Bank of America 2008 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

|

|

The sensitivities in the preceding table are hypothetical and should be

used with caution. As the amounts indicate, changes in fair value based

on variations in assumptions generally cannot be extrapolated because

the relationship of the change in assumption to the change in fair value

may not be linear. Also, the effect of a variation in a particular assump-

tion on the fair value of an interest that continues to be held by the

Corporation is calculated without changing any other assumption. In real-

ity, changes in one factor may result in changes in another, which might

magnify or counteract the sensitivities. Additionally, the Corporation has

the ability to hedge interest rate risk associated with retained residual

positions. The sensitivities in the previous table do not reflect any hedge

strategies that may be undertaken to mitigate such risk.

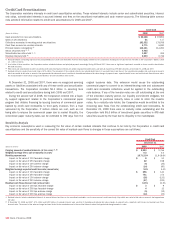

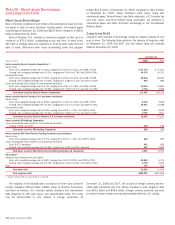

Other Securitizations

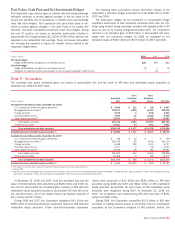

The Corporation also maintains interests in other securitization vehicles. These retained interests include senior and subordinated securities and

residual interests. The following table summarizes selected information related to home equity and automobile loan securitizations for 2008 and 2007.

Home Equity Automobile

(Dollars in millions) 2008 2007 2008 2007

Cash proceeds from new securitizations

$–

$ 363 $ 741 $–

Losses on securitizations

(1)

–

(20) (31) –

Collections reinvested in revolving period securitizations

235

41 ––

Repurchase of loans from trust

(2)

128

–184 –

Cash flows received on residual interests

27

115 ––

Principal balance outstanding

(3)

34,169

8,776 5,385 1,955

Senior securities held

(4, 5)

–

24,102 1,400

Subordinated securities held

(4, 6)

3

14 383 33

Residual interests held

(7)

93

584 100

(1) Net of hedges

(2) The repurchases of loans from the trust for home equity loans during 2008 was a result of the Corporation’s representations and warranties and the exercise of an optional clean-up call. The repurchases of automobile

loans during 2008 was substantially due to the exercise of an optional clean-up call.

(3) The increase in principal balance outstanding at December 31, 2008 from the prior year was due to the addition of Countrywide home equity securitizations.

(4) As a holder of these securities, the Corporation receives scheduled interest and principal payments accordingly. During 2008 and 2007, there were no significant impairments recorded on those securities classified as

AFS debt securities.

(5) Substantially all of the held senior securities issued by these securitization vehicles are valued using quoted market prices. At December 31, 2007, all of the senior securities issued by home equity securitization

vehicles were classified as trading account assets. At December 31, 2008 and 2007, substantially all of the senior securities issued by the automobile securitization vehicle were classified as AFS debt securities.

(6) At December 31, 2008 and 2007, all of the subordinated securities issued by the home equity securitization vehicles were valued using model valuations. At December 31, 2008, all of the subordinated securities

issued by the home equity securitization vehicles were classified as AFS debt securities and at December 31, 2007, all of these subordinated securities were classified as trading account assets. At December 31,

2008, all of the subordinated securities issued by the automobile securitization vehicle were classified as AFS debt securities and $330 million were valued using quoted market prices, while $53 million were valued

using model valuations. At December 31, 2007, all of the subordinated securities issued by the automobile securitization vehicle were valued using model valuations and classified as trading account assets.

(7) Residual interests include the residual asset, overcollateralization and cash reserve accounts, which are carried at fair value or amounts that approximate fair value. The residual interests were valued using model

valuations and substantially all are classified in other assets.

Under the terms of the Corporation’s home equity securitizations,

advances are made to borrowers when they make a subsequent draw on

their line of credit and the Corporation is reimbursed for those advances

from the cash flows in the securitization. During the revolving period of

the securitization, this reimbursement normally occurs within a short

period after the advance. However, when the securitization transaction

has begun its rapid amortization period, reimbursement of the Corpo-

ration’s advance occurs only after other parties in the securitization have

received all of the cash flows to which they are entitled. This has the

effect of extending the time period for which the Corporation’s advances

are outstanding. In particular, if loan losses requiring draws on monoline

insurer’s policies (which protect the bondholders in the securitization)

exceed a specified threshold or duration, the Corporation may not receive

reimbursement for all of the funds advanced to borrowers, as the senior

bondholders and the monoline insurer have priority for repayment. As of

December 31, 2008, the reserve for losses on expected future draw obli-

gations on the home equity securitizations in or expected to be in rapid

amortization was $345 million.

The Corporation has retained consumer MSRs from the sale or securi-

tization of home equity loans. The Corporation recorded $78 million in

servicing fees related to home equity securitizations during 2008. No

such fees were recorded during 2007. For more information on MSRs,

see Note 21 – Mortgage Servicing Rights to the Consolidated Financial

Statements. At December 31, 2008 and 2007, there were no recognized

servicing assets or liabilities associated with any of these automobile

securitization transactions. The Corporation recorded $30 million and

$27 million in servicing fees related to automobile securitizations during

2008 and 2007.

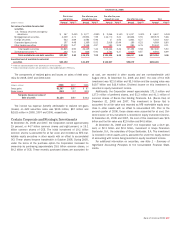

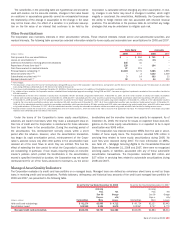

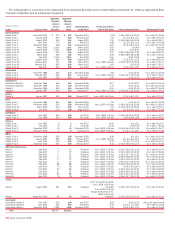

Managed Asset Quality Indicators

The Corporation evaluates its credit card loan portfolio on a managed basis. Managed loans are defined as on-balance sheet loans as well as those

loans in revolving credit card securitizations. Portfolio balances, delinquency and historical loss amounts of the credit card managed loan portfolio for

2008 and 2007, are presented in the following table.

At and for the Year Ended December 31, 2008 At and for the Year Ended December 31, 2007

(Dollars in millions) Outstandings

Accruing

Past

Due 90

Days or

More

Net

Charge-

offs/

Losses Outstandings

Accruing

Past

Due 90

Days or

More

Net

Charge-

offs/

Losses

Held credit card outstandings

$ 81,274 $2,565 $ 4,712

$ 80,724 $2,127 $3,442

Securitization impact

100,960 3,185 6,670

102,967 2,757 4,772

Managed credit card outstandings

$182,234 $5,750 $11,382

$183,691 $4,884 $8,214

Bank of America 2008

143