Bank of America 2008 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

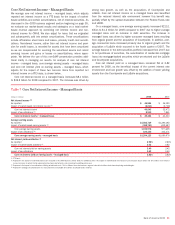

Card Services

Card Services, which excludes the results of Debit Card (included in

Deposits and Student Lending), provides a broad offering of products,

including U.S. Consumer and Business Card, Unsecured Lending, and

International Card. We offer a variety of co-branded and affinity credit card

products and are one of the leading issuers of credit cards through

endorsed marketing in the U.S. and Europe.

The Corporation reports its Card Services results on a managed basis,

which is consistent with the way that management evaluates the results

of Card Services. Managed basis assumes that securitized loans were

not sold and presents earnings on these loans in a manner similar to the

way loans that have not been sold (i.e., held loans) are presented. Loan

securitization is an alternative funding process that is used by the Corpo-

ration to diversify funding sources. Loan securitization removes loans

from the Consolidated Balance Sheet through the sale of loans to an

off-balance sheet QSPE which is excluded from the Corporation’s Con-

solidated Financial Statements in accordance with GAAP.

Securitized loans continue to be serviced by the business and are

subject to the same underwriting standards and ongoing monitoring as

held loans. In addition, excess servicing income is exposed to similar

credit risk and repricing of interest rates as held loans. The financial

market disruptions that began in 2007 continued to impact the economy

and financial services sector. Late in the third quarter and into the fourth

quarter of 2008, liquidity for asset-backed securities disappeared and

spreads rose to historic highs, negatively impacting our credit card securi-

tization programs. If these conditions persist, it could adversely affect our

ability to access these markets at favorable terms. For more information,

see the Liquidity Risk and Capital Management discussion on page 55.

Net income decreased $3.1 billion, or 85 percent, to $521 million

compared to 2007 as growth in net interest income and noninterest

income was more than offset by higher provision for credit losses of $8.2

billion.

Net interest income grew $2.9 billion, or 18 percent, to $19.2 billion

driven by higher managed average loans and leases of $21.3 billion, or

10 percent, combined with the beneficial impact of the decrease in short-

term interest rates on our funding costs.

Noninterest income increased $218 million, or two percent, to $9.2

billion as other income benefited from the $388 million gain related to

Card Services’ allocation of the Visa IPO as well as a $283 million gain

on the sale of a card portfolio. These increases were partially offset by

the decrease in card income of $377 million, or five percent, due to the

unfavorable change in the value of the interest-only strip and decreases in

interchange income driven by reduced retail volume and late fees.

Provision for credit losses increased $8.2 billion, or 73 percent, to

$19.6 billion compared to 2007 primarily driven by portfolio deterioration

and higher bankruptcies from impacts of the slowing economy, a lower

level of foreign securitizations and growth-related seasoning of the portfo-

lio. For further discussion, see Provision for Credit Losses on page 81.

Noninterest expense decreased $238 million, or three percent, to

$8.1 billion compared to 2007, as the impact of certain benefits asso-

ciated with the Visa IPO transactions and lower marketing expense were

partially offset by higher personnel and technology-related expenses from

increased customer assistance and collections infrastructure.

Key Statistics

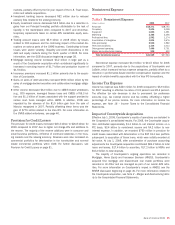

(Dollars in millions) 2008 2007

Card Services

Average – total loans and leases:

Managed

$229,347

$208,094

Held

124,946

104,810

Period end – total loans and leases:

Managed

226,081

225,889

Held

125,121

122,922

Managed net losses

(1)

:

Amount

15,321

10,088

Percent

(3)

6.68%

4.85%

Credit Card (2)

Average – total loans and leases:

Managed

$184,246

$171,376

Held

79,845

70,242

Period end – total loans and leases:

Managed

182,234

183,691

Held

81,274

80,724

Managed net losses

(1)

:

Amount

11,382

8,214

Percent

(3)

6.18%

4.79%

(1) Represents net charge-offs on held loans combined with realized credit losses associated with the

securitized loan portfolio.

(2) Includes U.S. consumer, foreign and U.S. government card. Does not include business card and

unsecured lending.

(3) Ratios are calculated as managed net losses divided by average outstanding managed loans and leases

during the year.

The table above and the following discussion presents select key

indicators for the Card Services and credit card portfolios.

Managed Card Services net losses increased $5.2 billion to $15.3

billion, or 6.68 percent of average outstandings, compared to $10.1 bil-

lion, or 4.85 percent in 2007. This increase was driven by portfolio

deterioration and higher bankruptcies reflecting the impacts of the slow-

ing economy. Additionally, portfolio deterioration during the second half of

2008 and growth-related seasoning of the unsecured lending portfolio

drove a portion of the increase.

Managed credit card net losses increased $3.2 billion to $11.4 bil-

lion, or 6.18 percent of average credit card outstandings, compared to

$8.2 billion, or 4.79 percent in 2007. The increase was driven by portfo-

lio deterioration and higher bankruptcies reflecting the impacts of a slow-

ing economy.

For more information on credit quality, see Consumer Portfolio Credit

Risk Management beginning on page 62.

Bank of America 2008

35