Bank of America 2008 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

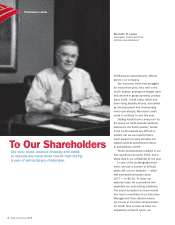

management products, and securities

sales and trading.

We are already seeing business

activity levels beginning to pick up. We

now have leading positions in markets

all over the world, and our investment

banking team is among the most tal-

ented and experienced in the business.

On the far side of the storm we’re

in, I believe there is tremendous

opportunity in both of these acquisi-

tions. And I am excited about working

with our new associates to seize it.

Managing risk and reward

We are in the business of taking risk —

lending to individuals and businesses

to fuel the economy. It is also our

business to manage that risk. Our

industry as a whole did a poor job on

that front in the lead-up to our current

crisis. The institutions that did the

worst job are no longer with us. Those

that did a better job have endured.

But no one I know of in this industry

is crowing. We all have learned — or

relearned — hard lessons.

The challenges created by the

economic and market environment do

not excuse Bank of America’s perfor-

mance. But they do help explain it.

One of the biggest issues we faced

over the course of the most recent

growth cycle was the speed and degree

of fundamental, structural changes that

were happening throughout the econ-

omy. New market participants were

emerging and growing rapidly, including

sovereign wealth funds, hedge funds

and other global investors. Structured

products, thanks to advancing technol-

ogy, grew more complex by the day.

The speed and volume of securities

creation and trading increased expo-

nentially. Markets and risks grew ever

more interconnected. And the sheer

volume of information in the system

that needed to be tracked, monitored,

analyzed and understood led to a grow-

ing opacity — the opposite of what you

want when you’re managing risk.

As we work our way through the

current cycle, we’re applying the

lessons we’ve learned the hard way.

One lesson is that we must not rely

too heavily on mathematical risk model-

ing in assessing risks. The models are

sophisticated, but they are only as good

as the assumptions of the people who

create them, and only as well-informed

as the data we feed into them. We

have to balance our risk modeling

abilities with what we know at any given

moment about our customers, clients

and portfolios; a commonsense under-

standing of economic fundamentals;

and our knowledge of business cycles.

And we must have the courage to test

the former against the latter when

economic facts and risk assessments

seem out of balance.

Another lesson is that we need

to return to the fundamentals in our

business. We are producing simpler

and more transparent products to

meet our customers’ current financial

needs, and developing those that will

help them when the cycle turns. We

also are recalibrating our assessments

of risk factors like customer credit-

worthiness, portfolio concentrations

and market trends to account for new

economic realities. And we are using

new tools to manage all these risks

more effectively.

Finally, we’ve concluded that, while

organizational structure can be impor-

tant in the way we manage risk, it is not

the primary determinant of success.

The most important factors are people

and culture. When we have the right

people in the right assignments —

people with not only intelligence and

insight, but also the courage to engage

teammates on thorny risk issues — and

when we have nurtured a risk culture

that welcomes and encourages debate,

we usually get to the right answer.

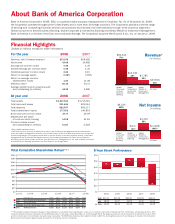

Total Deposits

’06 ’07 ’08

In millions, at ye ar e nd

$693,497

$805,177 $882,997

Bank of America

serves one of every

two U.S. households

and 99% of the U.S.

Fortune 500

Strong

Market

Share

6 Bank of America 2008