Bank of America 2008 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

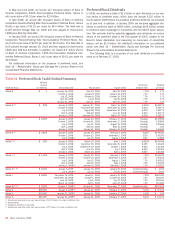

Credit Risk Management

The housing downturn and the financial market disruptions that began in

the second half of 2007 have continued to affect the economy and the

financial services sector in 2008. The housing downturn and the broader

economic slowdown accelerated during the second half of 2008 and

negatively impacted the credit quality of both our consumer and commer-

cial portfolios. The depth and breadth of the downturn as well as the

resulting impacts on the credit quality of our portfolios remain unclear.

However, we expect continued market turbulence and economic

uncertainty to continue well into 2009. This will result in higher credit

losses and provision for credit losses in future periods.

Credit risk is the risk of loss arising from the inability of a borrower or

counterparty to meet its obligations. Credit risk can also arise from opera-

tional failures that result in an erroneous advance, commitment or

investment of funds. We define the credit exposure to a borrower or coun-

terparty as the loss potential arising from all product classifications

including loans and leases, deposit overdrafts, derivatives, assets

held-for-sale and unfunded lending commitments that include loan com-

mitments, letters of credit and financial guarantees. Derivative positions

are recorded at fair value and assets held-for-sale are recorded at fair

value or the lower of cost or fair value. Certain loans and unfunded com-

mitments are accounted for at fair value in accordance with SFAS 159.

Credit risk for these categories of assets is not accounted for as part of

the allowance for credit losses but as part of the fair value adjustment

recorded in earnings in the period incurred. For derivative positions, our

credit risk is measured as the net replacement cost in the event the

counterparties with contracts in a gain position to us fail to perform under

the terms of those contracts. We use the current mark-to-market value to

represent credit exposure without giving consideration to future

mark-to-market changes. The credit risk amounts take into consideration

the effects of legally enforceable master netting agreements and cash

collateral. Our consumer and commercial credit extension and review

procedures take into account funded and unfunded credit exposures. For

additional information on derivatives and credit extension commitments,

see Note 4 – Derivatives and Note 13 – Commitments and Contingencies

to the Consolidated Financial Statements.

For credit risk purposes, we evaluate our consumer businesses on

both a held and managed basis. Managed basis assumes that credit card

loans that have been securitized were not sold and presents earnings on

these loans in a manner similar to the way loans that have not been sold

(i.e., held loans) are presented. We evaluate credit performance on a

managed basis as the credit card receivables that have been securitized

are subject to the same underwriting, servicing, ongoing monitoring and

collection standards as held loans. In addition to the discussion of credit

quality statistics of both held and managed credit card loans included in

this section, refer to the Card Services discussion on page 35. For addi-

tional information on our managed portfolio and securitizations, see Note

8 – Securitizations to the Consolidated Financial Statements.

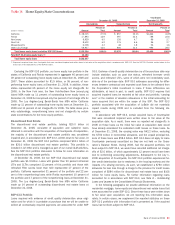

We manage credit risk based on the risk profile of the borrower or

counterparty, repayment sources, the nature of underlying collateral, and

other support given current events, conditions and expectations. We

classify our portfolios as either consumer or commercial and monitor

credit risk in each as discussed below.

We continue to refine our credit standards to meet the changing

economic environment. We have adjusted our underwriting criteria, as

well as enhanced our line management and collection strategies across

the consumer businesses in an attempt to mitigate losses. We have

increased our collections and customer assistance infrastructure in order

to enhance customer support.

In our domestic consumer credit card business, we have implemented

a number of initiatives to mitigate losses including increased use of

judgmental lending, adjusted underwriting, account and line management

standards, particularly in higher-risk geographies, and increased collec-

tions staffing levels. In response to the significant deterioration in our

consumer real estate portfolio we have implemented initiatives including

underwriting changes on newly originated consumer real estate loans

which increased the minimum FICO score and reduced the maximum

loan-to-value (LTVs) and combined loan-to-values (CLTVs). Additional LTV

and CLTV reductions were implemented for higher risk geographies. In our

home equity portfolio, we have also reduced unfunded lines on deteriorat-

ing accounts with declining equity positions.

In response to weakness in our direct/indirect portfolio, we have

implemented several initiatives to mitigate losses. In our unsecured lend-

ing business we have increased the use of judgmental lending and tighter

underwriting and account management standards for higher risk custom-

ers and higher-risk geographies. In our automotive and dealer-related

portfolios, we have tightened underwriting criteria and improved the risk-

based pricing for purchased loans.

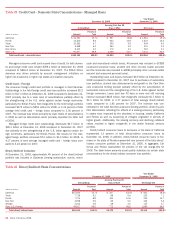

To mitigate losses in the commercial businesses, we have increased

the frequency and intensity of portfolio monitoring, hedging activity and

our efforts in managing the exposure when we begin to see signs of dete-

rioration. As part of our underwriting process we have increased scrutiny

around stress analysis and required pricing and structure to reflect cur-

rent market dynamics. Given the volatility of the financial markets, we

increased the frequency of various tests designed to understand what the

volatility could mean to our underlying credit risk. Given the single name

risk associated with the problems in the financial markets, we used a

real-time counterparty event management process to monitor key

counterparties. A number of initiatives have also been implemented in our

small business commercial – domestic portfolio including changes to

underwriting thresholds, augmented by a granular decision making proc-

ess by experienced underwriters including increasing minimum FICO

scores and lowering initial line assignments. We have also decreased

credit lines on higher risk customers in higher risk states and industries.

Further, we are increasing our customer assistance and collections

infrastructure and have instituted a number of other initiatives related to

our credit portfolios in an attempt to mitigate losses and enhance our

support for our customers. To help homeowners avoid foreclosure, Bank

of America and Countrywide modified approximately 230,000 home loans

during 2008. The majority of these home retention solutions were

extended as part of a broader initiative to offer modifications for approx-

imately $100 billion in mortgage financing for up to 630,000 borrowers

over the next several years. In addition to being committed to the loan

modification programs the Corporation continued to focus on lending by

extending more than $115 billion of new credit during the fourth quarter.

For more information, see Recent Events on page 22.

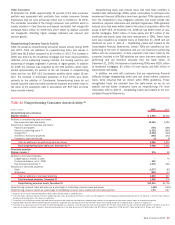

On July 1, 2008, the Corporation acquired Countrywide creating one of

the largest mortgage originators and servicers. We will continue our prac-

tice of not originating subprime mortgages and certain nontraditional

mortgages, and as such will not offer products such as Countrywide’s

pay-option and payment advantage ARMs (pay option loans), which we

classify as discontinued real estate in the Consumer Portfolio Credit Risk

Management discussion. We have significantly curtailed the production of

other nontraditional mortgages, such as certain low-documentation loans.

In addition, we will continue to offer first-lien mortgages conforming to

the underwriting standards of GSEs and the government, including loans

supported by the FHA and the Department of Veterans Affairs and other

loans designed for low and moderate income borrowers (e.g., Community

Reinvestment Act loans). We will also continue to offer first-lien

non-conforming loans, interest-only fixed-rate and ARMs that are subject

to a 10-year minimum interest-only period, and fixed-period ARMs.

Bank of America 2008

61