Bank of America 2008 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

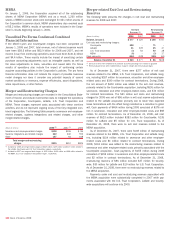

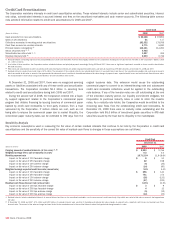

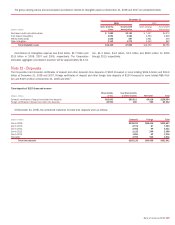

Note 7 – Allowance for Credit Losses

The following table summarizes the changes in the allowance for credit losses for 2008, 2007 and 2006.

(Dollars in millions) 2008 2007 2006

Allowance for loan and lease losses, January 1

$ 11,588

$ 9,016 $ 8,045

Adjustment due to the adoption of SFAS 159

–

(32) –

Loans and leases charged off

(17,666)

(7,730) (5,881)

Recoveries of loans and leases previously charged off

1,435

1,250 1,342

Net charge-offs

(16,231)

(6,480) (4,539)

Provision for loan and lease losses

26,922

8,357 5,001

Other

(1)

792

727 509

Allowance for loan and lease losses, December 31

23,071

11,588 9,016

Reserve for unfunded lending commitments, January 1

518

397 395

Adjustment due to the adoption of SFAS 159

–

(28) –

Provision for unfunded lending commitments

(97)

28 9

Other

(2)

–

121 (7)

Reserve for unfunded lending commitments, December 31

421

518 397

Allowance for credit losses, December 31

$ 23,492

$12,106 $ 9,413

(1) The 2008 amount includes the $1.2 billion addition of the Countrywide allowance for loan losses as of July 1, 2008. The 2007 amount includes the $725 million and $25 million additions of the LaSalle and U.S. Trust

Corporation allowance for loan losses as of October 1, 2007 and July 1, 2007. The 2006 amount includes the $577 million addition of the MBNA allowance for loan losses as of January 1, 2006.

(2) The 2007 amount includes the $124 million addition of the LaSalle reserve for unfunded lending commitments as of October 1, 2007.

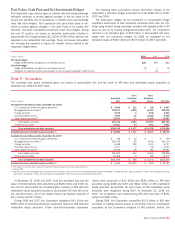

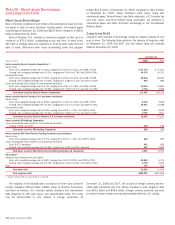

Note 8 – Securitizations

The Corporation routinely securitizes loans and debt securities. These

securitizations are a source of funding for the Corporation in addition to

transferring the economic risk of the loans or debt securities to third par-

ties. In a securitization, various classes of debt securities may be issued

and are generally collateralized by a single class of transferred assets

which most often consist of residential mortgages, but may also include

commercial mortgages, credit card receivables, home equity loans, auto-

mobile loans or mortgage-backed securities. The securitized loans may be

serviced by the Corporation or by third parties. With each securitization,

the Corporation may retain a portion of the securities, subordinated

tranches, interest-only strips, subordinated interests in accrued interest

and fees on the securitized receivables, and, in some cases, over-

collateralization and cash reserve accounts, all of which are called

retained interests. These retained interests are recorded in other assets,

AFS debt securities, or trading account assets and are carried at fair

value or amounts that approximate fair value with changes recorded in

income or accumulated OCI. Changes in the fair value of credit card

related interest-only strips are recorded in card income. In addition, the

Corporation may enter into derivatives with the securitization trust to miti-

gate the trust’s interest rate or foreign exchange risk. These derivatives

are entered into at market terms and are generally senior in payment. The

Corporation also may serve as the underwriter and distributor of the

securitization, serve as the administrator of the trust, and from time to

time, make markets in securities issued by the securitization trusts. For

more information related to derivatives, see Note 4 – Derivatives to the

Consolidated Financial Statements.

First Lien Mortgage-related Securitizations

The Corporation securitizes a portion of its residential mortgage loan origi-

nations in conjunction with or shortly after loan closing. In addition, the

Corporation may, from time to time, securitize commercial mortgages and

first lien residential mortgages that it originates or purchases from other

entities.

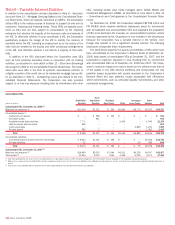

The following table summarizes selected information related to mortgage securitizations for 2008 and 2007.

Residential Mortgage

Non-Agency

Agency Prime Subprime Alt-A

Commercial

Mortgage

(Dollars in millions) 2008 2007 2008 2007 2008

(1)

2007 2008 2007 2008 2007

Cash proceeds from new

securitizations

(2)

$ 123,653

$ 50,866

$ 1,038

$17,499

$ 1,377

$–

$–

$ 745

$ 3,557

$15,409

Gains on securitizations

(3, 4)

25

52

2

27

24

–

–

1

29

103

Cash flows received on residual

interests

–

–

6

–

33

–

4

–

–

–

Principal balance outstanding

(5, 6)

1,123,916

192,627

111,683

44,565

57,933

–

136,027

12,157

55,403

47,587

Senior securities held

13,815

4,702

4,926

5,261

121

–

2,946

553

184

584

Subordinated securities held

–

–

43

143

4

–

18

36

136

77

Residual interests held

–

–

–

–

13

–

–

–

7

13

(1) The cash proceeds related to the non-agency subprime securitization were received during 2007; however, this securitization did not achieve sale accounting until 2008.

(2) The Corporation sells residential mortgage loans to government-sponsored agencies in the normal course of business and receives mortgage-backed securities in exchange. These mortgage-backed securities are then

subsequently sold into the market to third party investors for cash proceeds.

(3) Net of hedges

(4) Substantially all of the residential mortgages securitized are initially classified as LHFS and recorded at fair value under SFAS 159. As such, gains are recognized on these LHFS prior to securitization. During 2008 and

2007, the Corporation recognized $1.6 billion and $212 million of gains on these LHFS.

(5) Generally, the Corporation as transferor will service the sold loans and thus recognize an MSR upon securitization. See additional information to follow related to the Corporation’s role as servicer and Note 21 –

Mortgage Servicing Rights to the Consolidated Financial Statements.

(6) The increase in principal balance outstanding at December 31, 2008 from the prior year was due to the addition of Countrywide securitizations.

140

Bank of America 2008