Bank of America 2008 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

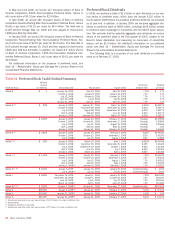

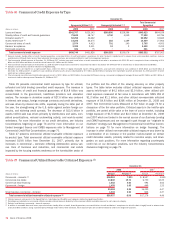

Table 17 Residential Mortgage State Concentrations

December 31, 2008

Year Ended

December 31, 2008

Outstandings Nonperforming Net Charge-offs

(Dollars in millions) Amount

Percent of

Total Amount

Percent of

Total Amount

Percent of

Total

California $ 84,847 35.6% $2,028 28.8% $411 44.4%

Florida 15,787 6.6 1,012 14.4 154 16.6

New York 15,539 6.5 255 3.6 5 0.5

Texas 10,804 4.5 315 4.5 20 2.2

Virginia 9,696 4.1 229 3.2 32 3.5

Other U.S./Foreign 101,377 42.7 3,205 45.5 303 32.8

Total residential mortgage loans (excluding SOP 03-3 loans)

$238,050 100.0% $7,044 100.0% $925 100.0%

Total SOP 03-3 residential mortgage loans (1)

9,949

Total residential mortgage loans

$247,999

(1) Represents acquired loans from Countrywide that were considered impaired and written down to fair value at the acquisition date in accordance with SOP 03-3. See page 65 for the discussion of the characteristics of

the SOP 03-3 loans.

$34.0 billion and $49.0 billion, and strengthened our Tier 1 Capital ratio

at December 31, 2008 and 2007 by 24 bps and 27 bps.

Excluding the SOP 03-3 portfolio, residential mortgage loans with

greater than 90 percent refreshed LTV represented 23 percent of the

portfolio and those loans with refreshed FICO lower than 620 represented

eight percent of the portfolio. In addition, residential mortgage loans to

borrowers in the state of California represented 36 percent and 32 per-

cent of total residential mortgage loans at December 31, 2008 and

2007. The Los Angeles-Long Beach-Santa Ana Metropolitan Statistical

Area (MSA) within California represented 13 percent and 11 percent of

the total residential mortgage portfolio at December 31, 2008 and 2007.

In addition, residential mortgage loans to borrowers in the state of Florida

represented seven percent and six percent of the total residential mort-

gage portfolio at December 31, 2008 and 2007. Additionally, 56 percent

and 40 percent of loans in California and Florida are in reference pools of

synthetic securitizations, as described above, which provide mezzanine

risk protection. Total credit risk on three percent of our mortgage loans in

Florida has been mitigated through the purchase of protection from gov-

ernment sponsored entities. The table above presents outstandings,

nonperforming loans and net charge-offs by certain state concentrations

for the residential mortgage portfolio.

The Community Reinvestment Act (CRA) encourages banks to meet

the credit needs of their communities for housing and other purposes,

particularly in neighborhoods with low or moderate incomes. At

December 31, 2008, our CRA portfolio comprised seven percent of the

total ending residential mortgage loan balances but comprised 24 per-

cent of nonperforming residential mortgage loans. This portfolio also

comprised 27 percent of residential mortgage net charge-offs during

2008. While approximately 48 percent of our residential mortgage portfo-

lio carries risk mitigation protection, only a small portion of our CRA

portfolio is covered by this protection.

Home Equity

At December 31, 2008, approximately 79 percent of the home equity

portfolio was included in GCSBB, while the remainder of the portfolio was

primarily in GWIM. Outstanding home equity loans increased $37.7 bil-

lion, or 33 percent, at December 31, 2008 compared to December 31,

2007, primarily due to the Countrywide acquisition which added approx-

imately $29.0 billion in home equity loans of which $14.2 billion is

included in the SOP 03-3 portfolio. An additional $25.0 billion in organic

growth and draws on existing lines was partially offset by paydowns and

net charge-offs. See page 65 for more information on the SOP 03-3 home

equity portfolio.

Home equity unused lines of credit totaled $107.4 billion at

December 31, 2008 compared to $120.1 billion at December 31, 2007.

The $12.7 billion decrease was driven primarily by higher account uti-

lization due to draws on existing lines as well as line management ini-

tiatives on deteriorating accounts with declining equity positions partially

offset by the addition of the Countrywide portfolio which added $4.5 bil-

lion of unused lines related to the non SOP 03-3 portfolio. The home

equity utilization rate was 52 percent at December 31, 2008 compared to

44 percent at December 31, 2007. The increase was driven by the same

factors as previously discussed as well as the addition of the Countrywide

portfolio which had a higher utilization rate.

Nonperforming home equity loans increased $1.3 billion compared to

December 31, 2007 and net charge-offs increased $3.2 billion to $3.5

billion for 2008, or 2.59 percent (2.73 percent excluding the SOP 03-3

portfolio) of total average home equity loans compared to 0.28 percent in

2007. These increases were driven by continued weakness in the hous-

ing markets, the slowing economy and seasoning of vintages originated in

periods of higher growth. Additionally, the increase was driven by high

refreshed CLTV loans in geographic areas that have experienced the most

significant declines in home prices. Home price declines coupled with the

fact that most home equity loans are secured by second lien positions

have significantly reduced and in some cases resulted in no collateral

value after consideration of the first lien position. This drove more severe

charge-offs as borrowers defaulted.

Excluding the SOP 03-3 portfolio, home equity loans with greater than

90 percent refreshed CLTV comprised 37 percent of the home equity

portfolio at December 31, 2008, and represented 85 percent of net

charge-offs for 2008. In addition, loans with a refreshed FICO lower than

620 represented 10 percent of the home equity loans at December 31,

2008. The 2006 vintage loans, which represent $34.2 billion, or 25

percent of our home equity portfolio, continue to season and have a

higher refreshed CLTV and accounted for approximately 49 percent of net

charge-offs for 2008. The portfolio’s 2007 vintages, which represent 26

percent of the portfolio, are showing similar asset quality characteristics

as the 2006 vintages and accounted for 28 percent of net charge-offs in

2008. Additionally, legacy Bank of America discontinued the program of

purchasing non-franchise originated loans in the second quarter of 2007.

These purchased loans represented only three percent of the portfolio but

accounted for 17 percent of net charge-offs for 2008.

64

Bank of America 2008