Bank of America 2008 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

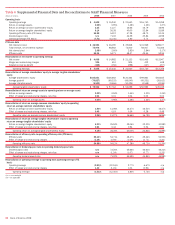

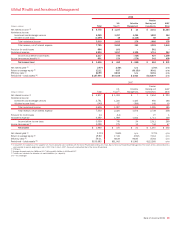

December 31 Average Balance

(Dollars in millions) 2008 2007 2008 2007

Total loans and leases

$340,692

$326,042 $337,352 $274,725

Total trading-related assets

247,552

308,316 341,544 362,195

Total market-based earning assets

(1)

244,914

360,276 368,751 412,587

Total earning assets

(2)

589,431

675,407 699,708 677,215

Total assets

(2)

707,170

778,158 816,832 771,219

Total deposits

251,798

246,242 239,097 219,891

(1) Total market-based earning assets represents earning assets included in CMAS but excludes loans that are accounted for at fair value in accordance with SFAS 159.

(2) Total earning assets and total assets include asset allocations to match liabilities (i.e., deposits).

GCIB provides a wide range of financial services to both our issuer

and investor clients that range from business banking clients to large

international corporate and institutional investor clients using a strategy

to deliver value-added financial products, transaction and advisory serv-

ices. GCIB’s products and services are delivered from three primary busi-

nesses: Business Lending, CMAS, and Treasury Services, and are

provided to our clients through a global team of client relationship

managers and product partners. In addition, ALM/Other includes the

results of ALM activities and other GCIB activities. Our clients are sup-

ported through offices in 22 countries that are divided into four distinct

geographic regions: U.S. and Canada; Asia; Europe, Middle East, and

Africa; and Latin America. For more information on our foreign operations,

see Foreign Portfolio beginning on page 79.

On January 1, 2009, we acquired Merrill Lynch in exchange for com-

mon and preferred stock with a value of $29.1 billion, creating a premier

financial services franchise with significantly enhanced wealth manage-

ment, investment banking and international capabilities. In addition, the

acquisition adds strengths in debt and equity underwriting, sales and

trading, and global merger and acquisition advice, creating significant

opportunities to deepen relationships with corporate and institutional

clients around the globe. For more information related to the Merrill Lynch

acquisition, see Note 2 – Merger and Restructuring Activity to the Con-

solidated Financial Statements.

During 2008, we reached an agreement with the Massachusetts

Securities Division under which we offered to purchase at par ARS held by

our retail customers, including individual investors, businesses, and

charitable organizations. Further in October 2008, we announced other

agreements in principle with the SEC, the Office of the NYAG, and the

North American Securities Administrators Association. These agreements

are substantially similar except that the agreement with the NYAG

requires the payment of a penalty. These agreements will cover approx-

imately $5.3 billion in ARS held by an estimated 5,600 of our customers.

We purchased approximately $4.7 billion of securities, $2.7 billion of

which were purchased by GWIM and $2.0 billion of which were purchased

by GCIB. During the year, we recognized mark-to-market losses of $181

million and $312 million in GWIM and GCIB on these securities and a

penalty of $50 million which was equally allocated to GWIM and GCIB.As

of December 31, 2008, our remaining commitment to purchase ARS was

$675 million of which $537 million related to GWIM and $138 million

related to GCIB.

Net income decreased $524 million to a net loss of $14 million and

total revenue decreased $211 million, or two percent, to $13.4 billion in

2008 compared to 2007. These decreases were driven by losses result-

ing from our CDO and other trading exposures. Additionally, we experi-

enced an increase in provision for credit losses which was partially offset

by higher net interest income and a decrease in noninterest expense.

Net interest income increased $5.3 billion, or 48 percent, driven

primarily by higher market-based net interest income which benefited from

the steepening of the yield curve and product mix. Additionally, net inter-

est income benefited from growth in average loans and leases of $62.6

billion, or 23 percent, combined with a higher margin on ALM activities.

These benefits were partially offset by the impact of competitive deposit

pricing and a shift in the deposit product mix as more customers moved

their deposits to higher yielding products. The growth in average loans

and deposits was due to the LaSalle merger as well as organic growth.

Noninterest income decreased $5.5 billion to a loss of $3.1 billion in

2008 compared to 2007, driven by declines in trading account profits

(losses) of $1.0 billion and other income of $5.2 billion. For more

information on the aforementioned decreases, see the CMAS discussion.

Additionally, noninterest income benefited from the favorable impact of

the Visa IPO transactions and an increase in service charge income.

The provision for credit losses increased $2.4 billion to $3.1 billion in

2008 compared to 2007 reflecting higher credit costs in Business Lend-

ing. For further information, see the Business Lending discussion.

Noninterest expense decreased $1.8 billion, or 15 percent, mainly

due to a reduction in performance-based incentive compensation in CMAS

and the impact of certain benefits associated with the Visa IPO trans-

actions, partially offset by the addition of LaSalle.

Business Lending

Business Lending provides a wide range of lending-related products and

services to our clients through client relationship teams along with vari-

ous product partners. Products include commercial and corporate bank

loans and commitment facilities which cover our business banking cli-

ents, middle-market commercial clients and our large multinational corpo-

rate clients. Real estate lending products are issued primarily to public

and private developers, homebuilders and commercial real estate firms.

Leasing and asset-based lending products offer our clients innovative

financing products. Products also include indirect consumer loans which

allow us to offer financing through automotive, marine, motorcycle and

recreational vehicle dealerships across the U.S. Business Lending also

contains the results for the economic hedging of our risk to certain

middle-market and real estate-related commercial credit counterparties

utilizing various risk mitigation tools.

Net income decreased $278 million, or 14 percent, to $1.7 billion in

2008 compared to 2007 as increases in net interest income and non-

interest income combined with a decrease in noninterest expense were

more than offset by increases in provision for credit losses.

Net interest income increased $1.3 billion, or 26 percent, driven by

average loan growth of 25 percent to $311.0 billion. The increase in

average loans and leases was attributable to the LaSalle acquisition and

organic growth primarily in commercial – domestic and real estate loans.

The increase in noninterest income of $443 million, or 38 percent,

was mainly driven by improved economic hedging results of our exposures

to certain commercial clients and an increase in service charges.

The provision for credit losses increased $2.4 billion to $3.1 billion in

2008 compared to 2007, reflecting reserve increases and higher charge-

offs primarily due to the continued weakness in the housing markets on

the homebuilder portfolio. Also contributing to this increase were higher

commercial – domestic and foreign net charge-offs which increased from

Bank of America 2008

39