Bank of America 2008 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

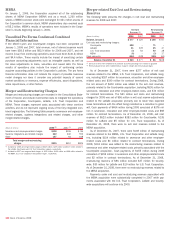

The Corporation executes the majority of its derivative positions in the

over-the-counter market with large, international financial institutions,

including broker/dealers and, to a lesser degree with a variety of other

investors. The Corporation is subject to counterparty credit risk in the

event that these counterparties fail to perform under the terms of their

contracts and records valuation adjustments against the derivative assets

to reflect counterparty credit risk. Substantially all of the derivative trans-

actions are executed on a daily margin basis. Therefore, events such as a

credit downgrade (depending on the ultimate rating level) or a breach of

credit covenants would typically require an increase in the amount of col-

lateral required of the counterparty (where applicable), and/or allow the

Corporation to take additional protective measures such as early termi-

nation of all trades. Further, as discussed above, the Corporation enters

into legally enforceable master netting agreements which reduce risk by

permitting the closeout and netting of transactions with the same

counterparty upon the occurrence of certain events. During 2008, valu-

ation adjustments of $3.2 billion were recognized as trading account

losses for counterparty credit risk. At December 31, 2008, the cumulative

counterparty credit risk valuation adjustment that was netted against the

derivative asset balance was $4.0 billion.

In addition, the fair value of the Corporation’s derivative liabilities is

adjusted to reflect the impact of the Corporation’s credit quality. During

2008, valuation adjustments of $364 million were recognized as trading

account profits for changes in the Corporation’s credit risk. At

December 31, 2008, the Corporation’s cumulative credit risk valuation

adjustment that was netted against the derivative liabilities balance was

$573 million.

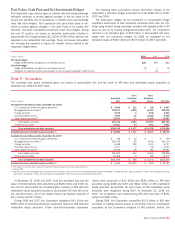

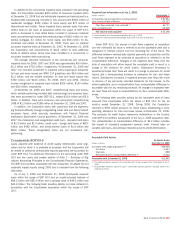

Credit Derivatives

The Corporation enters into credit derivatives primarily to facilitate client

transactions and to manage credit risk exposures. Credit derivatives

derive value based on an underlying third party-referenced obligation or a

portfolio of referenced obligations and generally require the Corporation

as the seller of credit protection to make payments to a buyer upon the

occurrence of a predefined credit event. Such credit events generally

include bankruptcy of the referenced credit entity and failure to pay under

the obligation, as well as acceleration of indebtedness and payment

repudiation or moratorium. For credit derivatives based on a portfolio of

referenced credits or credit indices, the Corporation may not be required

to make payment until a specified amount of loss has occurred and/or

may only be required to make payment up to a specified amount.

Credit derivative instruments in which the Corporation is the seller of

credit protection and their expiration at December 31, 2008 are summar-

ized in the table below. These instruments have been classified as

investment and non-investment grade based on the credit quality of the

underlying reference name within the credit derivative.

For most credit derivatives, the notional value represents the max-

imum amount payable by the Corporation. However, the Corporation does

not exclusively monitor its exposure to credit derivatives based on

notional value because this measure does not take into consideration the

probability of occurrence. As such, the notional value is not a reliable

indicator of the Corporation’s exposure to these contracts. Instead, a risk

framework is used to define risk tolerances and establish limits to help to

ensure that certain credit risk-related losses occur within acceptable,

predefined limits.

The Corporation may economically hedge its exposure to credit

derivatives by entering into a variety of offsetting derivative contracts and

security positions. For example, in certain instances, the Corporation may

purchase credit protection with identical underlying referenced names to

offset its exposure. At December 31, 2008, the carrying value and

notional value of credit protection sold in which the Corporation held

purchased protection with identical underlying referenced names was

$92.4 billion and $819.4 billion.

ALM Activities

Interest rate contracts and foreign exchange contracts are utilized in the

Corporation’s ALM activities. The Corporation maintains an overall inter-

est rate risk management strategy that incorporates the use of interest

rate contracts to minimize significant fluctuations in earnings that are

caused by interest rate volatility. The Corporation’s goal is to manage

interest rate sensitivity so that movements in interest rates do not sig-

nificantly adversely affect net interest income. As a result of interest rate

fluctuations hedged fixed-rate assets and liabilities appreciate or depreci-

ate in market value. Gains or losses on the derivative instruments that

are linked to the hedged fixed-rate assets and liabilities are expected to

substantially offset this unrealized appreciation or depreciation. Interest

income and interest expense on hedged variable-rate assets and

liabilities increase or decrease as a result of interest rate fluctuations.

Gains and losses on the derivative instruments that are linked to these

hedged assets and liabilities are expected to substantially offset this

variability in earnings.

Interest rate contracts, which are generally non-leveraged generic inter-

est rate and basis swaps, options and futures, allow the Corporation to

manage its interest rate risk position. Non-leveraged generic interest rate

swaps involve the exchange of fixed-rate and variable-rate interest pay-

ments based on the contractual underlying notional amount. Basis swaps

involve the exchange of interest payments based on the contractual under-

lying notional amounts, where both the pay rate and the receive rate are

floating rates based on different indices. Option products primarily consist

of caps, floors and swaptions. Futures contracts used for the Corpo-

ration’s ALM activities are primarily index futures providing for cash pay-

ments based upon the movements of an underlying rate index.

The Corporation uses foreign currency contracts to manage the foreign

exchange risk associated with certain foreign currency-denominated

assets and liabilities, as well as the Corporation’s investments in foreign

subsidiaries. Foreign exchange contracts, which include spot and forward

contracts, represent agreements to exchange the currency of one country

for the currency of another country at an agreed-upon price on an agreed-

upon settlement date. Exposure to loss on these contracts will increase

or decrease over their respective lives as currency exchange and interest

rates fluctuate.

(Dollars in millions)

Maximum

Payout/Notional

(1)

Less than One

Year

One to

Three Years

Three to

Five Years

Over Five

Years

Carrying

Value

Investment grade

(2)

$ 801,886 $1,039 $13,062 $32,594 $29,153 $ 75,848

Non-investment grade

(3)

198,148 1,483 9,222 19,243 13,012 42,960

Total $1,000,034 $2,522 $22,284 $51,837 $42,165 $118,808

(1) Excludes total return swaps as they are not specifically linked to a credit index or credit event.

(2) The Corporation considers ratings of BBB- or higher to meet the definition of investment grade.

(3) Includes non-rated credit derivative instruments.

134

Bank of America 2008