Bank of America 2008 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

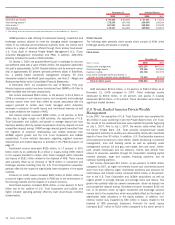

In order to ensure adequate liquidity through the full range of potential

operating environments and market conditions, we conduct our liquidity

management and business activities in a manner that will preserve and

enhance funding stability, flexibility, and diversity. Key components of this

operating strategy include a strong focus on customer-based funding,

maintaining direct relationships with wholesale market funding providers,

and maintaining the ability to liquefy certain assets when, and if, require-

ments warrant. Credit markets substantially deteriorated over the past 18

months and access to non-guaranteed market-based funding has dimin-

ished for financial institutions. For these reasons we have utilized various

government institutions (e.g., Federal Reserve, U.S. Treasury and FDIC)

funding programs to enhance our liquidity position. Many of these facili-

ties are temporary in nature, but have provided significant market stability

and have allowed many banks to maintain a healthy liquidity profile.

We develop and maintain contingency funding plans for both the

parent company and bank liquidity positions. These plans evaluate our

liquidity position under various operating circumstances and allow us to

ensure that we would be able to operate through a period of stress when

access to normal sources of funding is constrained. The plans project

funding requirements during a potential period of stress, specify and

quantify sources of liquidity, outline actions and procedures for effectively

managing through the problem period, and define roles and

responsibilities. They are reviewed and approved annually by ALCO.

Under normal business conditions, primary sources of funding for the

parent company include dividends received from its banking and non-

banking subsidiaries, and proceeds from the issuance of senior and

subordinated debt, as well as commercial paper and equity. Primary uses

of funds for the parent company include repayment of maturing debt and

commercial paper, share repurchases, dividends paid to shareholders,

and subsidiary funding through capital or debt.

Our borrowing costs and ability to raise funds are directly impacted by

our credit ratings. The credit ratings of Bank of America Corporation and

Bank of America, N.A. as of February 27, 2009 are reflected in the table

below.

The cost and availability of unsecured and secured financing are

impacted by changes in our credit ratings. A reduction in these ratings or

the ratings of other asset-backed securitizations could have an adverse

effect on our access to credit markets and the related cost of funds.

Some of the primary factors in maintaining our credit ratings include a

stable and diverse earnings stream, strong capital ratios, strong credit

quality and risk management controls, diverse funding sources and dis-

ciplined liquidity monitoring procedures.

If the Corporation’s long-term credit rating was incrementally down-

graded by one level by the rating agencies, we estimate the incremental

cost of funds and the potential lost funding would continue to be negli-

gible for senior and subordinated debt and short-term bank debt.

Additionally, we do not believe that funding requirements for VIEs and

other third party commitments would be significantly impacted. However,

if the Corporation’s short-term credit rating was downgraded by one level,

our incremental cost of funds and potential lost funding may

be material due to the negative impacts on our commercial paper pro-

grams.

Since October 2008, Bank of America has had the ability to issue

long-term senior unsecured debt through the TLGP program. This program

gives us the ability to issue AAA-rated debt backed by the full faith and

credit of the U.S. government regardless of our current credit rating. For

further information regarding this program, see Regulatory Initiatives

beginning on page 20.

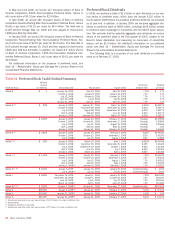

The parent company maintains a cushion of excess liquidity that

would be sufficient to fully fund the holding company and nonbank affili-

ate operations for an extended period during which funding from normal

sources is disrupted. The primary measure used to assess the parent

company’s liquidity is the “Time to Required Funding” during such a

period of liquidity disruption. Since deposits are taken by the bank operat-

ing subsidiaries and not by the parent company, this measure is not

dependent on the bank operating subsidiaries’ stable deposit balances.

This measure assumes that the parent company is unable to generate

funds from debt or equity issuance, receives no dividend income from

subsidiaries, and no longer pays undeclared dividends to shareholders

while continuing to meet nondiscretionary uses needed to maintain oper-

ations and repayment of contractual principal and interest payments

owed by the parent company and affiliated companies. Under this scenar-

io, the amount of time the parent company and its nonbank subsidiaries

can operate and meet all obligations before the current liquid assets are

exhausted is considered the “Time to Required Funding.” ALCO approves

the target range set for this metric, in months, and monitors adherence to

the target. Maintaining excess parent company cash helps to facilitate

the target range of 21 to 27 months for “Time to Required Funding” and

is the primary driver of the timing and amount of the Corporation’s debt

issuances. After incorporating the impacts of the Corporation’s acquis-

ition of Merrill Lynch, including the $10.0 billion of Series Q Preferred

Stock issued in connection with the TARP Capital Purchase Program,

“Time to Required Funding” increased to 23 months at December 31,

2008, compared to 19 months at December 31, 2007. Excluding the

impacts of Merrill Lynch acquisition and Series Q Preferred Stock issu-

ance would result in a significantly higher “Time to Required Funding” as

we had taken certain liquidity actions prior to December 31, 2008 in

preparation for the Merrill Lynch acquisition. The bank operating sub-

sidiaries maintain sufficient funding capacity to address large increases

in funding requirements such as deposit outflows. This capacity is com-

prised of available wholesale market capacity, liquidity derived from a

reduction in asset levels and various secured funding sources.

The primary sources of funding for our banking subsidiaries include

customer deposits and wholesale market-based funding. Primary uses of

funds for the banking subsidiaries include growth in the core asset portfo-

lios, including loan demand, and in the ALM portfolio. We use the ALM

portfolio primarily to manage interest rate risk and liquidity risk.

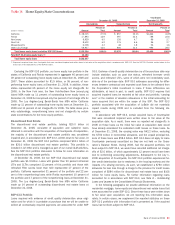

Table 11 Credit Ratings

Bank of America Corporation Bank of America, N.A.

Senior Debt

Subordinated

Debt

Commercial

Paper

Short-term

Borrowings

Long-term

Debt

Moody’s Investors Service A1 A2 P-1 P-1 Aa2

Standard & Poor’s A+ A A-1 A-1+ AA-

Fitch Ratings A+ A F1+ F1+ A+

56

Bank of America 2008