Bank of America 2008 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2008 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

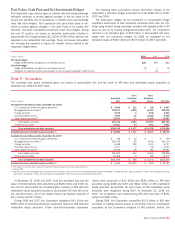

|

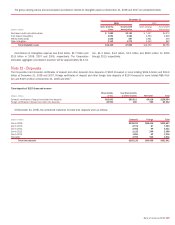

|

Unconsolidated VIEs

(Dollars in millions)

Multi-

Seller

Conduits

Asset

Acquisition

Conduits

Municipal

Bond

Trusts CDOs

Real Estate

Investment

Vehicles

Customer

Vehicles

Other

Vehicles Total

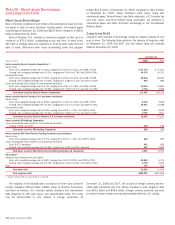

Unconsolidated VIEs, December 31, 2008 (1)

Maximum loss exposure

(2)

$42,046 $2,622 $7,145 $ 2,383 $5,696 $ 5,741 $4,337

$69,970

Total assets of VIEs 27,922 2,622 7,997 2,570 5,980 6,032 7,280

60,403

On-Balance Sheet Assets

Trading account assets $ 1 $ 1 $ 688 $ 732 $ – $ 2,877 $ 145

$ 4,444

Derivative assets – 293 379 6 – 2,864 –

3,542

Available-for-sale debt securities – – – 1,039 – – 5

1,044

Loans and leases 388 – – – – – 1,004

1,392

All other assets 23 – – – 4,996 – 1,765

6,784

Total $ 412 $ 294 $1,067 $ 1,777 $4,996 $ 5,741 $2,919

$17,206

On-Balance Sheet Liabilities

Derivative liabilities $ – $ 293 $ 27 $ 57 $ – $ – $ 85

$ 462

All other liabilities – – – – 1,632 – 80

1,712

Total $ – $ 293 $ 27 $ 57 $1,632 $ – $ 165

$ 2,174

Unconsolidated VIEs, December 31, 2007 (1)

Maximum loss exposure

(2)

$47,335 $6,399 $6,341 $11,135 $5,009 $ 9,114 $6,199

$91,532

Total assets of VIEs 29,363 6,399 6,361 13,300 5,138 11,725 9,562

81,848

(1) Includes unconsolidated VIEs and certain QSPEs which are not included in Note 8 – Securitizations to the Consolidated Financial Statements.

(2) Maximum loss exposure for unconsolidated VIEs includes on-balance sheet assets plus off-balance sheet exposures. It does not include losses previously recognized through write-downs of assets or the establishment

of derivative or other liabilities.

The table above presents total assets of unconsolidated VIEs in which

the Corporation holds a significant variable interest and Corporation-

sponsored unconsolidated VIEs in which the Corporation holds a variable

interest, even if not significant, at December 31, 2008 and 2007. The

table also presents the Corporation’s maximum exposure to loss result-

ing from its involvement with these VIEs at December 31, 2008 and

2007. The Corporation’s maximum exposure to loss is based on the

unlikely event that all of the assets in the VIEs become worthless and

incorporates not only potential losses associated with assets recorded on

the Corporation’s balance sheet but also potential losses associated with

off-balance sheet commitments such as unfunded liquidity commitments

and other contractual arrangements. Certain QSPEs in which the Corpo-

ration has continuing involvement but that are not discussed in Note 8 –

Securitizations to the Consolidated Financial Statements are also

included in the table. Assets and liabilities of unconsolidated VIEs

recorded on the Corporation’s Consolidated Balance Sheet at

December 31, 2008 are also summarized above.

Except as described below, we have not provided financial or other

support to consolidated or unconsolidated VIEs that we were not pre-

viously contractually required to provide, nor do we intend to do so.

Multi-Seller Conduits

The Corporation administers four multi-seller conduits which provide a

low-cost funding alternative to its customers by facilitating their access to

the commercial paper market. These customers sell or otherwise transfer

assets to the conduits, which in turn issue short-term commercial paper

that is rated high-grade and is collateralized by the underlying assets. The

Corporation receives fees for providing combinations of liquidity and

SBLCs or similar loss protection commitments to the conduits. The

Corporation also receives fees for serving as commercial paper place-

ment agent and for providing administrative services to the conduits. The

Corporation’s liquidity commitments are collateralized by various classes

of assets which incorporate features such as overcollateralization and

cash reserves that are designed to provide credit support to the conduits

at a level equivalent to investment grade as determined in accordance

with internal risk rating guidelines. Third parties participate in a small

number of the liquidity facilities on a pari passu basis with the Corpo-

ration.

The Corporation determines whether it must consolidate a multi-seller

conduit based on an analysis of projected cash flows using Monte Carlo

simulations which are driven principally by credit risk inherent in the

assets of the conduits. Interest rate risk is not included in the cash flow

analysis because the conduits are not designed to absorb and pass along

interest rate risk to investors. Instead, the assets of the conduits pay

variable rates of interest based on the conduits’ funding costs. The

assets of the conduits typically carry a risk rating of AAA to BBB based on

the Corporation’s current internal risk rating equivalent, which reflects

structural enhancements of the assets, including third party insurance.

Projected loss calculations are based on maximum binding commitment

amounts, probability of default based on the average one year Moody’s

Corporate Finance transition table, and recovery rates of 90 percent, 65

percent and 45 percent for senior, mezzanine and subordinate

exposures. Approximately 97 percent of commitments in the uncon-

solidated conduits and 70 percent of commitments in the consolidated

conduit are senior exposures. Certain assets funded by one of the uncon-

solidated conduits benefit from embedded credit enhancement provided

by the Corporation. Credit risk created by these assets is deemed to be

credit risk of the Corporation, which is absorbed by third party investors.

The Corporation does not consolidate three conduits as it does not

expect to absorb a majority of the variability created by the credit risk of

the assets held in the conduits. On a combined basis, these three con-

duits have issued approximately $97 million of capital notes and equity

interests to third parties, $92 million of which were outstanding at

December 31, 2008. These instruments will absorb credit risk on a first

loss basis. The Corporation consolidates the fourth conduit, which has

not issued capital notes or equity interests to third parties.

At December 31, 2008, liquidity commitments to the consolidated

conduit were mainly collateralized by credit card loans (25 percent), auto

loans (14 percent), equipment loans (10 percent), corporate and

commercial loans (seven percent), and trade receivables (six percent).

None of these assets are subprime residential mortgages. In addition, 29

percent of the Corporation’s liquidity commitments were collateralized by

projected cash flows from long-term contracts (e.g., television broadcast

contracts, stadium revenues and royalty payments) which, as mentioned

above, incorporate features that provide credit support. Amounts

advanced under these arrangements will be repaid when cash flows due

Bank of America 2008

145