Bank of America 2008 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

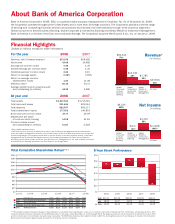

dividends and available to common

shareholders were $2.56 billion, or

$0.55 per diluted share, down from

$14.80 billion, or $3.30 per diluted

share, a year earlier. Revenue (on a

fully taxable-equivalent basis) rose 8

percent to $73.98 billion from $68.58

billion in 2007, from organic growth

and the addition of U.S. Trust, LaSalle

and Countrywide.

Return on average common share-

holders’ equity fell to 1.80 percent

from 11.08 percent. Our efficiency

ratio stayed well outside our target

range (under 50 percent), at 56.14

percent. Provision expense rose

$18.44 billion to $26.83 billion,

and nonperforming assets and net

charge-off ratios rose to 1.96 percent

and 1.79 percent, respectively.

There is no question that the reces-

sionary environment is hurting results

in all our businesses. And yet, the

news is not bad across the board. The

bulk of our losses in 2008 were the

result of severe market and economic

impacts in three of our businesses in

particular: Mortgage, Home Equity &

Insurance Services (MHEIS); Capital

Markets & Advisory Services (CMAS);

and Columbia Management. All of our

other businesses were able to gener-

ate a profit despite the harsh eco-

nomic environment, and two actually

increased net income in 2008.

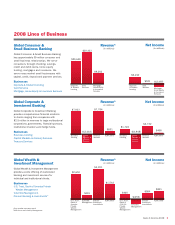

Within Global Consumer & Small

Business Banking (GCSBB), Depos-

its and Student Lending net income

increased 9 percent to $6.21 billion,

and Card Services, which has been bat-

tered by rising credit costs, still man-

aged to post net income for the year

of $521 million. In Global Corporate &

Investment Banking (GCIB), Business

Lending posted net income of $1.72

billion (down 14 percent on higher

credit costs), and Treasury Services net

income increased 28 percent to $2.73

billion. In Global Wealth & Investment

Management (GWIM), U.S. Trust earned

$460 million (down just 2 percent)

and Premier Banking and Investments

earned $584 million (a 54 percent

decrease due to higher credit costs).

The ability of our associates in

these businesses to generate sub-

stantial profits in our current economic

environment is a testament to their

skill and determination, and to the

advantages of our broad franchise. The

profitability of these businesses also

demonstrates why we value revenue

diversity so highly in our business model.

In times of severe financial stress,

what financial institutions need more

than anything is capital. Bank of

America has, for years, been among

the most well-capitalized banks in the

world. But the fourth quarter of 2008

tested even our ability to maintain a

deep well of financial resources.

In early October, to shore up capital

levels as credit losses accelerated,

we raised nearly $10 billion through

the sale of common stock and cut our

dividend on common stock in half.

Then, in mid-October, the U.S. Treasury

Department decided to use funds from

the Troubled Asset Relief Program

(TARP) to inject capital directly into the

nation’s banks through purchases of

preferred stock.

At the outset of this program, we

accepted an investment of $15 billion.

We also agreed at that time to accept

Merrill Lynch’s initial share of the TARP

funds, $10 billion, in early January.

After discussions with federal govern-

ment officials, the government agreed

to provide an additional $20 billion in

January to enable the closing of our

acquisition of Merrill Lynch.

All three preferred stock invest-

ments will yield a dividend to the U.S.

Treasury and have repayment terms for

the full amount of the investment. We

paid our first dividend to the U.S. Trea-

sury Department on all three tranches

Bank of America

holds $883 billion

in total deposits,

up 9.7% in 2008

Strong

Deposit

Growth

Tier 1

Capital Ratio

’07 ’08

8.64%

6.87%

9.15%

At year e nd

’06

4 Bank of America 2008