the recorded investment in impaired loans requiring an allowance

for loan and lease losses per SFAS 114 guidelines was $5.4 billion and

$1.2 billion, and the related allowance for loan and lease losses was

$720 million and $123 million. For 2008, 2007 and 2006, interest

income recognized on impaired loans totaled $105 million, $130 million

and $36 million, respectively.

At December 31, 2008 and 2007, nonperforming loans and leases,

which exclude performing troubled debt restructurings and acquired loans

that were accounted for under SOP 03-3, totaled $16.4 billion and $5.6

billion. In addition, there were consumer and commercial nonperforming

LHFS of $1.3 billion and $188 million at December 31, 2008 and 2007.

In addition, the Corporation works with customers that are experienc-

ing financial difficulty through renegotiating credit card and direct/indirect

consumer loans, while ensuring compliance with Federal Financial

Institutions Examination Council guidelines. At December 31, 2008 and

2007, the Corporation had renegotiated credit card – domestic held loans

of $2.3 billion and $1.6 billion, credit card – foreign held loans of $527

million and $483 million, and direct/indirect loans of $1.4 billion and

$810 million. These renegotiated loans are not considered non-

performing.

Countrywide SOP 03-3

Loans acquired with evidence of credit quality deterioration since origi-

nation and for which it is probable at purchase that the Corporation will

be unable to collect all contractually required payments are accounted for

under SOP 03-3. For additional information on the accounting under SOP

03-3 see the Loans and Leases section of Note 1 – Summary of Sig-

nificant Accounting Principles to the Consolidated Financial Statements.

The SOP 03-3 portfolio associated with the acquisition of LaSalle did not

materially impact results during 2008 and is excluded from the following

discussion.

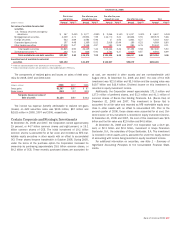

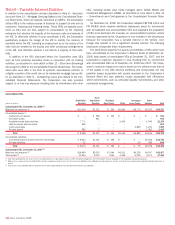

As of July 1, 2008 and December 31, 2008 Countrywide acquired

loans within the scope of SOP 03-3 had an unpaid principal balance of

$58.2 billion and $55.4 billion and a carrying value of $44.2 billion and

$42.2 billion. The following table provides details on loans obtained in

connection with the Countrywide acquisition within the scope of SOP

03-3.

Acquired Loan Information as of July 1, 2008

(Dollars in millions) Countrywide

(1)

Contractually required payments including interest $ 83,864

Less: Nonaccretable difference (20,157)

Cash flows expected to be collected

(2)

63,707

Less: Accretable yield (19,549)

Fair value of loans acquired $ 44,158

(1) Loan information as of Countrywide acquisition date, July 1, 2008.

(2) Represents undiscounted expected principal and interest cash flows at acquisition.

Under SOP 03-3, the excess of cash flows expected at acquisition

over the estimated fair value is referred to as the accretable yield and is

recognized in interest income over the remaining life of the loans. The

difference between contractually required payments at acquisition and the

cash flows expected to be collected at acquisition is referred to as the

nonaccretable difference. Changes in the expected cash flows from the

date of acquisition will either impact the accretable yield or result in a

charge to the provision for credit losses. Subsequent decreases to

expected principal cash flows will result in a charge to provision for credit

losses and a corresponding increase to allowance for loan and lease

losses. Subsequent increases in expected principal cash flows will result

in recovery of any previously recorded allowance for loan losses, to the

extent applicable, and a reclassification from nonaccretable difference to

accretable yield for any remaining increase. All changes in expected inter-

est cash flows will result in reclassifications to/from nonaccretable differ-

ences.

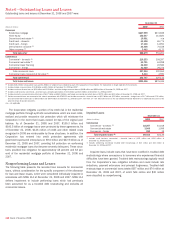

The following table provides activity for the accretable yield of loans

acquired from Countrywide within the scope of SOP 03-3 for the six

months ended December 31, 2008. During 2008, the Corporation

recorded a $750 million provision for credit losses establishing a corre-

sponding allowance for loan and lease losses at December 31, 2008.

This provision for credit losses represents deterioration in the Country-

wide SOP 03-3 portfolio subsequent to the July 1, 2008 acquisition date.

The reclassification to nonaccretable difference of $4.4 billion includes

the impact of increased prepayment speeds, lower interest rates on

variable rate loans, and principal reductions due to credit deterioration.

Accretable Yield Activity

(Dollars in millions)

Six Months Ended

December 31, 2008

Accretable yield, beginning balance

(1)

$19,549

Accretions (1,667)

Disposals (589)

Reclassifications to nonaccretable difference

(2)

(4,433)

Accretable yield, December 31, 2008 $12,860

(1) The beginning balance represents the accretable yield of loans acquired from Countrywide at July 1,

2008.

(2) Nonaccretable difference represents gross contractually required payments including interest less

expected cash flows.

Bank of America 2008

139