Bank of America 2008 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

|

|

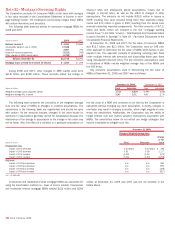

Note 21 – Mortgage Servicing Rights

The Corporation accounts for consumer MSRs at fair value with changes

in fair value recorded in the Consolidated Statement of Income in mort-

gage banking income. The Corporation economically hedges these MSRs

with certain derivatives and securities.

The following table presents activity for consumer mortgage MSRs for

2008 and 2007.

(Dollars in millions) 2008 2007

Balance, January 1

$ 3,053

$2,869

Countrywide balance, July 1, 2008

17,188

–

Additions

2,587

792

Impact of customer payments

(3,313)

(766)

Other changes in MSR market value

(6,782)

158

Balance, December 31

$12,733

$3,053

Mortgage loans serviced for investors (in billions)

$ 1,654

$ 259

During 2008 and 2007, other changes in MSR market value were

$(6.8) billion and $158 million. These amounts reflect the change in

discount rates and prepayment speed assumptions, mostly due to

changes in interest rates, as well as the effect of changes in other

assumptions. The amounts do not include $(333) million in losses in

2008 resulting from cash received being lower than expected prepay-

ments and $73 million in gains in 2007 resulting from the actual cash

received exceeding expected prepayments. The total amounts of $(7.1)

billion and $231 million are included in the line “mortgage banking

income (loss)” in the table “Level 3 – Total Realized and Unrealized Gains

(Losses) Included in Earnings” in Note 19 – Fair Value Disclosures to the

Consolidated Financial Statements.

At December 31, 2008 and 2007, the fair value of consumer MSRs

was $12.7 billion and $3.1 billion. The Corporation uses an OAS valu-

ation approach to determine the fair value of MSRs which factors in pre-

payment risk. This approach consists of projecting servicing cash flows

under multiple interest rate scenarios and discounting these cash flows

using risk-adjusted discount rates. The key economic assumptions used

in valuations of MSRs include weighted average lives of the MSRs and

the OAS levels.

Key economic assumptions used in determining the fair value of

MSRs at December 31, 2008 and 2007 were as follows:

December 31, 2008 December 31, 2007

(Dollars in millions) Fixed Adjustable Fixed Adjustable

Weighted average option adjusted spread

1.71% 6.40%

0.59% 2.54%

Weighted average life, in years

3.26 2.71

4.80 2.75

The following table presents the sensitivity of the weighted average

lives and fair value of MSRs to changes in modeled assumptions. The

sensitivities in the following table are hypothetical and should be used

with caution. As the amounts indicate, changes in fair value based on

variations in assumptions generally cannot be extrapolated because the

relationship of the change in assumption to the change in fair value may

not be linear. Also, the effect of a variation in a particular assumption on

the fair value of a MSR that continues to be held by the Corporation is

calculated without changing any other assumption. In reality, changes in

one factor may result in changes in another, which might magnify or coun-

teract the sensitivities. Additionally, the Corporation has the ability to

hedge interest rate and market valuation fluctuations associated with

MSRs. The sensitivities below do not reflect any hedge strategies that

may be undertaken to mitigate such risk.

December 31, 2008

Change in Weighted Average Lives

(Dollars in millions) Fixed Adjustable

Change

in Fair

Value

Prepayment rates

Impact of 10% decrease 0.23 years 0.13 years $ 786

Impact of 20% decrease 0.51 0.28 1,717

Impact of 10% increase (0.20) (0.11) (674)

Impact of 20% increase (0.36) (0.20) (1,258)

OAS level

Impact of 100 bps decrease n/a n/a 460

Impact of 200 bps decrease n/a n/a 955

Impact of 100 bps increase n/a n/a (428)

Impact of 200 bps increase n/a n/a (827)

n/a = not applicable

Commercial and residential reverse mortgage MSRs are accounted for

using the amortization method (i.e., lower of cost or market). Commercial

and residential reverse mortgage MSRs totaled $323 million and $294

million at December 31, 2008 and 2007 and are not included in the

tables above.

182

Bank of America 2008