Bank of America 2008 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

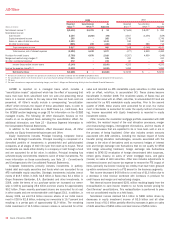

At December 31, 2008, we held $2.5 billion of purchased insurance

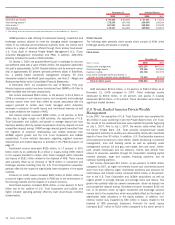

on our subprime super senior CDO exposure of which 71 percent was

provided by monolines in the form of CDS, total-return-swaps (TRS) or

financial guarantees. In the case of default, we look to the underlying

securities and then to recovery on purchased insurance. At December 31,

2008, these contracts were valued at $1.9 billion by referencing the fair

value of the CDO which is valued in the same manner as the unhedged

portion. We have adjusted these values downward by a total of $1.1 bil-

lion to date to reflect the counterparty credit risk to the issuers of the

insurance. In addition, we held collateral in the form of cash and market-

able securities of $401 million related to our purchased insurance. The

underlying insured CDOs are collateralized with approximately 38 percent

of subprime assets of which approximately 53 percent are of higher qual-

ity vintages from 2005 and prior.

In addition, at December 31, 2008 we held $1.1 billion of purchased

insurance on our non-subprime super senior CDO exposure all of which

was provided by monolines in the form of CDS, TRS or financial guaran-

tees. At December 31, 2008, these contracts were valued at

$146 million by referencing the fair value of the CDO which is valued in

the same manner as the unhedged portion. We have adjusted these

values downward by a total of $40 million to date to reflect counterparty

credit risk to the issuers of the insurance. For more information on our

credit exposure to monolines, see Industry Concentrations beginning on

page 76.

At December 31, 2008, the carrying value of the super senior

exposure in the form of cash positions, liquidity commitments, and

derivative contracts consisted of net subprime super senior exposure of

$981 million and net non-subprime super senior exposure of $2.3 billion.

In addition, we had $2.0 billion of exposure in purchased securities from

liquidated CDOs. For more information on our super senior liquidity

exposure, see the CDO discussion beginning on page 51.

The table below presents the carrying values of our subprime net

exposures including subprime collateral content and percentages of

recent vintages.

At December 31, 2008, the Corporation did not have any subprime

super senior liquidity commitments. Net other subprime super senior

exposure was $981 million at December 31, 2008. Other subprime super

senior exposure consists primarily of cash securities and CDS on CDO

positions. The collateral supporting the high grade exposure consisted of

about 45 percent subprime content, of which approximately 12 percent

was made up of 2006 and 2007 vintages while the remaining amount

was comprised of higher quality vintages from 2005 and prior. The collat-

eral supporting the mezzanine exposure consisted of approximately 35

percent subprime content, of which approximately 66 percent is com-

prised of later vintages. We recorded losses associated with these

exposures of $3.0 billion in 2008.

In addition, at December 31, 2008, we had $2.0 billion of exposure in

purchased securities from liquidated CDOs. These purchased securities

were carried at approximately 34 percent of their original net exposure

amount and approximately 27 percent of the underlying assets are sub-

prime.

We also had net non-subprime super senior exposure of $2.3 billion

which primarily included CMBS super senior exposures and highly rated

CLO exposures. The net non-subprime super senior exposure is com-

prised of $476 million of high grade super senior liquidity commitment

exposure and $1.8 billion of high grade other super senior exposure. We

recorded losses of $592 million associated with these exposures in

2008. These losses were primarily driven by spread widening and

impairments of principal from the CMBS exposure in these super senior

CDOs. These non-subprime super senior exposures experienced addi-

tional impairments of principal as credit conditions deteriorated in the

corporate debt and commercial mortgage markets during the second half

of 2008.

In addition to the super senior exposure including purchased secu-

rities at December 31, 2008, we also had exposure with a market value

of $563 million in our CDO sales and trading portfolio, of which approx-

imately $233 million was classified as subprime. This subprime exposure

is carried at approximately 22 percent of par value and includes $137

million of secondary trading positions and $96 million of positions in

legacy warehouses.

Subprime Super Senior Collateralized Debt Obligation Carrying Values

(1)

December 31, 2008

Vintage of Subprime Collateral

(Dollars in millions)

Subprime

Net

Exposure

Carrying

Value as

a Percent

of Original

Net Exposure

Subprime

Content of

Collateral

(2)

Percent in

2006/2007

Vintages

Percent in

2005/Prior

Vintages

Other super senior exposure

High grade $ 684 38% 45% 12% 88%

Mezzanine 297 56 35 66 34

Total other super senior $ 981 42

Purchased securities from liquidated CDOs 2,030 34 27 26 74

Total $3,011 36

(1) Classified as subprime when subprime consumer real estate loans make up at least 35 percent of the ultimate underlying collateral’s original net exposure value.

(2) Based on current net exposure value.

Bank of America 2008

43